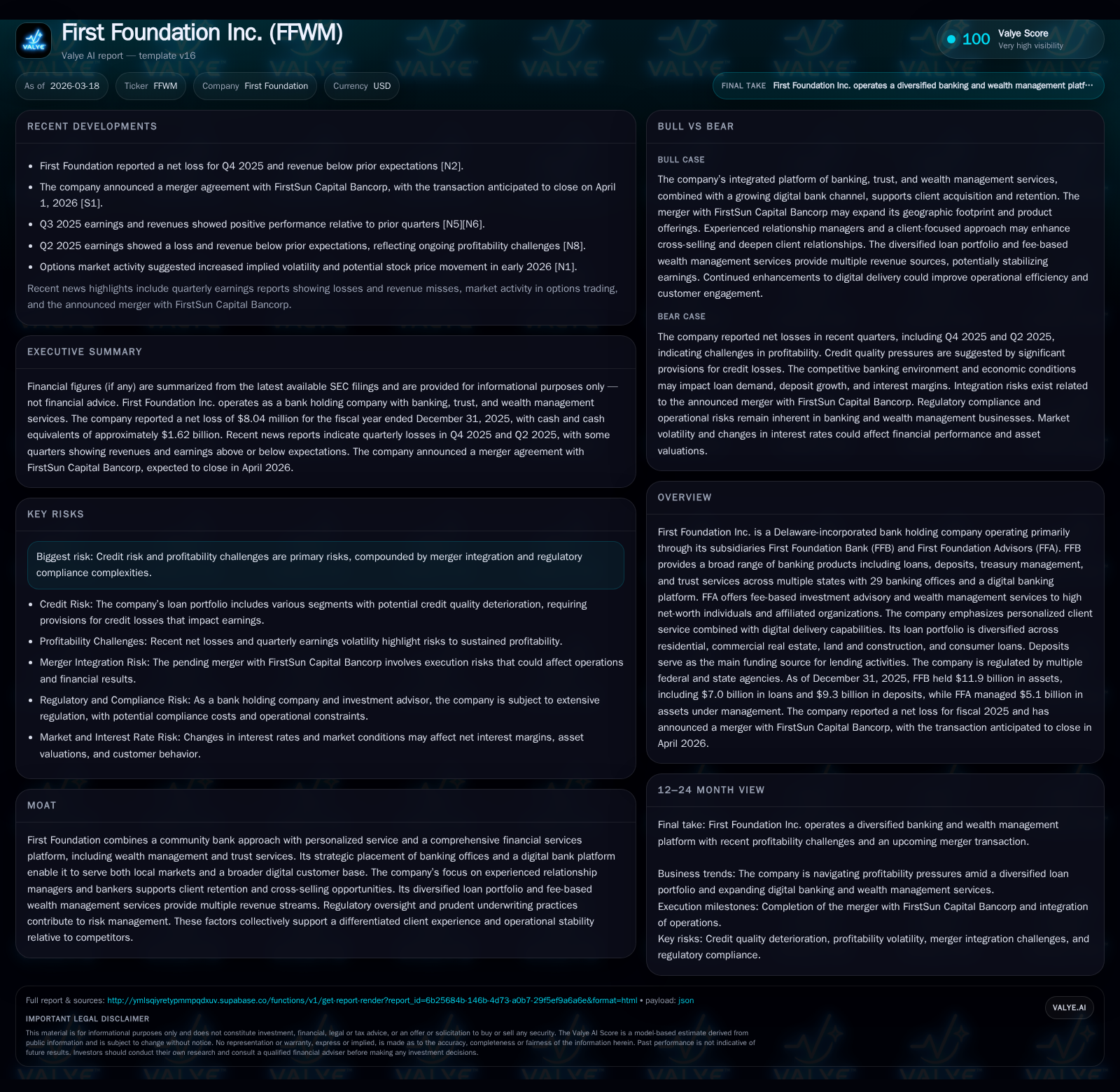

First Foundation’s Shift from Profitability to Integration Signposts Next Phase

Examining how First Foundation recalibrates strategy amid earnings challenges and merger integration while leveraging its diverse financial platform.

First Foundation Inc. has experienced notable shifts from profitability to operating losses in recent years, reflecting pressures from credit provisions and merger-related expenses. Its diversified loan portfolio—spanning multifamily residential, commercial real estate, land and construction, alongside fee-based wealth management—underpins multiple revenue streams but faces margin compression and credit risk factors. The firm’s integration of FirstSun Capital Bancorp, now federally approved, aims to expand market reach and realize scale efficiencies, though operational consolidation poses challenges. Capital discipline, marked by restrained buybacks and dividends amid negative free cash flow, shapes the current capital allocation outlook. Monitoring asset quality metrics and deposit growth will be essential milestones for assessing recovery momentum.

Financial Momentum and Shifts: Reviewing Past Growth Drivers

First Foundation's financial performance over the past four fiscal years illustrates a pronounced reversal from profitability to losses, symptomatic of credit and integration headwinds. The company reported net income of $17.3 million in FY2022 before declining to a modest $2.5 million gain in FY2023, then flipping into losses of -$14.1 million in FY2024 and narrowing slightly to -$8.0 million in FY2025 [F1]. Operating cash flow exhibited similar volatility: a robust $101 million positive generation in FY2022 gave way to a steep decline through FY2024's -$8.7 million and further down to -$31.9 million by end-2025. Capital expenditures increased somewhat from $4.6 million in FY2022 to $3.3 million last year after peaking at $8.2 million in FY2023 as investments in digital infrastructure were prioritized amidst changing client engagement trends [F1].

The plunge in operating cash flow alongside net loss signals intensified credit provisioning consistent with sectorwide pressures amid an elevated default risk environment for select loan categories. Additionally, the costs related to recent merger activities have pressured earnings and liquidity dynamics.

Historical performance (annual)

| FY | Net ($mm) | CFO ($mm) | Capex ($mm) | Net YoY |

|---|---|---|---|---|

| 2025 | -8 | -32 | 3 | +43.0% |

| 2024 | -14 | -9 | 3 | -653.8% |

| 2023 | 3 | 6 | 8 | -85.3% |

| 2022 | 17 | 101 | 5 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | Div ($mm) | Buybacks ($mm) | FCF ($mm) |

|---|---|---|---|

| 2025 | 1 | 0 | -35 |

| 2024 | 1 | 0 | -12 |

| 2023 | 9 | 1 | -2 |

| 2022 | 25 | 5 | 96 |

Source: SEC companyfacts cache [F1].

(Note: Dividend paid amount for FY2025 corresponds with payments through December 31, 2024.)

Diverse Loan Portfolio and Wealth Management as Revenue Pillars

Central to First Foundation’s business model is its diversified loan portfolio comprising multifamily residential mortgage loans primarily collateralized by adjustable-rate instruments with initial fixed-rate periods spanning three to ten years; commercial real estate loans including both owner-occupied and non-owner occupied properties featuring adjustable rates tied to independent indexes; land and construction loans tailored for urban infill multifamily projects plus owner-occupied single-family residences; as well as commercial industrial (C&I) loans mostly secured by business assets other than real estate; finally complemented by consumer loans generally granted against borrowers’ financial stability criteria .

This multi-channel approach balances loan-to-value ratios prudently while employing rigorous underwriting methodologies encompassing primary (collateral cash flows), secondary (borrower income and liquidity), and tertiary (collateral valuation) sources of repayment [S4]. Comprehensive stress testing regimes assess interest rate fluctuations, capitalization rate shifts, lease absorption trends, and economic outlooks within specific submarkets . High LTV ratios are generally avoided especially for land/construction segments given elevated default probabilities.

Simultaneously, First Foundation Advisors contributes steady fee-based income derived from $5.1 billion assets under management as of end-2025 by providing personalized wealth advisory services targeted at high-net-worth individuals who benefit from integrated trust solutions aligned with banking relationships [S14]. This mix generates multiple revenue streams that dilute concentration risks typical of lenders reliant solely on interest income.

Navigating Recent Profitability Challenges and Underwriting Rigor

The sharp downturn into net losses during FY2024–FY2025 reflects compounded effects of crescendoing credit risks amid challenging macroeconomic conditions that elevate potential loan losses especially within consumer and real estate segments [F1]. Margin compression has also emerged due to competition intensifying on deposit pricing coupled with elevated funding costs.

Underwriting rigor remains a cornerstone mitigating deeper deterioration: each credit approval hinges on comprehensive documentation supporting all repayment sources emphasizing the borrower's ability evidenced through debt service coverage ratios exceeding minimum thresholds typically above industry norms; borrower liquidity checks; verification of income statements; loan-to-value caps aligned with historical recovery benchmarks; plus qualitative assessments of character and management experience where applicable .

Operational stability is sought through centralized loan processing at Irvine administrative offices that enable uniform application of credit policies across geographies mitigating erratic credit behavior variance observed in fragmented banking entities [S9].

These thorough protocols partially explain why although net income contracted severely for two consecutive years, escalated allowances for credit losses suggest proactive reserve positioning designed to absorb anticipated charge-offs adequately rather than reactive impairment accounting.

Merger Integration: Regulatory Approval and Strategic Consolidation

First Foundation secured Federal Reserve approval on March 11, 2026 to merge with FirstSun Capital Bancorp, signaling regulatory confidence in the combined entity's capitalization plans and oversight framework post-transaction [S3,N1]. This strategic consolidation extends the branch footprint beyond existing locations enhancing competitive positioning within target markets.

The integration aims to harness cost synergies via elimination of overlapping support functions while unifying digital platforms thereby increasing efficiency metrics over medium term horizons [N1]. However, operational complexities persist given the need for harmonizing varied IT systems, standardizing underwriting processes shaped by different regional lending cultures, retaining key relationship managers amidst organizational reshuffles, plus managing regulatory compliance layers expanding through enlarged asset bases.

From the buy-side perspective these integration risks warrant exacting monitoring as premature cost cuts or misaligned customer experiences could erode established client loyalty foundation crucial for cross-selling banking alongside wealth management products.

Outlook on Growth Prospects Amid Competitive and Regulatory Constraints

Absent explicit financial guidance disclosures post-merger closure ([N1],[S1],[S2]), prudent investor attention focuses on forward levers embedded within First Foundation’s dual delivery channels combining traditional banking offices with cutting-edge digital platforms attracting nationwide depositors beyond physical branch catchments [S14].

Client retention fueled by experienced relationship managers incentivized via team-oriented compensation plans preserves revenue predictability through fee income growth particularly within wealth advisory trailing broader economic cycles more resiliently than lending interest margins [S14]. Expansion into underserved niches such as SBA-guaranteed small business lending underpins community banking mission broadening client acquisition pipelines constrained less by rate environments than regulatory capital buffers limiting aggressive asset growth strategies [S6,S10].

Competitive pressures remain salient especially amid rising regulatory scrutiny intensifying operational overheads alongside disciplined underwriting necessary given recent higher delinquency patterns anticipated during economic normalization phases.

Capital Allocation: Dividends, Buybacks, and Cash Flow Realities

Despite two consecutive loss-making fiscal years through end-2025 First Foundation maintained dividend distributions totaling approximately $1.13 million annually since FY2024 down sharply from $24.8 million paid out in FY2022 reflecting conservative payout philosophy during earnings stress cycles balancing shareholder expectations against internal capital needs [F1]. Concurrent share repurchase activity manifested similarly restraint dropping below half-million dollars recently signaling prudent balance sheet stewardship prioritizing liquidity preservation over aggressive capital returns amid negative free cash flow estimated near -$35 million last fiscal year (operating cash flow minus capex) [F1].

Equity levels contracted somewhat but remained robust around $913 million as of year-end 2025 buttressing capital adequacy supporting both organic origination pipelines plus integration-related expenses without immediate external equity raises noted thus far though vigilance toward stress testing outcomes remains elevated given heightened credit provisioning trends outlined previously .

Incremental capital expenditures reflect continued investments into technology infrastructure enabling scalable digital banking deployments complementing personalized advisory delivered through human advisors—a duality central to maintaining competitive advantage over peer community banks reliant predominantly on legacy models lacking integrated offerings or technological agility.

Key Milestones to Watch and Analytical Forecasts

In absence of forward-looking guidance explicitly published by First Foundation post-merger announcement ([N1],[S3]), investors should prioritize upcoming quarterly earnings publications focusing sharply on asset quality indicators explicitly: non-performing loans ratio movements indicative of potential credit erosion or stabilization; loan loss reserve adequacy relative to emerging delinquency trends; core deposit growth tracing customer acquisition effectiveness particularly within newly consolidated markets; alongside trends in fee income generated by wealth advisory arms signaling client base durability or shift.

Additionally attention toward effective merger integration progress tracked through expense ratio improvements or one-time integration-related costs disclosed will provide clarity on realization of expected scale economies versus persistent execution risks.

Consistent improvement across these parameters would signal transition from recent profitability setbacks toward sustainable earnings trajectories leveraging First Foundation’s diversified multi-channel revenue model fortified by capital discipline adhering stringently to underwriting standards benchmarked contextually against prevailing macroeconomic stressors.

This analysis synthesizes publicly available financial data including SEC filings ([F1], [S#]) alongside contemporaneous news reports ([N#]). It does not constitute investment advice nor forecasts but serves as an informed assessment based strictly on verified metrics and documented company disclosures.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments