Splash Beverage Group’s Revenue Collapse and Strategic Pivot in 2025

A sharp revenue contraction in 2025 has compelled Splash Beverage Group to pursue a transformative acquisition targeting the cannabinoid wellness sector.

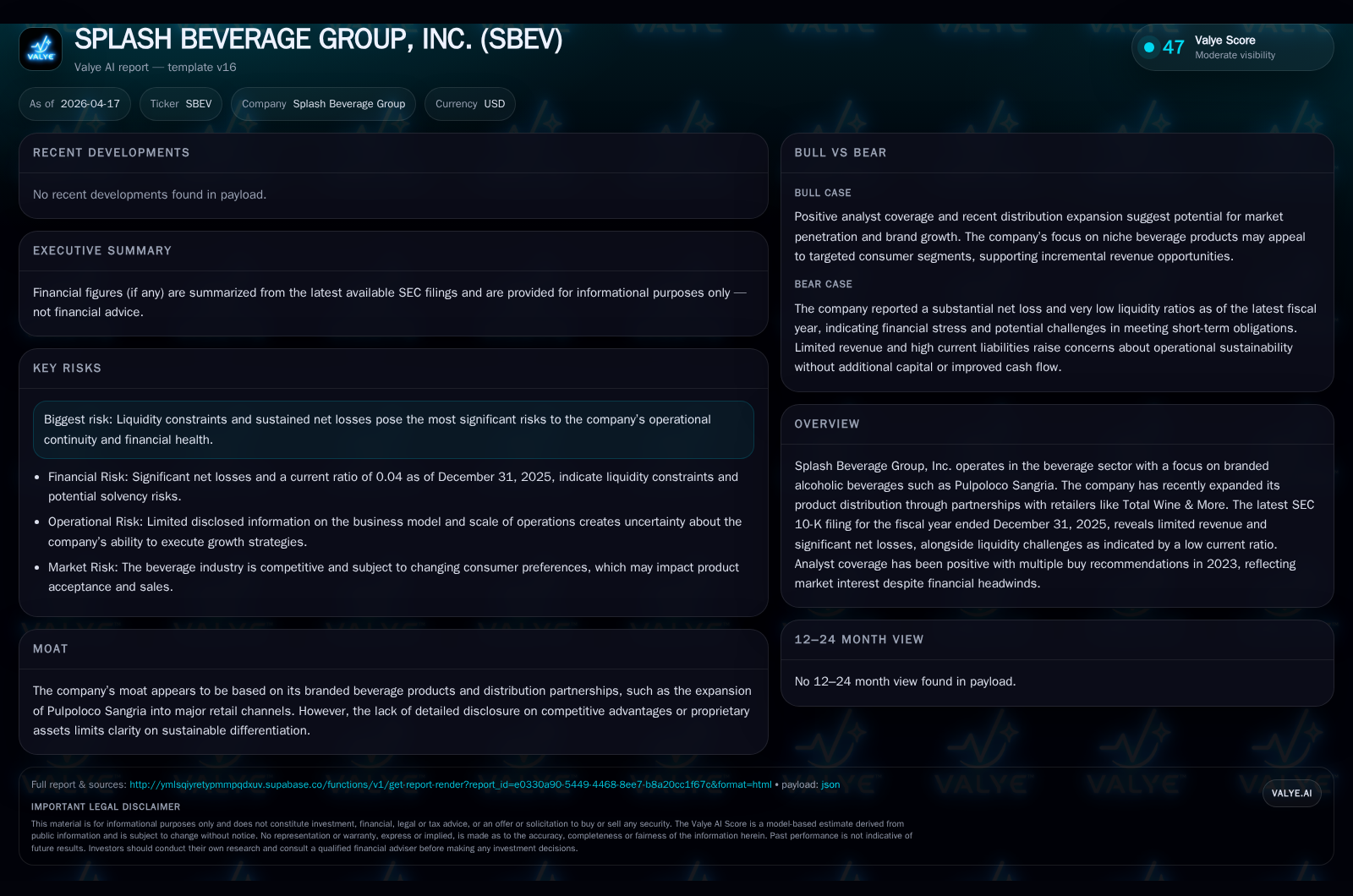

Splash Beverage Group, historically a brand portfolio player in alcoholic beverages, witnessed a dramatic revenue collapse of over 98% in FY2025 compared to FY2024, coupled with persistent high operating losses and severely strained liquidity. Faced with a going concern warning and delisting risk, the company is shifting its business model through a planned acquisition of Medterra CBD, signaling a strategic pivot into federally compliant cannabinoid wellness products. The success of this transition hinges on effective capital raises and integration, while ongoing net losses and litigation pose substantial risks.

From Brand Management to Revenue Freefall: Tracing Splash Beverage’s Recent Performance

Splash Beverage Group traditionally pursued growth by managing a portfolio of branded alcoholic beverage products. However, FY2025 marked a near-complete revenue collapse with reported sales shrinking dramatically from $4.15 million in FY2024 to merely $73,066 by year-end 2025—a decline of approximately 98.2% [F1]. Operationally, this revenue freefall reflects severe SKU portfolio attrition and the effective cessation of core beverage sales for much of 2025 due to capital shortages that curtailed production and distribution capabilities [S1]. The company did report limited delivery of tequila product sales beginning March 2026 [S1], indicating nascent efforts to revive top-line activity.

Historic Financial Trends: Revenue Collapse Amid Persistent Operating Losses

Despite shrinking revenues, operating expenses remained largely fixed or only marginally scaled down, resulting in sustained heavy operating losses totaling approximately -$14.2 million in FY2025 [F1]. While this represented an 11.6% improvement from the prior year's -$16 million operating loss—primarily due to reduced sales-related costs—the company continues to operate deeply underwater on an operational basis. Negative operating leverage intensified as fixed cost burdens were disproportionately high relative to plummeting sales volumes.

Cash Flow Challenges and Deteriorating Liquidity Ratios: Warning Signals from the Balance Sheet

Liquidity indicators illustrate a dire financial position entering calendar 2026. As of December 31, 2025, total cash and equivalents stood at just $281K versus current liabilities exceeding $16.26 million—a current ratio of only 0.04 [F1]. Operating cash flows were significantly negative at -$4.82 million during FY2025 but showed some improvement versus prior years’ cash burn—still far above sustainable levels [F1]. Auditors have explicitly flagged these liquidity deficiencies in their opinion paragraphs citing substantial doubt about Splash's ability to continue as a going concern without additional financing [S1]. This underscores a working capital crunch and an unsustainable burn rate binding Splash until fresh capital becomes available.

Capital Structure Maneuvers Amid Funding Gaps: Debt Instruments and Equity Concerns

To address funding challenges due to equity issuance difficulties, Splash converted certain equity issuance obligations into promissory notes bearing no interest unless default occurs (then capped at 10% per annum) maturing in January 2028 [S4][S5]. Amendments to equity lines of credit include mandatory prepayments tied to new equity proceeds but add complexity around dilution management [S6]. These steps aim to preserve liquidity flexibility without triggering immediate dilutive events but introduce refinancing risk.

Pivoting Strategy: Letter of Intent for Medterra CBD Acquisition as Growth Catalyst

On March 4, 2026, Splash entered into a non-binding letter of intent for acquiring Medterra CBD LLC—an established operator within the federally compliant cannabinoid wellness industry with over two million customers nationally and internationally [S3][S17]. The transaction values Medterra at an enterprise value of $37.6 million through issuance of approximately 75 million common shares plus convertible preferred shares (Series X and X-1) convertible at $0.50 per share [S17]. Approximately one-fifth (19.99%) of common stock will transfer directly at closing; remaining equity is structured via protective preferred instruments with conversion rights.

This marks a fundamental business model shift into cannabinoid wellness products—a sector blending health & wellness trends with consumer packaged goods dynamics. The deal requires raising roughly $10.4 million in cash at close for Medterra’s debt repayment plus coverage for income taxes related to ownership transfers [S17]. This diversification may offer growth avenues absent in Splash’s struggling beverage segment.

Risks on the Horizon: Continued Net Losses, Delisting Threats, and Litigation Exposure

Recurring heavy net losses reached -$25.2 million in FY2025 despite lower expenses commensurate with collapsed sales levels [F1]. The company faces NYSE American delisting risk triggered by failure to meet minimum stockholders’ equity requirements ($6 million threshold) with negative equity around -$15.3 million by end-2025 [F1][S1]. Appeals are pending linked closely to Medterra deal closing and resultant equity injection.

Legal risks include ongoing litigation from TapouT LLC over breach allegations on licensing agreements dating back over a decade—with damages possibly exceeding $1.7 million though management has reserved about $330K based on mediation outlooks [S1]. This adds financial uncertainty amid tenuous operating stability.

Capital Allocation Overview: Returns, Dividends, Buybacks Absent Amid Financial Strain

Historical returns have been negative due to prolonged operational deficits compounded by eroding equity value resulting in an estimated negative return on equity nearing -165% at FY2025 close [F1]. Negative free cash flow generation confirms no discretionary distributions such as dividends or share buybacks have been feasible or declared recently [F1], reflecting prioritization of survival financing strategies.

Historical performance (annual)

| FY | Rev ($mm) | Net ($mm) | CFO ($mm) | OpInc ($mm) | Rev YoY | Net YoY |

|---|---|---|---|---|---|---|

| 2025 | 0 | -25 | -5 | -14 | -98.2% | -6.2% |

| 2024 | 4 | -24 | -8 | -16 | -78.0% | -13.1% |

| 2023 | 19 | -21 | -10 | -15 | +4.2% | +3.2% |

| 2022 | 18 | -22 | -14 | -21 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | ROE% |

|---|---|

| 2025 | 164.9 |

| 2024 | 127.5 |

| 2023 | 374.7 |

| 2022 | -232.7 |

Source: SEC companyfacts cache [F1].

Negative numbers shown in parentheses for clarity; steep decline in revenues contrasts modest improvements in loss figures.

This analysis synthesizes publicly filed financial data through April 17th, 2026 ([F1], [S#]) alongside regulatory disclosures regarding strategic transactions shaping Splash Beverage Group's evolution during an especially challenging fiscal period.

Disclaimer: This report is intended solely for informational purposes based on publicly available data up to April 17th; it does not constitute investment advice or recommendations regarding securities or market activities related to Splash Beverage Group.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments