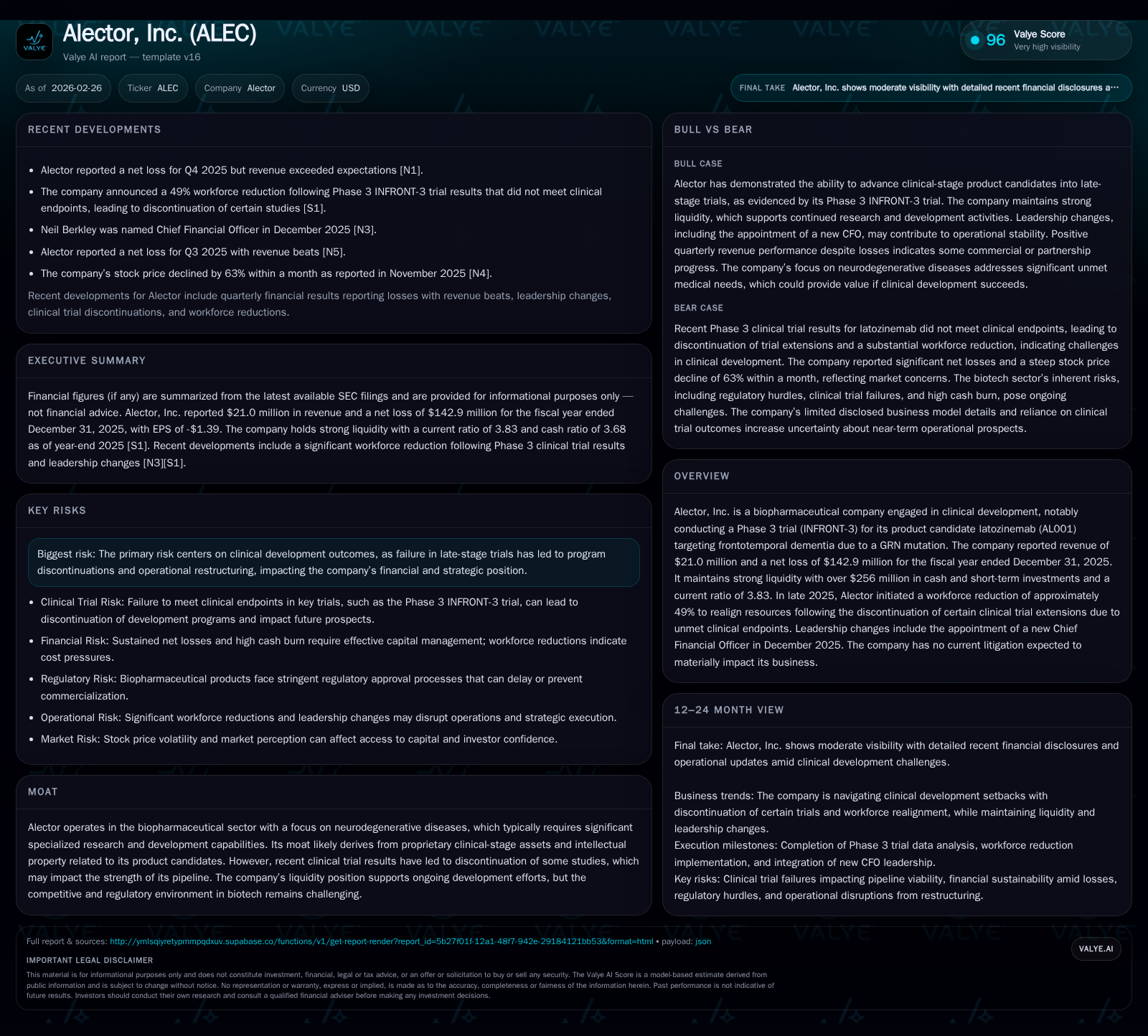

Alector's Clinical Setbacks Reshape Growth and Capital Strategy

Alector experienced a sharp revenue decline in 2025 linked to clinical trial failures, triggering workforce cuts and a strategic refocus.

In 2025, Alector’s revenue plummeted nearly 80% following disappointing Phase 3 trial results for its lead neurodegenerative candidate latozinemab (AL001), prompting discontinuation of certain studies and a significant workforce reduction. Despite sustained net losses and operational cash burn, the company maintains strong liquidity with over $256 million in cash and equivalents and a healthy current ratio. Leadership changes, including appointing a new CFO, underline efforts to recalibrate financial discipline. Forward growth is constrained by pipeline uncertainty, with progress hinging on remaining clinical assets and potential regulatory pathways.

Historical Revenue Peaks and Subsequent Decline

Alector’s top-line performance exhibits pronounced volatility tied closely to clinical program fortunes. Revenue grew from a modest $6.0 million in FY2019 to peak at $100.6 million in FY2024, driven largely by progression of clinical-stage assets towards later-stage trials and associated milestone payments [F1]. This trajectory was abruptly reversed in FY2025, with revenue collapsing nearly 80% to just $21.0 million. Such contraction directly corresponds to the discontinuation of key trial extensions after the Phase 3 INFRONT-3 trial of latozinemab (AL001) missed critical endpoints [S1][N1]. Operating income showed persistent deficits throughout this period: it worsened from -$145.0 million in FY2024 to -$156.0 million in FY2025, driven by sustained R&D costs despite program attrition [F1]. Net loss widened from -$119.0 million in FY2024 to -$142.9 million in FY2025 alongside revenue declines, highlighting operational leverage pressures [F1].

Historical performance (annual)

| FY | Rev ($mm) | Net ($mm) | CFO ($mm) | OpInc ($mm) | Rev YoY | Net YoY |

|---|---|---|---|---|---|---|

| 2025 | 21 | -143 | -184 | -156 | -79.1% | -20.1% |

| 2024 | 101 | -119 | -230 | -145 | +8.7% | |

| 2023 | -130 | -184 | -152 | +2.2% | ||

| 2022 | -133 | -20 | -138 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | FCF ($mm) | ROE% |

|---|---|---|

| 2025 | -184 | -466.3 |

| 2024 | -231 | -93.9 |

| 2023 | -187 | -97.2 |

| 2022 | -24 | -62.2 |

Source: SEC companyfacts cache [F1].

Note: The YoY percentages compare fiscal years where data is consecutively available.

Impact of INFRONT-3 Trial Outcomes on Operational Scale

The INFRONT-3 Phase 3 study evaluated latozinemab’s efficacy for frontotemporal dementia caused by GRN mutations—a highly specialized neurodegenerative condition with limited treatment options [S1]. Preliminary data disclosed in late 2025 revealed that the trial failed to meet its primary efficacy endpoint, resulting in the company halting the open-label extension portion and the broader continuation study [S14][N1]. Consequent operational resizing was severe: Alector announced a workforce reduction approximating 49%, which translates to around 75 employees across multiple departments [S14]. Associated one-time restructuring expenses are estimated at $7.7 million, largely related to severance and termination benefits payable through early-mid 2026 [S14][S16]. This strategic retrenchment reflects a narrowing focus on core assets with potential viability.

Pipeline Status and Forward Growth Prospects

At present, the core proprietary asset in clinical evaluation is latozinemab (AL001). Following the discontinuation of its pivotal Phase 3 extension studies, remaining development options are constrained [S1][N1]. The company has not disclosed any approved products or generating sustainable revenues outside this program [S1]. Forward growth thus heavily depends on either demonstrating positive outcomes from ongoing ancillary studies or advancing alternative product candidates earlier in development—details of which remain limited publicly.

Clinical risk remains significantly elevated given the historical failure; however, Alector emphasizes continued focus on neurodegenerative diseases leveraging its immuno-neurology platform [N1]. In absence of explicit forward sales guidance or milestone schedules from recent filings, key growth drivers will hinge on scientific advances translating into viable regulatory submissions or partnership deals—any of which could alter capital deployment strategies.

Liquidity Position Fuels Strategic Continuity Amid Setbacks

Notwithstanding operational challenges, Alector maintains a robust liquidity position as of December 31, 2025: current assets stand at approximately $266.5 million compared to current liabilities of $69.5 million, yielding an impressive current ratio of about 3.83—indicating ample short-term solvency [F1]. Cash and short-term investments total around $65.8 million providing essential runway for continuing R&D efforts despite steep revenue declines [F1][S13].

Operating cash flow outflows remain substantial at negative $184 million for FY2025 after accounting for minimal capital expenditures ($41,000)—reflective of intensive investment in pipeline progression even as programs contract [F1]. This cash burn underscores ongoing financing needs but also affirms commitment to core therapeutic development initiatives.

Capital Allocation: Evaluating Cash Flow, ROE, and Buybacks

Capital deployment centers predominantly on research-oriented expenditures as reflected by continued net losses ($142.9 million) and negative operating cash flows for multiple years running [F1]. Return on equity is sharply negative at approximately -466%, calculated from net losses relative to diminished shareholders’ equity ($30.6 million) post write-downs associated with program impairments [F1]. There have been no dividends declared or share repurchase programs active during this period; all internal resources appear dedicated toward sustaining clinical initiatives amid restructured operations.

This pattern aligns with typical biopharmaceutical developmental stage companies operating pre-commercially where prioritizing innovation financing takes precedence over shareholder distributions.

Leadership Changes and Management Response to Challenges

In late December 2025, Neil Berkley ascended from interim to permanent Chief Financial Officer roles while retaining duties as Chief Business Officer—a consolidation indicative of streamlined financial governance amid critical pipeline pauses [S22][N1]. This leadership adjustment coincided with personnel reductions and signals intensified oversight over budgeting and resource allocation during transformative phases.

Former President & Head of Research & Development Dr. Sara Kenkare-Mitra resigned effective year-end 2025 following the strategic pivot away from some development programs [S16], further reflecting organizational realignment to adapt addressing unsuccessful trial results without reported dissent over company policies.

Management confirms absence of any material ongoing legal proceedings affecting business fundamentals [S4].

Key Milestones and Upcoming Catalysts to Monitor

While explicit guidance or forecasted milestones were not provided recently [N1][S1], analysts should monitor:

- Any interim updates or data readouts from residual clinical programs involving AL001 or alternative candidates,

- Regulatory engagement activities potentially signaling submissions or fast-track considerations,

- Strategic collaborations or licensing agreements that may augment pipeline depth or extend financial flexibility,

- Further operational adjustments if trial risks materialize affecting resource allocation.

Progress on these fronts will be critical determinants shaping financial outlook beyond immediate liquidity preservation efforts.

This analysis synthesizes Alector’s latest annual filings and public disclosures without speculative estimates absent direct company guidance or market consensus forecasts. The high-risk nature inherent in neurodegenerative drug development underscores volatility around projected outcomes which readers should incorporate when contextualizing corporate evolution.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments