Constellation Acquisition Corp I’s Path to NASDAQ: Unlocking Value through US Elemental

Examining CSTAF’s financial constraints as a SPAC and its transformative business combination plan with US Elemental in the lithium sector.

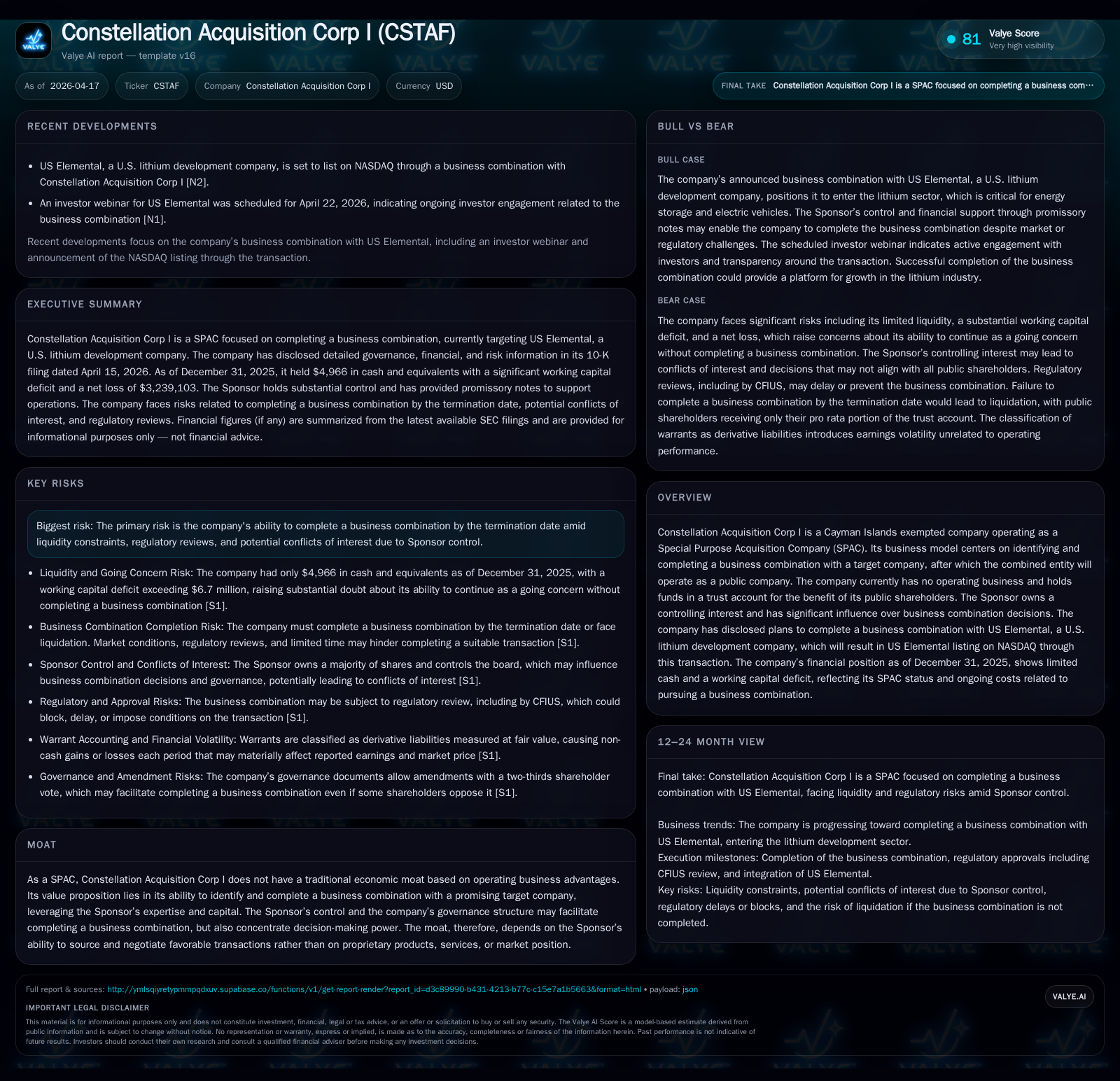

Constellation Acquisition Corp I (CSTAF) faces acute liquidity pressures and operating losses characteristic of a Special Purpose Acquisition Company approaching its mandatory liquidation deadline. Its path forward hinges on the successful execution of a business combination with US Elemental, a U.S.-based lithium development company targeting NASDAQ listing. While historical financials reveal deteriorating cash flows and mounting deficits, the strategic pivot towards lithium development positions CSTAF at the intersection of growing EV battery demand and ESG-focused mineral sourcing. Sponsor influence and governance present typical SPAC risks, underscoring the importance of milestone tracking as CSTAF approaches critical regulatory and shareholder decision points.

SPAC Model and Financial History: An Overview of Performance and Challenges

Constellation Acquisition Corp I operates as a Cayman Islands exempted company structured explicitly as a Special Purpose Acquisition Company (SPAC). This vehicle's core function is to pool public capital in trust while seeking a target private company for merger. CSTAF’s financial history underscores this archetype: it reports no revenue-generating operations but incurs administrative and acquisition pursuit costs reflected in persistent operating losses. According to [F1], CSTAF posted operating losses of approximately -$1.07 million in FY2025, an improvement from -$1.57 million in FY2024 and significantly narrowed compared to -$3.56 million in FY2023. This positive trend likely reflects cost management as the company advances toward its intended business combination.

However, increased net losses tell a more nuanced story. Net income plummeted to -$3.24 million in FY2025 from -$0.25 million in FY2024, largely attributable to escalating expenses tied to due diligence, legal fees, advisory services, and transaction-related outlays aimed at consummating the business combination. Operating cash flow remains negative (-$470k in FY2025), though it improved relative to previous years’ steeper outflows ([F1]). These figures paint a picture common for late-stage SPACs: controlling overhead while expending resources to seal a deal before expiration.

Historical performance (annual)

| FY | Net ($mm) | CFO ($) | OpInc ($mm) | Net YoY |

|---|---|---|---|---|

| 2025 | -3 | -470238 | -1 | -1204.8% |

| 2024 | 0 | -753238 | -2 | +31.1% |

| 2023 | 0 | -1333630 | -4 | -102.8% |

| 2022 | 13 | -444415 | -1 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | Buybacks ($mm) | ROE% |

|---|---|---|

| 2025 | 27 | 13.9 |

| 2024 | 24 | 1.3 |

| 2023 | 269 | 2.0 |

| 2022 | -103.1 |

Source: SEC companyfacts cache [F1].

Table: Constellation Acquisition Corp I Financial Snapshot (FY2022–FY2025) [F1]

Liquidity Crisis and Capital Structure Pressures Heading into Business Combination

The liquidity profile elucidated in CSTAF's latest reported period is dire: cash and equivalents stand at $4,966 against current liabilities nearing $9.9 million ([F1]). This yields a near-zero current ratio—a severe strain on CSTAF’s operational flexibility during what management acknowledges as the crucial runway preceding either business combination closure or mandatory liquidation ([S1] Item 1A Risk Factors).

Substantial doubt regarding CSTAF's ability to continue as a going concern was explicitly noted by its auditors due to these circumstances ([S1]). The scarcity of liquid assets heightens the urgency for completing the business combination before the termination deadline or securing alternative capital injections. Notably absent are indications that CSTAF currently holds committed external financing beyond sponsor support.

This structural stress stems partly from ongoing costs involved in searching for a suitable target entity amid volatile capital markets. The risk profile includes potential forced liquidation if the scheduled timeline lapses without transaction consummation ([S1]). Beyond liquidation risk lies dilution threat should CSTAF issue additional securities or debt instruments to fund completion or satisfy redemption obligations post-merger.

Strategic Rationale Behind Targeting US Elemental in the Lithium Development Space

CSTAF has disclosed intentions to merge with US Elemental—a U.S.-based lithium development company—in what would usher lithium assets onto NASDAQ under this transaction ([N1]). This pivot marks CSTAF’s transition from an empty shell balancing administrative expenses toward an operational entity embedded within fast-growing energy materials supply chains.

The strategic allure of US Elemental resides in lithium's rising importance as an essential mineral underpinning battery technologies predominantly employed in electric vehicles (EVs). Global demand forecasts anticipate sustained growth fueled by accelerating EV adoption dovetailed with tightening environmental regulation facilitating domestic mineral projects over imports—even more so amid geopolitical uncertainties influencing raw material supply stability ([N1]).

By effectuating this merger with US Elemental through a SPAC structure—a pathway offering expedited public market access compared to traditional IPO routes—CSTAF aims to capture value premised on expanding lithium resource development while leveraging ESG investor interest focused on American-sourced critical minerals.

Governance Dynamics and Sponsor Influence on Deal Execution and Risk Exposure

Governance disclosures reveal that CSTAF's Sponsor wields controlling interest with significant sway over decisions related to business combinations ([S1] Item 10 & Items on Conflicts of Interest). Unlike some SPACs adopting restrictive policies barring deals involving Sponsor affiliates to mitigate agency conflicts, CSTAF lacks explicit prohibitions preventing acquisitions of Sponsor-related businesses if deemed appropriate.

Such concentration of power can expedite deal execution through aligned incentives but also surfaces conflict risk between Sponsor objectives and public shareholders’ interests—especially regarding timing pressures leading up to liquidation deadlines ([S1]). The absence of clear administrative safeguards compounds these concerns.

In addition to potential misaligned motivations when evaluating target terms or valuation thresholds dictated by Sponsor imperatives rather than independent fiduciary oversight,[S1] cites scenarios where Sponsor-linked entities might compete for acquisition opportunities concurrently creating strategic tension within deal origination processes.

Evaluating Near-Term Milestones: Business Combination Timeline and Investor Communications

Investor engagement underscores rising focus on definitive merger milestones anchored around regulatory clearances and shareholder approvals ahead of mandated firewalls before consummation ([N2]). An updated investor webinar scheduled for April 22nd signals transparency efforts aligning stakeholders toward imminent events impacting trade sentiment.

Key forthcoming steps include finalizing definitive agreements regulatory filings with SEC reviews ensuring compliance with disclosure mandates alongside proxy statements related to shareholder vote procedures ([N2],[S3]). Market participants will watch carefully for any delays or modifications communicated by management that could presage renegotiations or fallback liquidation scenarios.

This calendar-centric scrutiny is characteristic for transactional SPACs confronting ticking-clock deadlines where incremental announcements predicate shifts in valuation expectations.

Capital Allocation Trends: Buybacks, Cash Flow Constraints and Implications for Shareholder Returns

Operating without active commercial revenue streams necessitates strict capital discipline within SPACs such as CSTAF; however historical data reveals heavy cumulative share repurchases totalling nearly $27.4 million in FY2025 alone ([F1]), continuing sizable buybacks from prior periods.

Coupled with substantial negative operating cash flows each year averaging several hundred thousand dollars low liquidity inherently constrains dividend distributions or any form of direct shareholder returns until combined operations stabilize post-merger.

Moreover,the company's shareholders' equity has deteriorated from negative $12.49 million in FY2022 steadily worsening to almost negative $23.26 million FY2025 boundaries reflective primarily of accumulated losses alongside transaction-related financial impacts ([F1]). This balance sheet erosion limits financial maneuverability further until notable asset accretion occurs through target incorporation.

Hence prospective investors should temper expectations on capital return prospects during this pipeline phase emphasizing focus instead on fundamental transformation achieved via closing the pending lithium sector deal.

Risks Around Completion and Market Volatility Amid Geopolitical Tensions Impacting Capital Raising Environment

Beyond CSTAF-specific operational hurdles lie broader macro risks highlighted candidly by disclosures painting complex geopolitical backdrops adversely affecting financial markets crucial for liquidity procurement ([S1] Risk Factors). The ongoing Russia-Ukraine war escalation alongside Middle Eastern conflicts inject pronounced uncertainty into debt-equity markets impacting ability both for sponsors/targets alike raise bridge financing or attract long-term investors.

Compounded here are intensifying tensions between China-Taiwan posing potential disruptions within supply chains central to battery metals technologies particularly relevant for companies like US Elemental following integration onto public markets via CSTAF ([S1]).

Such factors generate heightened volatility potentially delaying regulatory valuations or prompting shifts in investor appetite ultimately influencing strategic decision points around transaction timing or structure modifications expected imminently by stakeholders.

What to Watch Next: Key Metrics and Events for Stakeholders

Absent explicit management guidance on post-merger operational targets publicly disclosed thus far, attention naturally pivots toward monitoring concrete leading indicators:

- Trust account balances reflecting residual liquidity available pre-closing,

- Timeliness and substance of SEC filings concerning proxy circulars/prospectuses detailing merger terms,

- Outcomes from April 22 investor webcast signaling sentiment trajectory,

- Redeemable warrant exercises activity per OTC notices which may shift capitalization patterns ([S3]).

Given prevailing financial constraints juxtaposed with significant opportunity exposure through US Elemental’s lithium development project stakeholders face a critical observational window assessing whether this SPAC’s structural challenges yield viable platform establishment or default into wind-down mode.

DISCLAIMER: This analysis does not constitute investment advice or recommendations regarding securities ownership or transactions related to Constellation Acquisition Corp I (CSTAF). It presents an objective synthesis based solely on publicly available data sourced primarily from company filings [F1], SEC disclosures [S1,S3], and reputable market news outlets [N1,N2]. Readers should independently verify all information before making any investment considerations.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments