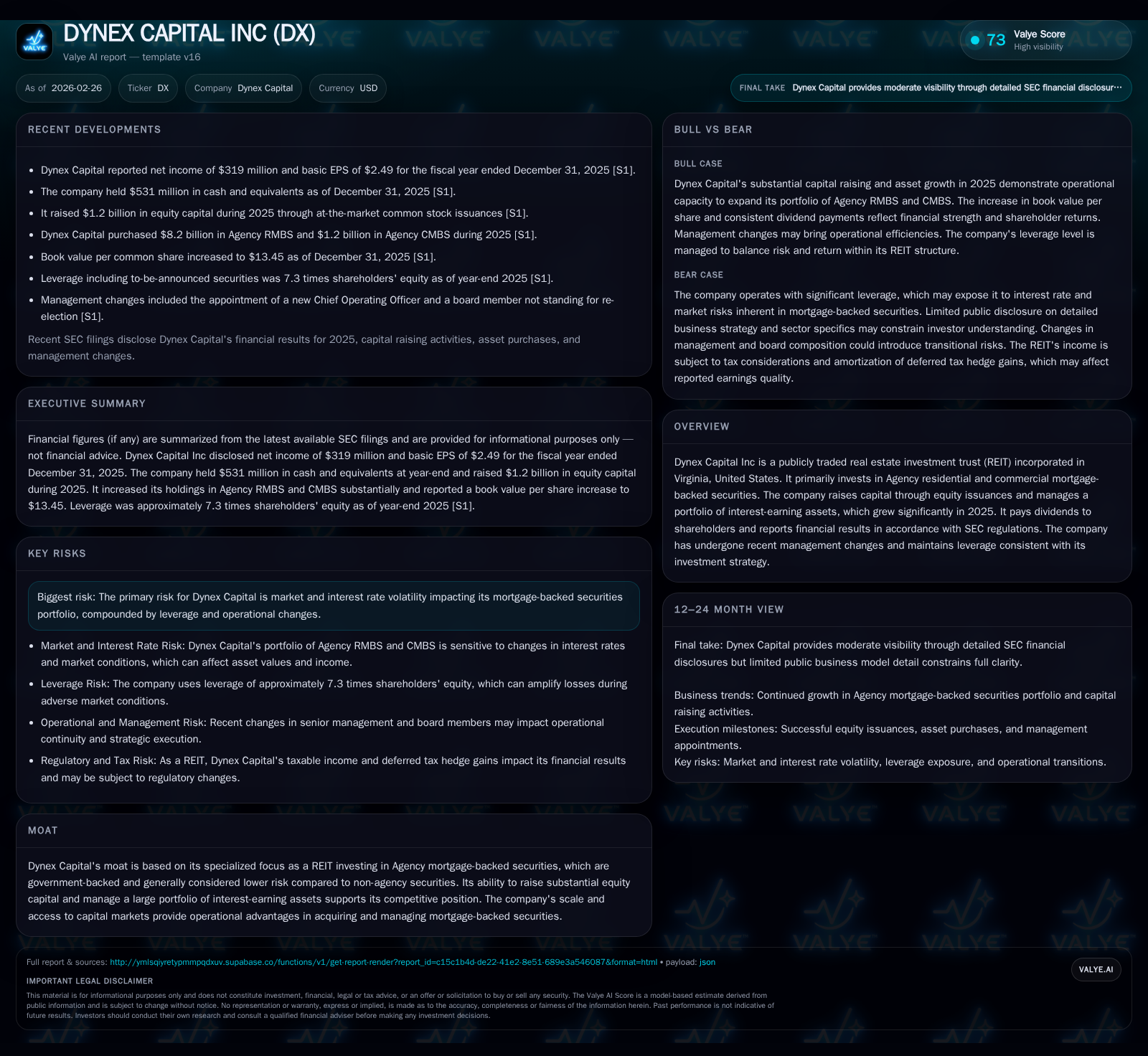

Dynex Capital’s 2025 Turnaround: From Rare Down Year to Robust Portfolio Expansion

After struggling with a rare net loss in 2023, Dynex Capital converted to robust earnings growth and significant portfolio scaling in 2025, fueled by strategic equity raises and focused Agency RMBS accumulation.

Dynex Capital rebounded strongly in 2025 from a modest net loss in 2023 to delivering $319 million in net income, driven by aggressive asset purchases and expanded equity capital. The company boosted its interest-earning asset base by nearly 60% and raised over $1.2 billion through at-the-market stock offerings. Despite elevated leverage of about 7.3x equity including TBAs, Dynex maintained dividend growth with $2.00 declared for 2025, reflecting improved earnings power and cash flow generation. The REIT continues to navigate market and interest rate risks inherent in Agency mortgage-backed securities investing while positioning for sustained performance amid evolving capital markets dynamics.

From Deficit to Dividend: The Journey Through 2023-2025 Performance

Dynex Capital’s financial trajectory over the past few years has been marked by a dramatic reversal of fortune. In calendar year 2023, the mortgage REIT reported a rare net loss amounting to approximately $6.1 million [F1], reflecting pressures from interest rate volatility that compressed net interest margins across the sector. Fast forward two years, annual net income had soared over fivefold to reach $319 million by the end of fiscal year 2025 [F1]. This represents an impressive 180% year-over-year increase from the prior period.

Accompanying this surge was a remarkable expansion in operating cash flow (CFO), which leapt more than sevenfold from roughly $14 million in 2024 to nearly $121 million in 2025 [F1]. This restored source of liquidity is critical not only for covering dividend distributions but also fueling ongoing portfolio investments. Book value per common share similarly advanced, underpinned by comprehensive income gains emphasized in recent company disclosures [S12].

This turnaround is emblematic of Dynex’s ability to navigate complex macro conditions while leveraging its niche as a mortgage REIT focused exclusively on Agency securities — financial instruments backed by government-sponsored entities that typically afford lower credit risk compared to non-agency alternatives.

Historical Financial Summary (FY2022-FY2025)

Historical performance (annual)

| FY | Net ($mm) | CFO ($mm) | Net YoY |

|---|---|---|---|

| 2025 | 319 | 121 | +180.1% |

| 2024 | 114 | 14 | +1958.0% |

| 2023 | -6 | 62 | -104.3% |

| 2022 | 143 | 126 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | Div ($mm) |

|---|---|

| 2025 | 247 |

| 2024 | 118 |

| 2023 | 93 |

| 2022 | 72 |

Source: SEC companyfacts cache [F1].

Note: Approximate ROE calculated using latest net income divided by last reported equity at FY2012 level due to limited comparable data.

Portfolio Expansion and Asset Acquisition Driving Growth

Central to Dynex Capital’s resurgence was an active campaign of asset acquisitions notably within Agency residential mortgage-backed securities (RMBS) and commercial mortgage-backed securities (CMBS). Over the course of fiscal year 2025 alone, the firm amassed roughly $8.2 billion of Agency RMBS and an additional $1.2 billion of Agency CMBS [S12].

This acquisition spree expanded the average balance of interest-earning assets significantly by approximately 58% year-over-year [S12], underpinning top-line revenue acceleration through yield capture amid fluctuating spread environments. The firm’s focus on Agency MBS mitigates credit risk given GSE guarantees but places it squarely exposed to duration and convexity risks stemming from changes in interest rates.

To capitalize on favorable market dislocations including TBA (to-be-announced) securities opportunities—futures contracts allowing purchase or sale of agency MBS before their delivery—Dynex leveraged its scale and operational expertise. This approach has cemented the REIT’s moat anchored in specialized asset management capabilities within government-backed mortgage debt sectors.

Capital Strategy: Equity Raises Fueling Scale and Liquidity

Augmenting its firepower for purchases was an aggressive equity issuance strategy executed primarily through at-the-market (ATM) stock offerings throughout the year. These initiatives yielded $1.2 billion in net proceeds during calendar year 2025 alone [S12], bolstering cash reserves and ensuring flexibility amid volatile funding environments.

As of December end-of-year close, liquidity stood at about $1.4 billion [S12], providing ample runway for further portfolio rotation or tactical buying as market dynamics evolve.

The company systematically expanded its distribution agreement capacity via multiple amendments culminating in an authorized pool upward of over two hundred million shares available for sale via ATM programs as recent as January ’26 [S16][S18]. This underscores both management’s confidence and market receptivity but also necessitates vigilance around shareholder dilution tradeoffs versus accretive growth.

Leverage and Risk Management in A Mortgage REIT Context

While enhancing its asset base sustainably is fundamental to growth narratives here, Dynex has concomitantly maintained relatively high leverage levels characteristic of mREITs targeting yield enhancement strategies. Including cost basis for TBA positions—the futures instruments referred earlier—leverage stood around approximately 7.3 times shareholders’ equity by December ’25 [S12].

This degree of gearing exposes Dynex not just to base interest rate fluctuations but also convexity risk—the nonlinear price sensitivity of mortgage securities relative to rates—that can materially affect portfolio valuation volatility.

SEC filings explicitly enumerate such risks along with operational factors tied to recent executive turnover aimed at strengthening oversight [S4][S5][S12]. Notably the appointment of a new Chief Operating Officer early ’26 signals prioritization on day-to-day execution amidst this risk milieu [S14].

The choice to remain primarily invested in government agency MBS affords mitigation against credit events looming over non-agency sectors but does not insulate against macro shocks or policy shifts impacting yields or prepayment speeds.

Dividend Stability and Shareholder Returns Amid Market Cycles

A hallmark assessment point for REIT investors rests on reliability and sustainability of dividend payouts given tax-driven distribution requirements.

Dynex declared dividends totaling $2.00 per common share during fiscal year ’25 with quarterly payments steady at roughly $0.51 each [F1][S7][S9]. Supported by underlying earnings power evidenced via comprehensive income surges ($2.85 per share full-year comprehensive income reported) [S12], payout coverage ratios have improved markedly since prior years.

Despite increasing distributions alongside rapid growth spending and high leverage use, buybacks have been notably absent from recent capital return strategies [F1], reflective perhaps of prioritization toward asset accumulation rather than repurchase backstops.

Operating cash flows exceeding dividends paid indicate that internally generated cash suffices for sustaining payouts without excessive reliance on external financing channels currently [F1]. This dynamic underlines prudent capital stewardship balancing shareholder returns with growth aspirations.

What’s Next? Milestones and Metrics to Monitor in 2026

Looking ahead into calendar ’26 and beyond—while no explicit guidance or milestone forecasts are issued publicly at this time—a set of key performance indicators warrant close tracking (analysis):

- Economic return per share evolution on quarterly cadence highlighting book value growth versus dividends paid,

- Maintenance or potential recalibration of leverage multiples especially given market rate outlooks,

- Stability of portfolio yield spreads amid shifting Fed policy trajectories affecting prepayment behavior,

- Monitoring legal/regulatory headwinds impacting mREIT operating frameworks as delineated by SEC disclosures,

- Management team transitions’ effectiveness particularly integration of new COO responsibilities paired with CFO duties,

- Pace and pricing dynamics related to ATM equity issuance programs possibly affecting shareholder dilution versus accretive asset purchases.

Such metrics will illuminate whether Dynex can sustain or enhance its newly found footing beyond an exceptional turnaround into consistent growth phases characteristic of resilient mortgage REITs catering institutional investors seeking agency-backed exposure.

This report synthesizes publicly available SEC filings ([S#]) and company facts database ([F1]) dated up through early 2026 capturing Dynex Capital’s latest operating results without speculative projections or investment advice.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments