Crescent Energy’s Strategic Expansion and Capital Discipline Frame 2025 Performance

Examining Crescent Energy's growth via acquisitions and disciplined capital management amid market headwinds for fiscal year 2025.

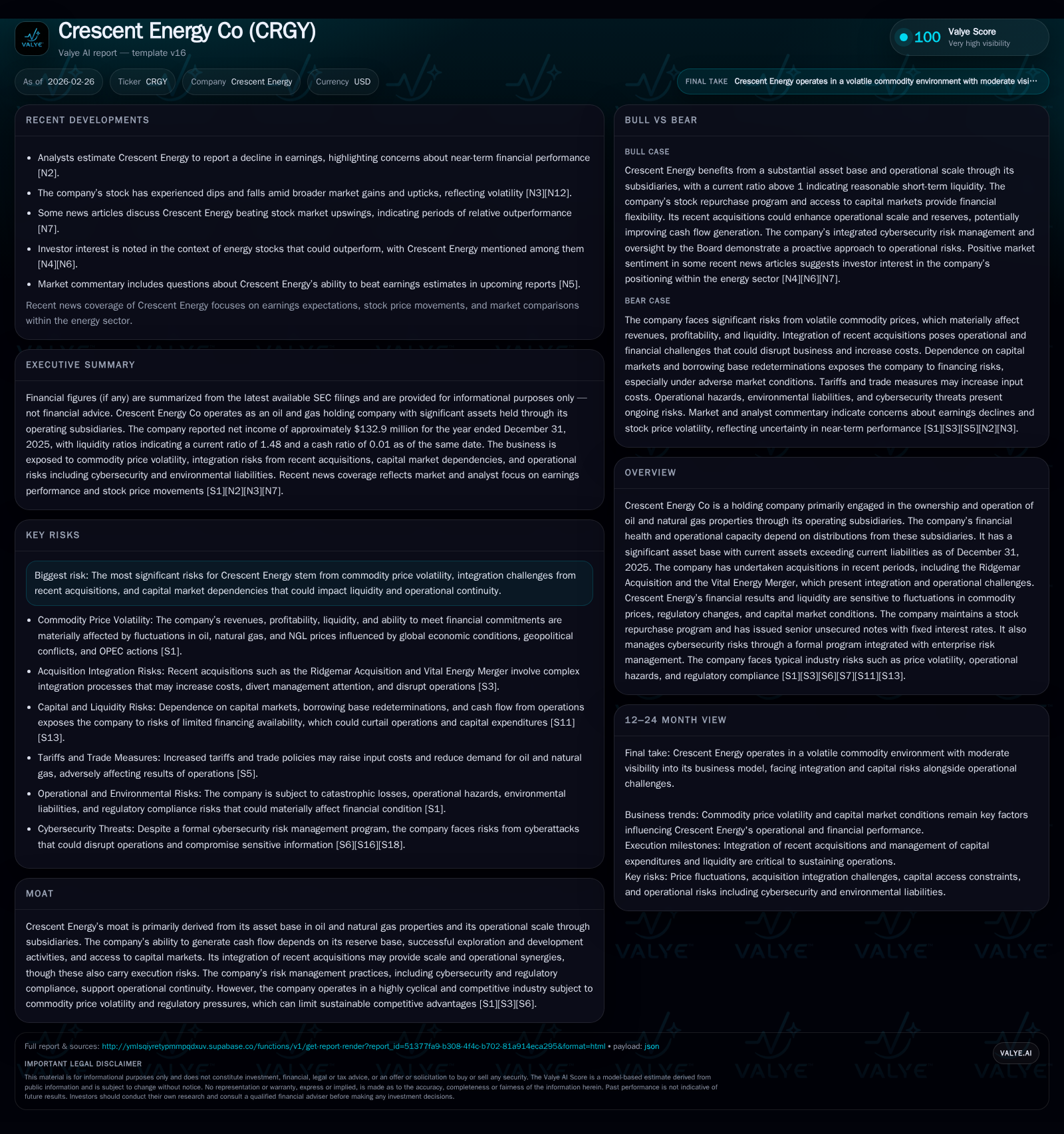

Crescent Energy demonstrated a modest rebound in operating income in 2025, supported by steady capital expenditures and significantly improved net income, reversing prior losses. The company faces integration and operational risks from recent acquisitions including Ridgemar and the Vital Energy merger, which have added scale but also complexity. Robust operating cash flow generation outpaced capital spending, enabling sustained shareholder returns through dividends and share repurchases, while liquidity remains sensitive to borrowing base redeterminations and commodity price volatility. Regulatory, cybersecurity, and macroeconomic risks continue to shape the operational landscape.

From Tide to Transition: Review of Crescent Energy’s Recent Growth Trajectory

Crescent Energy emerged from a challenging 2024 with a marked recovery in operating metrics in fiscal 2025, evidenced by a measured 5% increase in operating income to $229 million from $218 million a year earlier [F1]. This modest rebound followed significant losses the previous year reflecting transitional pressures associated with major asset acquisitions. Net income posted an even more pronounced turnaround, soaring 216% year-over-year to reach $133 million—underscoring successful operational adjustments post-acquisition. The company's ability to capitalize on its expanding asset base while navigating volatile commodity prices signaled resilience.

Capital expenditure patterns remained disciplined with nearly flat capex around $182 million, demonstrating investment moderation aligned with cash flow realities [F1]. This emphasis on sustainable reserve replacement costs—the fundamental driver behind oil & gas sustainable growth—reflects prudent project selection amid cyclicality. Operating cash flow grew substantially by over 37% year-over-year to about $1.68 billion, supporting a robust free cash flow profile nearing $1.5 billion after subtracting capex—a critical indicator of financial flexibility in a capital-intensive sector [F1].

Historical performance (annual)

| FY | Net ($mm) | CFO ($mm) | OpInc ($mm) | Capex ($mm) | Net YoY |

|---|---|---|---|---|---|

| 2025 | 133 | 1680 | 229 | 182 | +216.0% |

| 2024 | -115 | 1223 | 218 | 180 | -269.5% |

| 2023 | 68 | 936 | 325 | 84 | -30.1% |

| 2022 | 97 | 1012 | 1284 | 93 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | Div ($mm) | Buybacks ($mm) | FCF ($mm) |

|---|---|---|---|

| 2025 | 115 | 33 | 1499 |

| 2024 | 65 | 8 | 1043 |

| 2023 | 34 | 0 | 852 |

| 2022 | 28 | 0 | 920 |

Source: SEC companyfacts cache [F1].

Note: Operating income and net income fluctuations reflect prior-year impairments related to acquisition accounting adjustments.

Integration Realities: Impact of Ridgemar Acquisition and Vital Energy Merger

Crescent’s strategic expansion through the Ridgemar Acquisition and the Vital Energy Merger has altered its operational blueprint significantly. Management notes scale advantages that can enhance reserves replacement and operational synergies; however these benefits are tempered by execution risks tied to integrating distinct cultures and asset portfolios [N2][S1][S2].

Integration challenges manifest as potential short-term diluted earnings power due to management bandwidth devoted to alignment efforts and restructuring costs. Resource allocation may be strained during this transition phase affecting organic exploration initiatives and capital deployment efficiency. Liquidity depends on timely distribution flows from consolidated entities within OpCo's structure subject to legal restrictions under Delaware law and debt covenants [S9][S1].

Cash Flow Strength Amid Commodity Price Volatility

Despite market unpredictabilities driven by geopolitical tensions impacting oil and natural gas demand—and their prices—Crescent achieved solid operating cash flows commensurate with its asset scale. The nearly $1.68 billion CFO figure exceeded capex commitments for the year [$182 million], indicative of stringent capital discipline amid cyclical industry dynamics [F1][S1]. Strong free cash flow reflects effective hedging common within upstream operations cushioning commodity price exposure.

Risk disclosures highlight how fluctuations caused by global events such as conflicts affect pricing benchmarks integral to revenue stability. Seasonal temperature variations also influence natural gas demand impacting revenue variability forecasts inherent in continuous operation models for oil & gas producers [S1].

Capital Allocation Focus: Dividends, Buybacks and Investment Discipline

Strong free cash flows underpin Crescent’s capital return policy focused on shareholder value enhancement. Dividends increased significantly to $115 million in 2025 from roughly $65 million the prior year—a near doubling consistent with improved earnings capacity [F1][S5]. Concurrently share repurchases rose notably from $7.8 million in 2024 to over $33 million in 2025 supported by an expanded board-approved buyback authorization increased recently from $150 million initially approved in March 2024 to $400 million indefinitely extended as of February 2026 [S6].

These capital return actions balance rewarding shareholders presently while preserving investment optionality for organic growth or future bolt-on transactions aligned with strategic ambitions. Timing of buybacks is subject to market conditions plus regulatory considerations such as excise taxes on repurchases instituted under IRA legislation that may modulate repurchase cadence going forward [S6].

Liquidity Profile and Debt Management Under Increased Leverage

As a holding company relying on distributions from OpCo subsidiaries as its sole source of funding corporate overheads including tax payments it faces liquidity sensitivities heightened by capital-intensive acquisition activity [S1][S9]. Borrowing base redeterminations linked to revolving credit facilities impose semiannual assessments that may reduce credit availability depending on asset valuations anchored on commodity price forecasts at determination points scheduled twice yearly [S4][S7]. These reductions introduce refinancing or working capital risks typical among exploration & production entities during mid-cycle troughs.

Additional indebtedness associated with acquisition financing—including assumption of Vital Energy senior notes—elevates leverage potentially constraining future capital market access or increasing margin calls if credit ratings deteriorate due to commodity price declines or event-driven risks [S10][S17]. Interest rate exposure under variable rate debt compounds funding cost uncertainties.

Regulatory and Market Risks Influencing Operational Resilience

Crescent operates within a complex regulatory environment encompassing federal,state,and local statutes governing environmental protection,pipeline safety(PHMSA),interstate commerce(FERC),taxation,and anti-manipulation rules impacting commodity trading relevant to physical sales hedging programs[S8][S14][S18].[S2]Notes rising raw material input costs due to tariffs since April2025 injecting inflationary pressures that could compress margins if passing along increases is constrained.

Environmental regulations including methane leak detection requirements for gathering pipeline operations may necessitate accelerated capital projects or enhanced maintenance expenditures beyond current budgets.Failure to comply invites civil penalties scaling into multi-million dollar daily fines subject to enforcement protocols by agencies like FERC or PHMSA with escalating scrutiny noted around climate change litigation risks paralleling industry peers' experiences[S16][S22][S23].

Cybersecurity risk is addressed through an enterprise-wide governance framework overseen quarterly at board level involving cross-functional teams integrating IT security with operations risk mitigation.The Head of Cybersecurity & GRC brings two decades’ domain expertise ensuring specialized defense postures against emerging threats typical for energy infrastructure providers[S20].

Outlook Essentials: What to Watch for in Crescent Energy’s Next Phase

No explicit forward guidance was provided per latest filings; however upcoming indicators include monitoring integration milestones tied to Ridgemar assets and Vital Energy merger realization progress operationally and financially[N3][N4]. Semiannual borrowing base redeterminations anticipated around April will serve as pivotal inflection points dictating near-term liquidity flexibility.

Commodity price movements remain the paramount macro catalyst shaping revenue outlooks alongside legislative developments impacting tax treatment or environmental compliance costs noted within regulatory disclosures.Market sentiment shifts surrounding energy transition narratives versus fossil fuel valuations also impact financing conditions available for sustaining capex programs aligned with reserve replacement targets.

Taken together,Crescent's trajectory reflects a nuanced balancing act between expansion-driven scale benefits intertwined tightly with operational execution excellence amidst an inherently cyclical marketplace shaping potential upside or downside scenarios.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments