FRP Holdings Balances Diversified Real Estate Growth Against Elevated Interest Costs and Development Risks

FRP Holdings pursues growth across industrial, multifamily, development, and mining segments with a capital-intensive model amid rising expenses and competitive pressures.

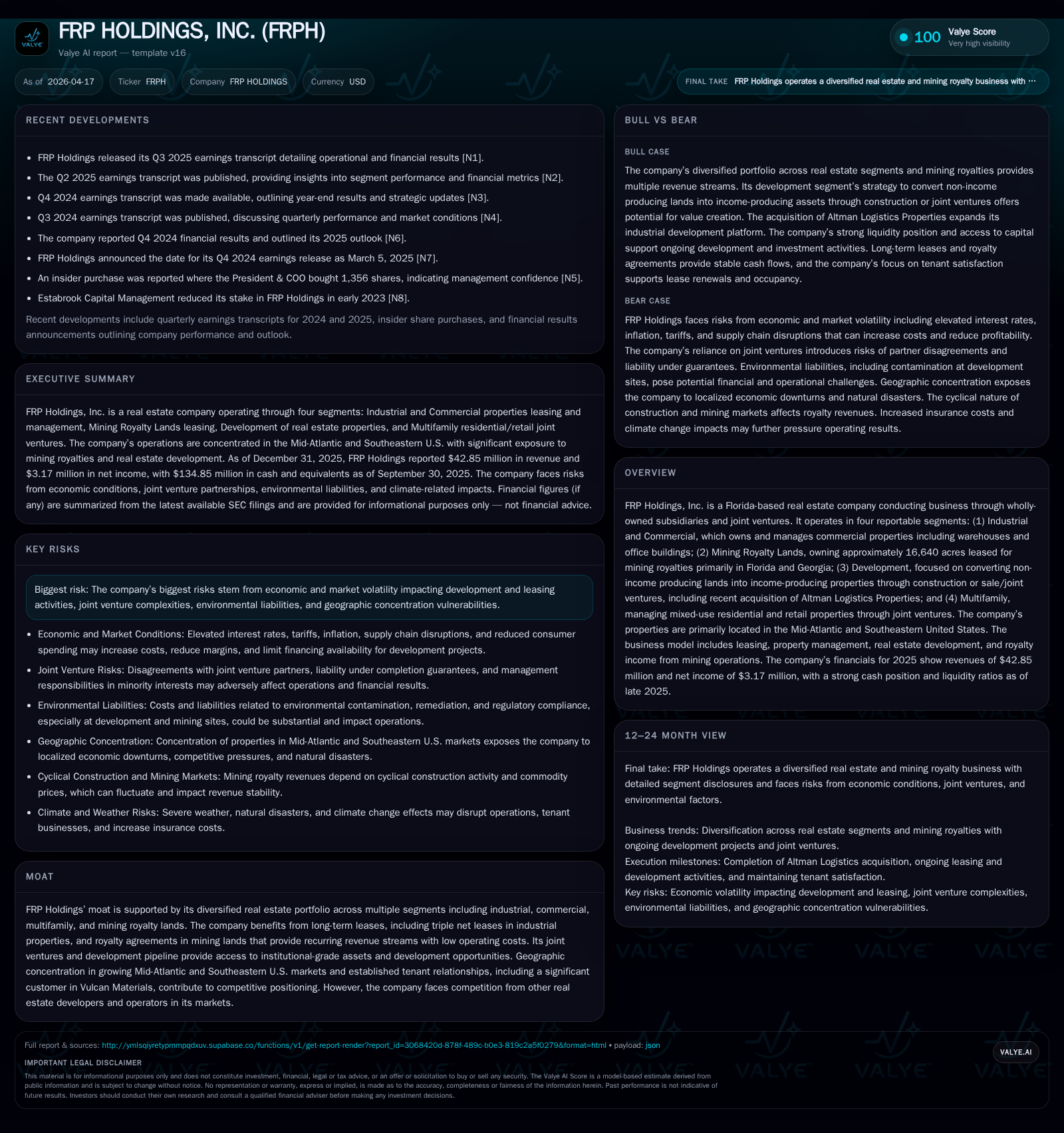

FRP Holdings operates through four main segments—industrial & commercial, mining royalty lands, development, and multifamily—primarily in the Mid-Atlantic and Southeastern US. Its diversified real estate portfolio benefits from long-term leases, stable royalty income, and ongoing development projects including recent acquisitions. Although revenue grew modestly by 2.6% in 2025, operating income declined 40%, with net income dropping nearly 48% due to increased expenses related to acquisitions and higher general administrative costs. The company maintains strong liquidity but faces negative free cash flow driven by sizable capital expenditures on development projects. Key risks include economic volatility affecting tenant demand and financing availability, exposure to a major tenant in the mining segment, and rising construction and labor costs.

Company Overview

FRP Holdings, Inc., headquartered in Florida, is a real estate company operating primarily in the Mid-Atlantic and Southeastern United States. The business is organized into four reportable segments: Industrial & Commercial properties comprising warehouses and office buildings; Mining Royalty Lands spanning approximately 16,640 acres leased mostly for extraction activities; a Development segment focused on transforming non-income producing land into income-producing real estate through construction or sales/joint ventures; and Multifamily operations managing mixed-use residential/retail properties via joint ventures [S1][S2][S11].

Historical Financial Performance

From 2022 through 2025, FRP Holdings saw top-line growth from $37.5 million to $42.8 million, reflecting a compound average annual growth rate just above 4%. Specifically, revenue grew modestly by 2.6% in the latest fiscal year ending December 31, 2025 [F1].

However, operating income exhibited volatility: it more than doubled from $8.0 million in 2022 to peaks around $11.7 million in both 2023-24 before contracting sharply by about 40% to $7.0 million in 2025. Net income mirrored this trend with a peak near $6.4 million in 2024 declining almost 48% to $3.3 million last year [F1].

The earnings contraction primarily stems from one-time acquisition expenses related to the Altman Logistics platform purchase completed October 2025 (~$2 million), alongside heightened general & administrative (G&A) expenses attributed to an executive succession plan initiated mid-2024 [S2][S24]. Industrial segment profitability was also pressured by increased depreciation following completion of new warehouse assets plus lower occupancy resulting from tenant defaults or non-renewals [S24].

Operating cash flow has held relatively steady despite these earnings swings—hovering near $29 million annually—and remains robust versus net income as a result of non-cash charges such as depreciation [F1][S13]. Yet free cash flow (operating cash flow minus capex) continues negative due to aggressive reinvestment: capex nearly doubled year-over-year exceeding $51 million in both 2024-25 compared with roughly half that amount two years prior [F1].

Historical performance (annual)

| FY | Rev ($mm) | Net ($mm) | CFO ($mm) | OpInc ($mm) | Rev YoY | Net YoY |

|---|---|---|---|---|---|---|

| 2025 | 43 | 3 | 30 | 7 | +2.6% | -47.8% |

| 2024 | 42 | 6 | 29 | 12 | +0.6% | +20.4% |

| 2023 | 42 | 5 | 33 | 12 | +10.7% | +16.1% |

| 2022 | 37 | 5 | 22 | 8 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | Buybacks ($mm) | FCF ($mm) | ROE% |

|---|---|---|---|

| 2025 | 0 | -21 | 0.8 |

| 2024 | 0 | -22 | 1.5 |

| 2023 | 2 | 22 | 1.3 |

| 2022 | 0 | -5 | 1.1 |

Source: SEC companyfacts cache [F1].

Segment Insights

Industrial & Commercial

This segment owns warehouses and office buildings located mostly in Maryland and Florida including recently completed speculative warehouses such as the Chelsea project (moved from development segment upon completion). Leases often feature triple-net terms providing stable cash flow with most tenant expenses borne separately by lessees [S11][S25]. Occupancy rates experienced some declines recently due to specific tenant defaults and non-renewals contributing to an operating profit decline of approximately $1 million year-over-year [S24][N2].

Mining Royalty Lands

Mining royalties from leases on roughly sixteen thousand acres provide high-margin recurring revenue streams since operational risks lie with tenants like Vulcan Materials who accounted for about 26% of FRP’s consolidated revenue in 2025—introducing notable concentration risk should any material disruption occur [S11][S19]. Royalties are based on tons mined multiplied by price benchmarks with minimal direct costs borne by FRP apart from taxes at non-leased properties.

Development Segment

Focused on converting idle land into rentable or saleable assets through new construction or joint ventures—the segment includes diverse projects like residential lots in Harford County MD or industrial warehouses via recently acquired Altman Logistics Properties LLC platform that expanded FRP’s footprint significantly in Florida logistics real estate [S11][S10][S26][N3]. The Altman deal brought new institutional-grade industrial developments under construction expected for completion mid-2026 and beyond while adding near-term acquisition-related expenses totaling around $2 million impacting earnings last year [N3][S24]. Substantial ongoing capital deployment supports this growth strategy with ~$73 million planned investments continuing over near term funded through available liquidity plus partner contributions.

Multifamily Segment

Through joint ventures owning residential apartments paired with retail spaces primarily concentrated in Washington DC and Greenville SC markets—leasing terms typically range from one-year apartment leases with month-to-month renewals up to long-dated retail leases spanning over a decade including percentage rent components tied to tenant sales performance enhancing upside capture from high-performing retail tenants [S21]. The segment includes consolidated ventures such as Dock79 and The Maren partnerships contributing stable rental streams.

Capital Structure & Liquidity

FRP maintains substantial liquidity with approximately $135 million cash equivalents reported at June-September quarter-end enabling funding of active development pipelines without urgent refinancing needs if market conditions shift unfavorably [F1][S15][S18].

Total consolidated debt is about $194 million consisting largely of fixed-rate loans ($180 million at average ~3%) predominantly secured by major multifamily assets like Dock79 plus floating rate loans tied to SOFR indices for construction financing ($14 million). Variable-rate exposure introduces moderate interest rate sensitivity though mitigated partially via interest rate swaps or rate caps implemented on certain borrowings creating predictable interest cost ceilings around high single digits for near term loans [S1]. As SOFR increases by one basis point annualized interest expense rises roughly by $40,000 indicating moderate variable rate debt sensitivity.

In addition to conventional mortgages FRP uses joint venture equity contributions plus partner capital calls typical of real estate developers focused on institutional quality projects which help share financial risks but require coordination regarding timing of capital calls and distributions especially amid volatile market cycles.

Capital Allocation & Returns

The company’s historical dividend payouts have been sporadic; recent buybacks were minimal (~$464k in FY25), suggesting surplus capital remains invested preferentially into growth initiatives rather than returning cash aggressively to shareholders so far [F1].

Return on equity approximates below one percent (0.8%) driven down mainly by depressed net earnings relative to equity base over $420 million reflecting sizable land holdings evaluated at cost plus accumulated investments rather than cyclical earnings power alone [F1]. This underscores the capital-intensive nature of their business model typical among diversified property holding companies investing significantly upfront with longer payback horizons.

Growth Prospects & Outlook

FRP's growth depends heavily on executing its ambitious pipeline—including completion of industrial/logistics facilities associated with the Altman acquisition expected end-Q2 2026—and incremental leasing success within existing and newly developed properties across segments [N3].

Multifamily expansion projects like the Woven joint venture underway in Greenville SC aim to capitalize on regional population growth trends supported by targeted tax credits boosting financial feasibility [S10].

Mining royalty lands offer potential “second lives” where exhausted sites can be repurposed for mixed-use residential developments contingent on zoning approvals currently underway particularly notable examples being Brooksville FL site planned for over five thousand housing units [S16][S19].

However elevated borrowing costs from recent interest rate hikes limit favorable financing windows for refinancings or new project leverage increasing hurdle rates challenging investment returns [S1]. Also ongoing inflationary pressures raise raw material prices (e.g., steel, lumber) and labor expenses posing margin headwinds for development builds [S14].

Lease renewals remain a focus area given competition forcing price concessions particularly within industrial parks where institutional landlords are active catering aggressively priced Class A product offering flexible lease structures.

Risk Factors Summary

- Heavy geographic concentration exposes FRP particularly in Mid-Atlantic and Southeastern U.S markets which might incur region-specific risks such as hurricanes or economic downturns impacting tenants’ ability to pay rents or maintain operations.

- Reliance on few key tenants notably Vulcan Materials amplifies counterparty risk if any lease interruptions arise.

- Rising interest rates increase cost of capital pressuring net yields especially on floating-rate construction loans pending rollover into fixed permanent financing [S14].

- Construction delays or higher than anticipated costs could defer projected rental streams stretching out timelines impacting liquidity.

- Joint venture arrangements require complex coordination; misalignment with partners may affect operational decisions affecting asset optimization.

- Regulatory risk surrounding environmental matters tied to mining lands reclamation obligations though typically managed under lessee responsibility caveat exists.

Conclusion

FRP Holdings embodies a multi-pronged real estate platform leveraging diversification across industrial/commercial properties, mining royalties, multifamily residential ventures, and active land development converting latent assets into monetizable income streams. While steady revenue progression underscores inherent resilience within its portfolio mix alongside long-term lease commitments, underlying profitability compression signals elevated near-term expense burdens primarily linked to strategic acquisitions and executive transitions. Capital absorption remains substantial reflecting commitment towards expansion platforms especially logistics-focused warehouses integral amid evolving supply chain imperatives attracting institutional demand. Liquidity appears ample providing operational runway but macroeconomic dynamics warrant close monitoring notably financing conditions influencing project yield viability alongside market leasing fundamentals. Collectively, FRP must balance growth investment rigor against execution risks amidst competitive leasing environments alongside cyclical exposure inherent within commodity-linked royalties shaping future financial trajectory.

This analysis synthesizes SEC filings, earnings transcripts, recent disclosures, industry context considerations but does not constitute investment advice.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments