Hess Midstream LP Reports 8.4% Revenue Gain and 58% Net Income Surge in 2025 After Chevron Merger

The company’s 2025 results show improved margins and active share repurchases despite tight liquidity following integration into Chevron’s portfolio.

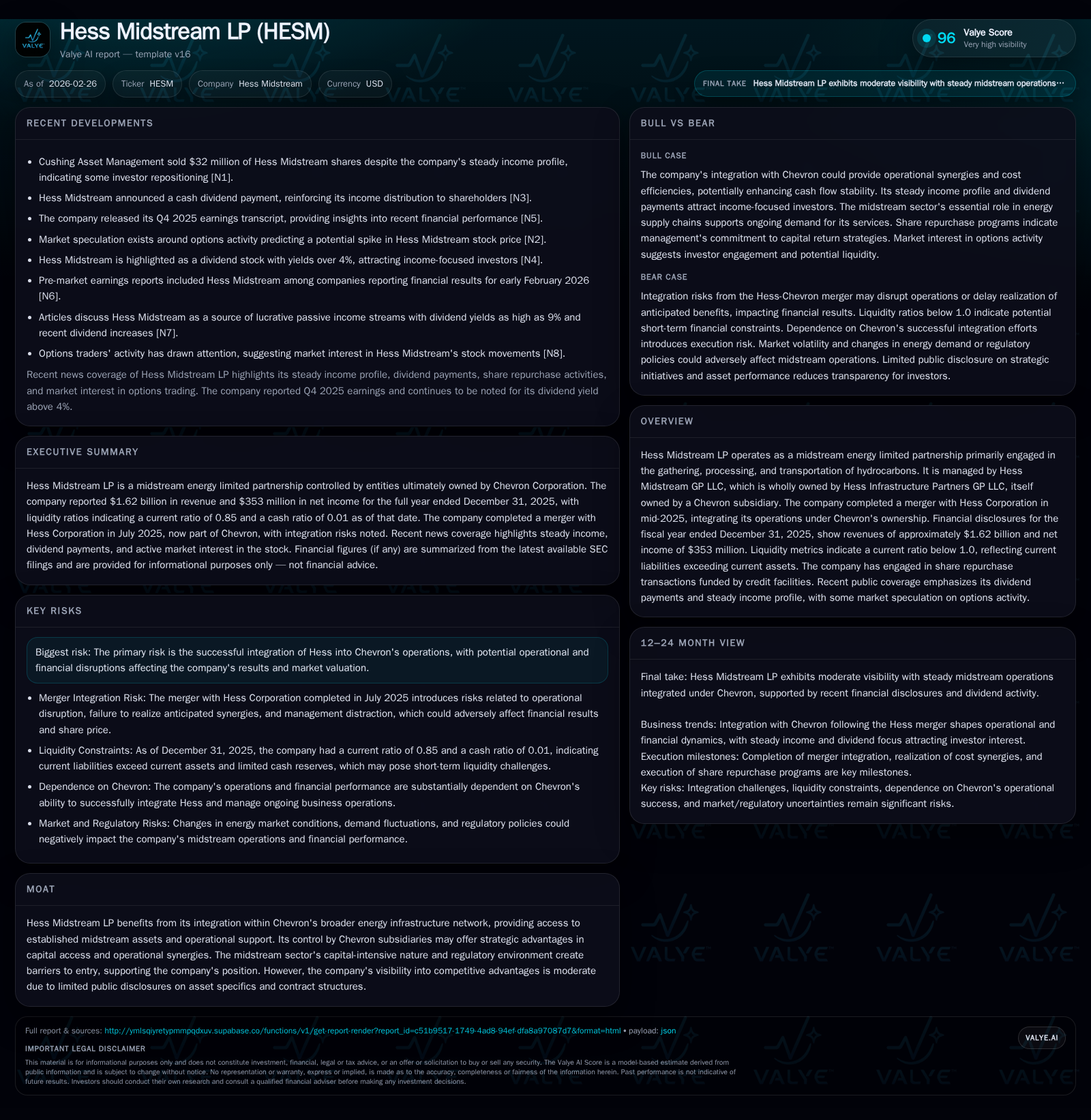

Hess Midstream LP reported revenue of $1.62 billion for the fiscal year ended 2025, up 8.4% year-over-year, driven by operational synergies following its merger into Chevron’s portfolio in mid-2025. Operating income and net income expanded substantially, aided by improving efficiencies and strong asset utilization. The company is managing liquidity carefully, with a current ratio below 1.0, while actively repurchasing shares funded through credit facilities. Future growth will depend on successful post-merger integration and realization of anticipated synergies.

Overview and Ownership Structure

Hess Midstream LP (NYSE: HESM) operates predominantly as a midstream energy limited partnership focused on gathering, processing, and transporting hydrocarbons. It is governed by Hess Midstream GP LLC, wholly owned by Hess Infrastructure Partners GP LLC, which in turn is owned entirely by Hess Investments North Dakota LLC, a Chevron subsidiary [S1]. This structure follows a significant corporate event — the mid-2025 merger wherein Hess Midstream was integrated into Chevron’s broader energy infrastructure network [S2][N2]. This transition marks a pivotal point from standalone operations toward tighter alignment with Chevron’s strategic initiatives.

Historical Performance: Drivers of Growth

The company demonstrated steadily improving financial performance over recent years. Revenue expanded from approximately $1.28 billion in 2022 to $1.62 billion in 2025 — an overall increase reflecting both organic growth and merger-related enhancements [F1]. Growth drivers included increased throughput volumes across its pipeline and processing assets, improved contract terms facilitated by Chevron's negotiating leverage, and operational synergies realized post-merger.

Operating income increased from about $791 million in 2022 to more than $1 billion in 2025, highlighting rising operating efficiencies amid relatively stable capital expenditure levels [F1]. Net income growth was particularly pronounced, rising from $84 million in 2022 to $353 million in 2025 — evidencing margin expansion and effective cost controls.

Cash flow generation remained robust with operating cash flow consistently above $860 million since 2022, culminating at just under $984 million for the latest fiscal year [F1]. The company managed capital investments prudently; after peaking near $306 million in 2024, capital expenditures dropped roughly 16.5% to $256 million in 2025.

This environment enabled significant capital return programs including share repurchases totaling about $400 million annually between 2023 and 2025 [F1]. These buybacks were partly financed with debt drawn on revolving credit facilities [S4][S6], demonstrating confidence in cash flow resiliency despite moderate leverage.

Financial Summary Table

Historical performance (annual)

| FY | Rev ($mm) | Net ($mm) | CFO ($mm) | OpInc ($mm) | Rev YoY | Net YoY |

|---|---|---|---|---|---|---|

| 2025 | 1621 | 353 | 984 | 1008 | +8.4% | +58.2% |

| 2024 | 1496 | 223 | 940 | 919 | +10.9% | +88.1% |

| 2023 | 1349 | 119 | 866 | 817 | +5.8% | +41.4% |

| 2022 | 1275 | 84 | 861 | 791 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | Buybacks ($mm) | FCF ($mm) |

|---|---|---|

| 2025 | 400 | 728 |

| 2024 | 300 | 634 |

| 2023 | 400 | 643 |

| 2022 | 400 | 623 |

Source: SEC companyfacts cache [F1].

Note: All figures rounded and sourced from SEC filings as of February 26, 2026 [F1].

Merger Impact and Future Growth Prospects

The July 2025 merger with Hess Corporation positioned Hess Midstream within Chevron's asset portfolio [S2]. This strategic consolidation is expected to generate run-rate cost synergies and accelerate free cash flow growth over a five-year horizon as communicated by management during earnings calls [N2]. However, challenges inherent to integration remain paramount risk factors:

- Potential operational disruptions could affect near-term results.

- Realization of expected synergies depends on effective coordination of assets and personnel retention amid organizational changes.

- Market uncertainty over commodity prices may influence throughput volumes indirectly impacting revenues.

Growth moving forward will hinge on these variables alongside ongoing investment in midstream infrastructure enhancements tailored towards growing hydrocarbon production volumes under Chevron's upstream strategy [S8].

Capital Allocation Priorities & Liquidity Profile

In alignment with its stable cash generation profile, Hess Midstream has maintained dividend payouts consistent with public reports emphasizing steady investor returns [N1][N6]. Dividends have become a notable consideration for income-focused investors against a backdrop of around four percent or higher yield on Class A shares.

Simultaneously, the company pursued sizeable share repurchase programs funded mainly through borrowings on existing credit lines — an approach observed in agreements executed in August prior year for approximately $70 million shares repurchased and retired subsequently [S4][S6]. Buybacks aggregated to about $400 million in fiscal year-end totals corroborated by official filings [F1].

Liquidity metrics reveal some constraint, with reported current assets of $159 million versus liabilities approximating $188 million by year-end December ’25 resulting in a sub-1 current ratio (~0.85) [F1]. This implies reliance on working capital management efficiency and access to committed credit for short-term obligations.

Chevron’s backing reduces refinancing risk yet underscores dependency on parent strategies given shared governance structures where directors and executives appointed are closely linked across entities ([S21],[S22]). The corporate office relocation to Houston aligns operationally closer with Chevron’s headquarters enhancing managerial integration effectiveness noted early in ’26 filings [S24].

Governance Changes Reflecting Parent Influence

Executive leadership shifts throughout late-2025 including the retirement of key officers succeeded by Chevron-affiliated replacements highlight increased governance integration [S25][S21]. Board appointments now include senior executives from Chevron subsidiaries responsible for functions such as crude supply and trading, underpinning strategic alignment especially relating to asset optimization across upstream/downstream segments.

These moves signal prioritization of operational cohesion while maintaining disclosure regimes required for public partnerships.

Risks to Monitor

Key uncertainties primarily relate to:

- Execution risks associated with integrating complex midstream asset portfolios under one management umbrella.

- Potential adverse impact on short-term earnings if synergy targets face delays or higher-than-expected costs emerge.

- Exposure to regulatory changes influencing pipeline operations or environmental compliance standards.

- Cybersecurity threats as noted among disclosed risk factors affecting infrastructure availability or integrity [S1].

Given this backdrop, investors should monitor quarterly earnings trends indicating synergy capture progress alongside management commentary addressing any operational hurdles [N2].

Conclusion

Hess Midstream LP's transition into Chevron's ecosystem has catalyzed measurable top-line growth and profitability gains through synergistic benefits realized since the mid-‘25 merger closing. Cash flow generation supports solid capital return initiatives despite tight liquidity metrics common within capital-intensive midstream operators leveraging modest working capital buffers.

Strategic risk centers on continued smooth post-merger integration success against sector volatility tied to upstream production growth assumptions that feed the company's pipeline volumes. Governance adjustments denote deeper parent oversight aiming to maximize asset value within Chevron's overall portfolio roadmap.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments