Western Uranium & Vanadium Corp. Advances Processing Amid Capital and Market Volatility

The company balances ramping its unique Kinetic Separation technology with ongoing funding requirements and volatile uranium markets.

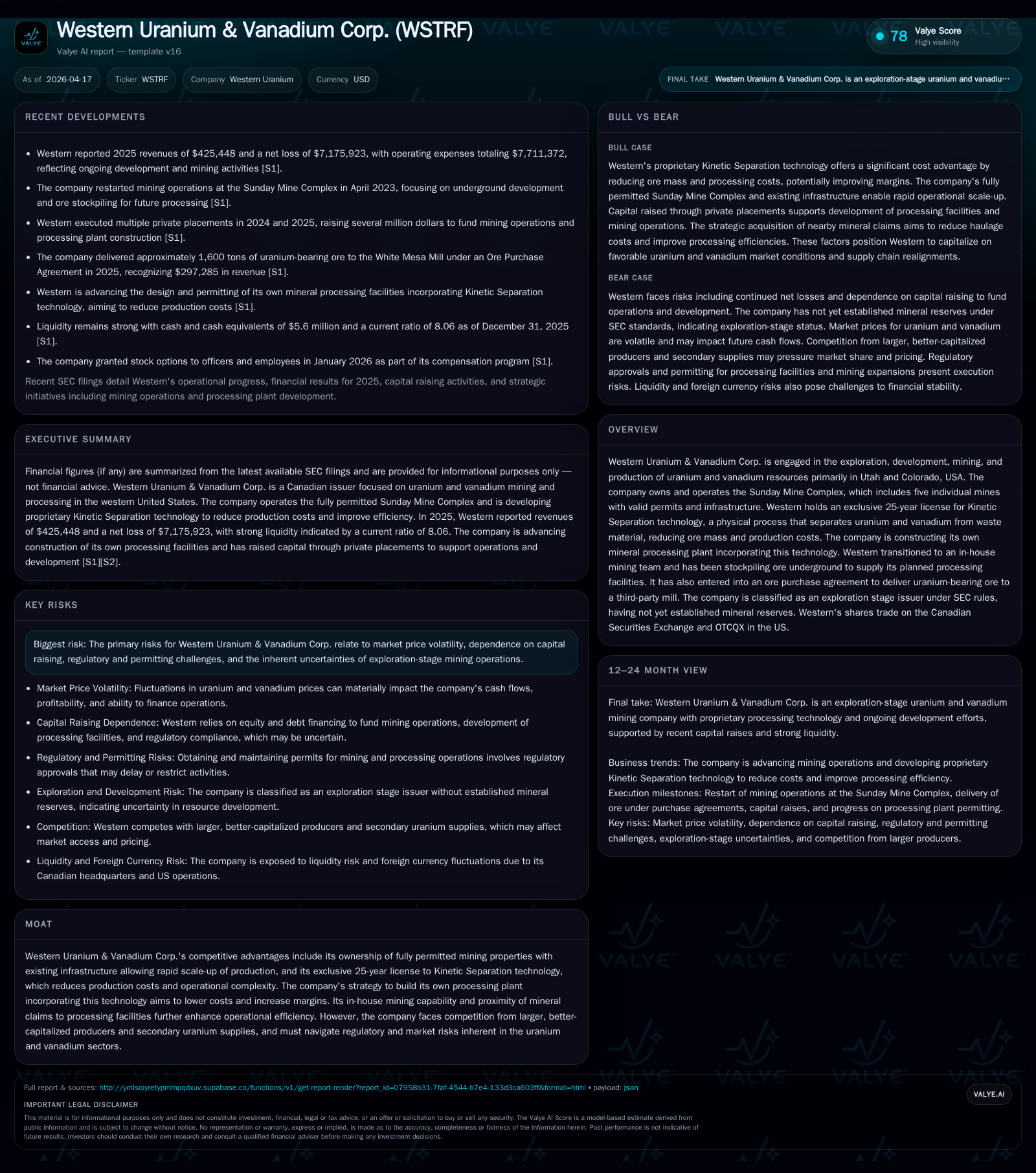

Western Uranium & Vanadium Corp. maintains operations centered on its fully permitted Sunday Mine Complex in Colorado, alongside developing proprietary Kinetic Separation processing capabilities aimed at reducing costs. Despite revenue growth in 2025, the firm continues to operate with persistent net losses and negative cash flow, relying heavily on equity financings to sustain development efforts. Its capital allocation priorities focus on advancing the Mustang Mineral Processing Plant while navigating uranium market uncertainties and regulatory risks intrinsic to mining ventures.

Business Overview and Historical Context

Western Uranium & Vanadium Corp. focuses on exploration, development, mining, and production of uranium and vanadium primarily within Utah and Colorado. Its core asset is the Sunday Mine Complex (SMC), comprising five individual mines all holding valid permits and established infrastructure facilitating expedited production scaling [S1]. Since acquiring these assets from Energy Fuels Holding Corp in 2014, the Company has worked toward reviving mining operations interrupted years prior. Low-cost operational advantages derive partly from proximity of claims, infrastructure access, and its proprietary Kinetic Separation technology licensed exclusively for 25 years, which physically separates uranium and vanadium from waste material, aiming to lower ore mass processed and reduce expenditures [N/A overview]. The current strategy involves constructing the Mustang Mineral Processing Plant incorporating this technology to improve margins.

Financially, Western remains an exploration-stage issuer under US SEC rules [S1]. Historical performance shows limited revenues primarily from oil and gas lease royalties alongside nascent mineral outputs. For fiscal year 2025, revenues increased materially to $425K from $184K in 2024, linked mainly to expanded mining activities and resource monetization steps [F1]. However, operating losses have persisted as significant investment is still directed at mine development, technology licensing, mill construction, and general administrative functions.

Historical performance (annual)

| FY | Rev ($mm) | Net ($mm) | CFO ($mm) | OpInc ($mm) | Rev YoY | Net YoY |

|---|---|---|---|---|---|---|

| 2025 | 0 | -7 | -6 | -7 | +131.5% | +29.0% |

| 2024 | 0 | -10 | -8 | -10 | -57.4% | -104.6% |

| 2023 | 0 | -5 | -4 | -5 | -94.5% | -592.5% |

| 2022 | 8 | -1 | 5 | -1 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | ROE% |

|---|---|

| 2025 | -23.7 |

| 2024 | -33.9 |

| 2023 | -16.1 |

| 2022 | -2.4 |

Source: SEC companyfacts cache [F1].

Note: Capex for recent years not consistently reported; allocation focused on mill construction.

The company generated operating losses exceeding $7 million in FY2025 but improved compared to over $10 million loss in FY2024. Operating cash flow remained negative at approximately $5.8 million reflecting expenditures sustaining operations and development activities [F1]. No dividends or share buybacks were executed during this period despite authorization of a normal course issuer bid initiated December 19, 2025; management cites prioritizing cash retention amid funding needs [S1][S3].

Growth Drivers and Operational Progress

Western’s primary growth catalyst centers on advancing its Kinetic Separation-enabled Mustang Mineral Processing Plant designed to process uranium-vanadium ores efficiently with lower capital intensity than traditional milling methods . Ownership of fully permitted mines allows relatively rapid operational scale-up once processing facilities become operational.

In addition to internal mining teams working underground stockpiles at SMC to feed planned processing capacity steadily , the Company has also secured ore purchase agreements with third-party mills as an interim measure pending Mustang Plant commissioning . These operational synergies leverage technological advantages alongside lowered logistic complexity due to site proximity.

The exclusive license model for Kinetic Separation locked in for a quarter-century provides a potentially durable competitive edge against traditional mill operators through cost savings that should translate into better margins if market conditions support profitable commercial processing .

Nevertheless, near-term growth depends heavily on successfully constructing and commissioning the processing plant as well as securing continued financing for these capital projects. Market volatility in uranium prices directly affects cash flow potential once production ramps up . Regulatory approvals remain essential unknowns; delays or cost overruns could cap expansion prospects.

Financial Position and Capital Allocation

As of December 31, 2025, Western held approximately $5.6 million in cash and equivalents with a strong current ratio exceeding 8x owed largely to deferred liabilities [F1]. Working capital stood at about $6.1 million versus current liabilities near $0.76 million indicating near-term solvency buffers but still constrained resources relative to scale ambitions.

The Company continued raising equity in recent years via multiple brokered private placements combining gross proceeds exceeding CAD $11 million across late 2024 through late 2025 periods [S6][S13]. For example:

- June 13, 2025 private placement raised roughly $3.7 million USD (CAD $5M) [S1]

- October 14, 2025 offering brought an additional ~$4.2 million USD (CAD $5.9M) [S1]

- November 2024 financing added about $3.9 million USD (CAD$5.46M) [S6]

Proceeds support construct of the Mustang Plant along with scaling mining operations at SMC. Despite available funds today management signals fiscal discipline balancing shareholder returns: although authorized under NCIB program to repurchase up to ~10% public float shares through Dec '26 timeframe no purchases occurred through FY2025 reflecting prudent cash deployment choices given uncertain market dynamics and developmental stage [S3][S4].

Asset retirement obligations linked with reclamation activities are recognized liabilities totaling over $1.18 million gross value as of year-end precluding any overlooked future cleanup costs; part relate specifically to mines under active reclamation like Van 4 Mine where surety reductions were recently approved by authorities after reclamation milestones met [S9][S22][S24].

Industry Context and Risk Factors

Uranium's primary commercial use remains as nuclear reactor fuel critical for electricity generation globally. The sector is witnessing increased political support amid decarbonization pressures pushing new reactor builds alongside technology innovations driving demand fundamentals higher over medium-long term horizons . Conversely, the Company must grapple with uranium price volatility compounded by geopolitical factors such as U.S.-Russia trade sanctions affecting supply chains negatively impacting pricing stability [S27].

Smaller producers face challenges competing with incumbent large-scale miners benefiting from economies of scale and greater financial firepower amid complex permitting environments requiring extensive environmental compliance attention notably within U.S. jurisdictional frameworks governing restoration obligations given legacy mine footprints.

Capital raising dependence remains pivotal given Western’s exploration stage status without sustained positive operating cash flows; failure to secure timely funds risks delaying or downsizing development plans undermining future growth trajectories [S6][S28]. Legal risks appear low currently with no material litigation but routine regulatory inspections persist as operational overheads contributing non-trivial compliance expenditures [S5].

Outlook Considerations

Explicit company guidance is limited but milestones worth monitoring include:

- Completion timeline progress of Mustang Mineral Processing Plant commissioning,

- Regulatory clearance updates notably around Kinetic Separation full licensing utilization,

- Ore stockpile drawdown rates feeding processing capacity,

- Future financing rounds terms shaping liquidity profile,

- Uranium market price trajectory influencing potential commercial viability,

- Any further share repurchases under NCIB providing hints of management confidence.

Operationalizing proprietary separation technology combined with permitted assets constitutes a differentiated proposition if execution succeeds amid sector volatility. However notably Western Uranium & Vanadium continues generating net losses limiting immediate return on equity reflected by approximately -24% ROE calculated for FY2025 using net income against equity figures reported [F1]. Cash burn reductions observed from prior years signify partial operational tightening but sustainable profitability remains distant.

Conclusion

Western Uranium & Vanadium Corp epitomizes a junior miner investing heavily in technical innovation and asset development designed for niche market advantage within uranium/vanadium sectors enmeshed in regulatory rigor. Accelerated revenue growth juxtaposed with persistent losses highlights developmental operating phase realities typical for early-stage miners transitioning toward production phases. Strong permitting status coupled with exclusive proprietary processing exposure are strategic advantages masked currently by capital intensity demands and cyclic sector risks stemming from price fluctuations plus geopolitical uncertainties. Prudence around managing liquidity reserves alongside timing access to project milestones will dictate near-term feasibility for delivering on ambitious production ramp goals set by management.

This report incorporates information available as of April 17, 2026 from official SEC filings and company disclosures; it does not constitute investment advice or recommendations.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments