Family Office of America’s Strategic Acquisitions Shape CPA Succession and Wealth Services Growth

FOFA’s recent quarter highlights acquisitions and integration efforts critical to consolidating CPA practices amid an aging professional base, underpinning its holistic family office platform expansion.

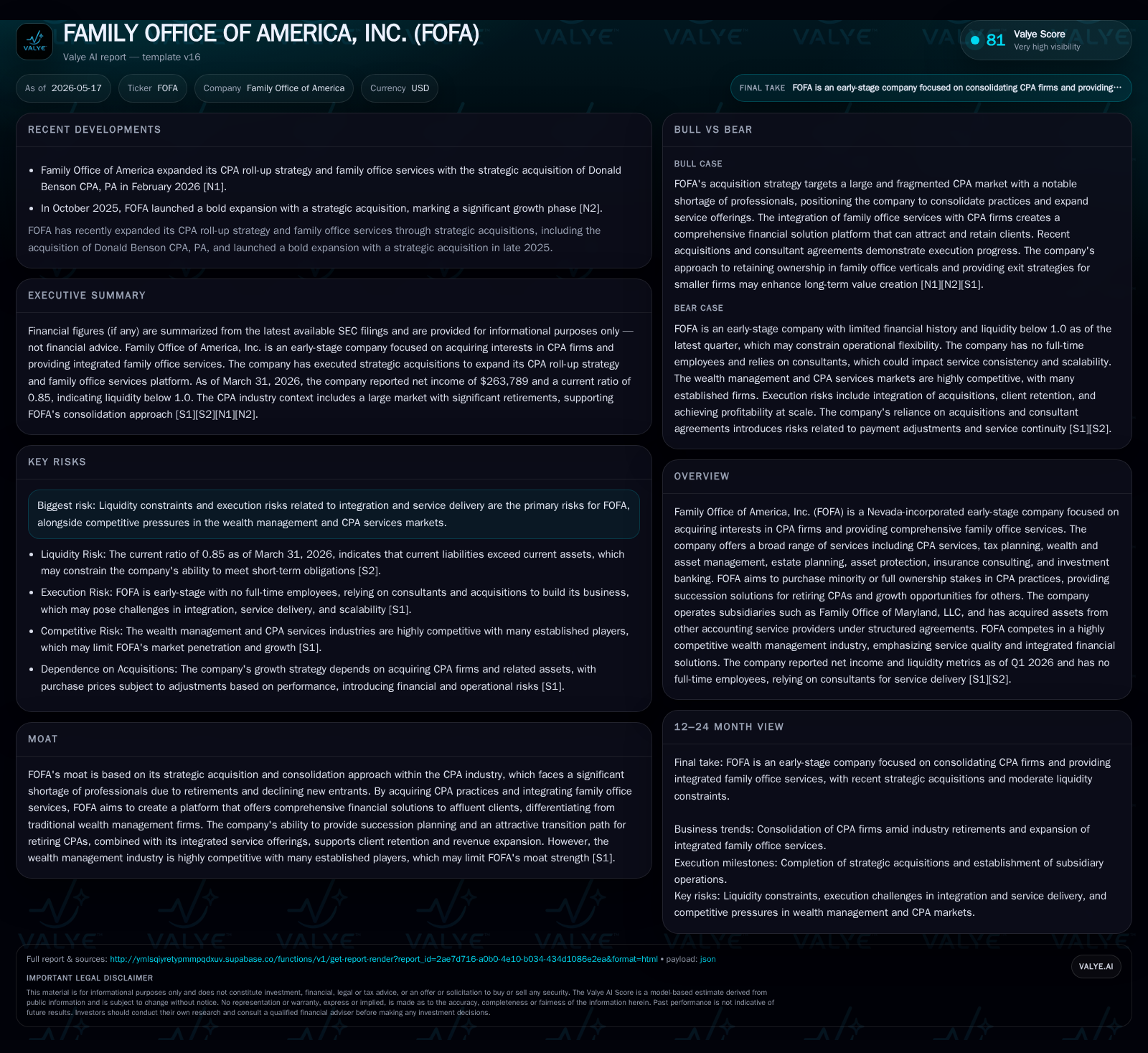

In its latest 10-Q filing dated May 15, 2026, Family Office of America, Inc. (FOFA) advanced its strategy of acquiring CPA firm interests and related assets, exemplified by the Benson Family Office acquisition. This follows a continued push into integrated family office services through subsidiaries such as Family Office of Maryland. The company operates in a complex landscape marked by significant CPA retirements and competitive wealth management sectors. FOFA's business model hinges on succession solutions for retiring CPAs alongside cross-selling expanded financial services, providing a differentiated offering targeted at affluent clients. Key risks include tight liquidity—evidenced by a current ratio below 1—and integration challenges amid fierce market competition.

Latest Quarterly Operating Developments

The May 15, 2026 10-Q filing marks a pivotal update for Family Office of America (FOFA), underscoring its acquisition-driven expansion strategy within the CPA and family office services domain [S2]. The quarter reflects the first full operational period following the January 1, 2026 asset purchase agreement with Benson Family Office & Accounting Services, LLC [S9]. This transaction entailed acquiring non-attest service assets — encompassing tax preparation, bookkeeping, and related accounting activities — outside traditional audit scopes.

Payment for the Benson acquisition is structured over multiple years totaling $353,750, subject to subsequent adjustment based on achieved revenues ($283k threshold) and EBITDA ($76k benchmark) during a twelve-month measurement period [S7][S9]. Consulting arrangements with the former owner provide continuity to mitigate client attrition risks inherent in acquisitions [S7]. The stabilized retention of key personnel contributes to FOFA’s ability to integrate acquired practices effectively.

Additionally notable is FOFA’s subsidiary Family Office of Maryland ("FO Maryland"), incorporated in late September 2025 as part of vertical expansion designed to bundle multiple family office functions under one platform umbrella [S8]. FO Maryland's ongoing asset purchase agreement from Toone & Associates LLP finalized in Q4 2025 further extends FOFA’s footprint in regional markets with structured earn-out provisions emphasizing accountable revenue realization post-close [S8][S13].

Despite active acquisition pursuits, FOFA's liquidity position remains constrained with a current ratio of approximately 0.85; current liabilities at $787k exceed current assets of $669k as of March 31, 2026 [F1]. Total debt stands at roughly $508k, portraying a tight working capital environment that necessitates prudent cash flow management amid integration resource demands.

Business Model and Integrated Service Offering

FOFA synthesizes an acquisition-centric business model targeting minority or complete ownership stakes in established CPA firms while layering comprehensive family office services beyond pure compliance. Revenues stem primarily from operating acquired CPA practices' non-attest work streams—e.g., tax planning/preparation, bookkeeping—supplemented by wealth management advisory fees generated via affiliated family office entities such as FO Maryland [S1][S8].

This hybrid structure positions FOFA uniquely: rather than only offering traditional accounting or standalone wealth management services, it aims to establish platform stickiness via integrated offerings including estate planning, asset protection strategies, insurance consulting, and investment banking advisory services [S1]. Ownership participation aligns incentives across parties—retiring CPAs benefit from succession exit strategies while retaining potential distributions from affiliated wealth entities owned partially by their practice. This mutually beneficial framework supports both client retention and incremental wallet share expansion leveraging deeper client relationships.

Importantly, FOFA emphasizes non-attest engagements consistent with regulatory constraints affecting public accounting attest work preservation under the Uniform Accountancy Act. By focusing on these complementary services alongside holistic financial solutions typical of family offices servicing high-net-worth individuals or families, FOFA differentiates from commodity-like CPA consolidators and traditional wealth managers who often operate more siloed practices [S1][S8].

Competitive Dynamics in CPA and Wealth Management Sectors

The combined CPA practice consolidation and family office service market is intensely competitive. Large integrated financial institutions dominate much of wealth management through scale advantages while numerous niche providers vie for specialized client segments. FOFA operates amid this bifurcated landscape targeting mid-market CPA firms seeking succession alternatives as well as affluent clientele looking for consolidated advisory solutions [S1][S10].

Fragmentation characterizes the CPA sector with many small independent practices challenged by retiring principals; approximately 75% of U.S. CPAs are estimated at or nearing retirement age while new entrants have been declining—the number of candidates sitting for the examination dropped from about 50,000 in 2010 to roughly 32,000 by 2021 according to AICPA data referenced by FOFA [S10]. This shortage increases consolidation impetus but also invites competitors adopting different models—some focusing solely on mergers/acquisitions for scale without expanded service platforms.

FOFA’s moat rests on offering retiring or growth-oriented CPAs an attractive transition mechanism paired with enriched service capabilities that foster loyalty beyond simple compliance transactions. However, pricing remains vulnerable given fee sensitivities especially among cost-conscious clients accustomed to commoditized tax/accounting work. Larger competitors may leverage scale for cost efficiencies or brand credibility making client acquisition expensive.

Growth Catalysts: Industry Demographics and Succession Solutions

Demographic shifts constitute the core structural driver enabling FOFA’s growth thesis. The industry faces accelerated attrition among older CPAs with inadequate replacement levels creating an acute succession void [S10]. FOFA’s tailored approach of purchasing interests in practices offers immediate relief to retiring principals lacking clear exit paths.

Supplementing acquisitions with scalable family office solutions enables cross-selling possibilities potentially broadening average client revenue per firm beyond historical benchmarks limited largely to tax season spikes and related accountancy margins [S1][S10]. Expansion across state lines through subsidiaries like FO Maryland provides additional geographical diversification reducing concentration risk.

By building out ancillary lines such as insurance consulting and investment banking advisory—services frequently demanded by high-net-worth clients—FOFA aligns itself closer to broader wealth management ecosystems rather than narrowly defined accounting vendor roles.

Risks and Execution Challenges: Liquidity, Integration, and Competition

Liquidity constraints are evident given a current ratio of 0.85, reflecting a tighter working capital posture that may limit flexibility deploying capital towards further acquisitions or hiring needed integration resources without additional financing support [F1]. Managing cash flow timing especially relative to earn-out obligations on recent purchases will be critical.

Integration risk commands attention given the complex nature of consolidating distinct CPA entities which are relationship-driven businesses deeply reliant on trusted advisors retained post-acquisition. Failure to maintain consultant engagement or disrupt service quality could trigger client losses damaging projected revenue synergies.

Competitive intensity also poses threats: fee compression potential exists amidst numerous alternatives including lower-cost virtual accounting providers enabled by technology. In wealth management verticals, entrenched incumbents improve digital offerings placing pressure on newer platforms like FOFA's which must demonstrate clear value-add beyond price.[S1]

Key Milestones and Market Indicators to Monitor

Stakeholders should track quarterly earnings releases for organic growth trends within newly acquired units such as Benson Family Office assets and FO Maryland operations capturing same-store sales momentum post-integration [S2][S9].

Client retention rates among acquired consultants remain paramount; successful transitions evidenced by stable or increasing recurring revenues validate acquisition strategy execution.

Adjusted purchase price reconciliations based on actual financial performance during measurement periods will shed light on underlying profitability and cash flow impacts tied directly to transactional structures detailed in the agreements [S7][S9].

Pipeline visibility regarding new acquisition targets or signed agreements can signal sustainability of growth trajectory beyond one-time deals.

Latest Financial Position and Metrics Snapshot

Latest financial snapshot

| Metric | Value | Period |

|---|---|---|

| Total debt | $507750 | |

| 2026-03-31 | ||

| Net debt | $507750 | |

| 2026-03-31 | ||

| Current assets | $668579 | |

| 2026-03-31 | ||

| Current liabilities | $787182 | |

| 2026-03-31 | ||

| Current ratio | 0.85x | |

| 2026-03-31 |

Source: SEC companyfacts cache [F1].

Financially, FOFA exhibits early-stage characteristics rooted in active investment cycles supporting platform build-out rather than profitability benchmarks yet. Negative income metrics reported historically are consistent with burgeoning operational expenses tied to acquisitions though not restated specifically this quarter [F1].

No material litigation or contingent liabilities have been disclosed adding some stability amid ongoing business transformation efforts [S6].

This analysis synthesizes information through the latest SEC filings emphasizing operational shifts as opposed to prescribing investment views. Business fundamentals pivot around demographic-driven acquisition opportunities coupled with integrated family office offerings competing vigorously against established industry players under tighter liquidity conditions.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments