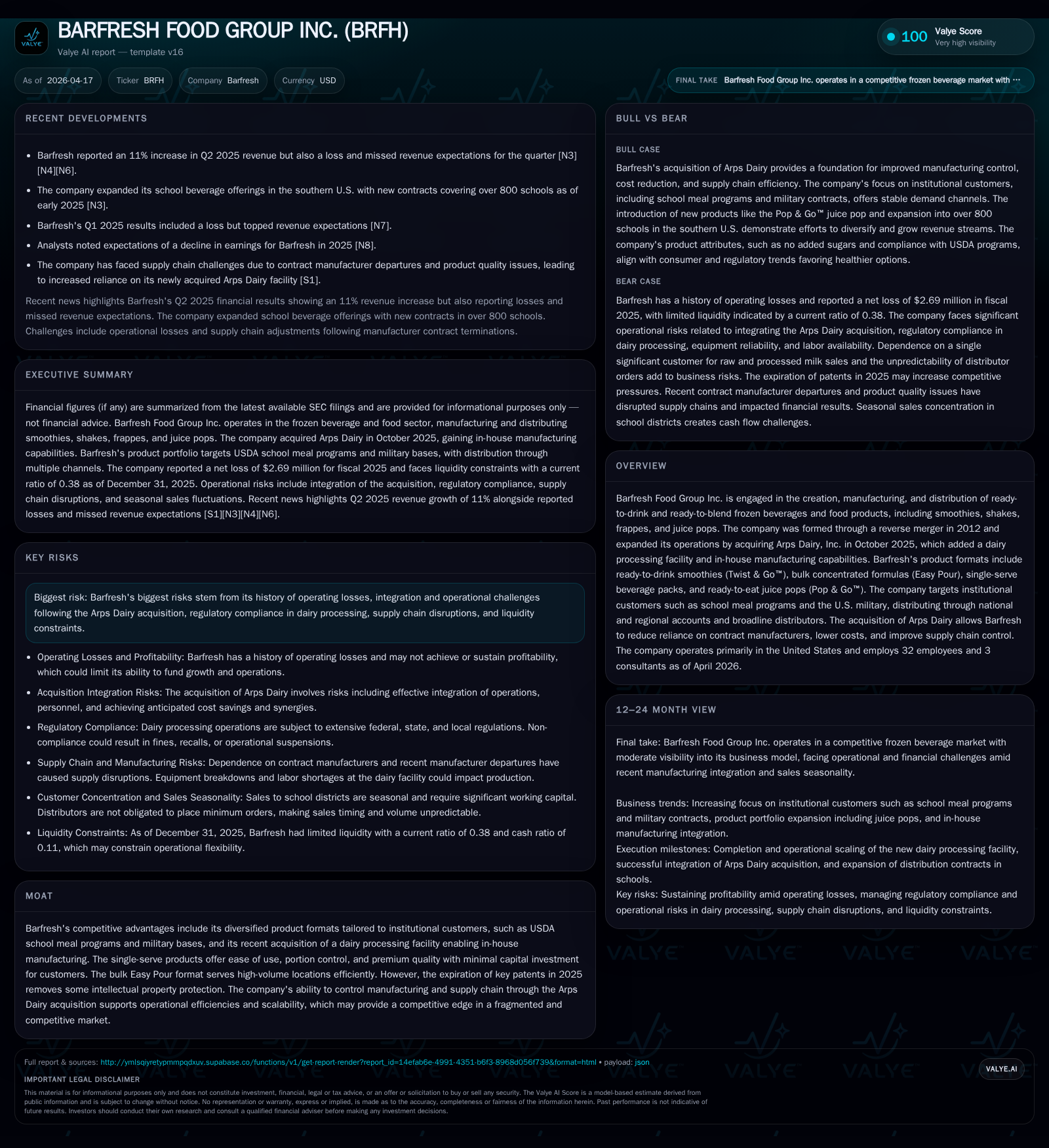

Barfresh Food Group Faces Growth Constraints and Operating Losses Post-Arps Dairy Acquisition

Barfresh leverages acquisition-driven vertical integration and diverse product formats to target institutional markets, yet profitability and liquidity remain significant challenges.

Barfresh Food Group Inc. specializes in ready-to-drink and ready-to-blend frozen beverages sold primarily to institutional accounts such as USDA school meal programs and the U.S. military. The company’s 2025 acquisition of Arps Dairy incorporated in-house manufacturing capabilities, aiming to reduce costs and enhance supply chain control. Despite these strategic moves, Barfresh continues operating at a loss, with liquidity and execution risks heightened by integration complexities, regulatory compliance in dairy processing, and supply chain disruptions. Capital expenditures mainly focus on expanding production capacity via a new facility targeted for completion in 2026. Watching for successful plant start-up, customer order trends, and working capital management will be key to assessing future operational improvements.

Company Background and Historical Growth

Barfresh Food Group Inc., post its formation through a reverse merger in 2012, has built its business around creating ready-to-drink and ready-to-blend frozen beverages including smoothies and shakes. The product lineup features proprietary offerings such as Twist & Go™ smoothies designed with no added sugars or preservatives, targeting institutional customers like the USDA school meal programs and the U.S. military [S10][S11]. In October 2025, Barfresh acquired Arps Dairy, which provided a strategic entry into owning manufacturing capabilities through a dairy processing facility. This acquisition marked a major shift from reliance on third-party contract manufacturers toward vertically integrated operations [S1][S15].

From a pure revenue perspective, Barfresh saw very strong growth acceleration; annual revenue reportedly increased nearly threefold from prior periods reaching around $4.37 million by the end of 2015 (latest available historical snapshot), corresponding with expanded production capacity and broader market reach. While revenue growth was robust (about +297% YoY from latest figures available), profitability has lagged significantly as operating income remained negative at -$3.4 million FY2025 [F1]. Net losses narrowed marginally to around -$2.7 million that year but still reflect substantial operating challenges.

Historical performance (annual)

| FY | Net ($mm) | CFO ($mm) | OpInc ($mm) | Capex ($) | Net YoY |

|---|---|---|---|---|---|

| 2025 | -3 | -2 | -3 | 123000 | +4.6% |

| 2024 | -3 | -2 | -3 | 53000 | -0.0% |

| 2023 | -3 | -3 | 13000 | +54.6% | |

| 2022 | -6 | -3 | -6 | 13000 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | FCF ($mm) | ROE% |

|---|---|---|

| 2025 | -2 | -202.6 |

| 2024 | -2 | -488.8 |

| 2023 | -3 | -112.8 |

| 2022 | -3 | -246.7 |

Source: SEC companyfacts cache [F1].

*Note: Revenue data for years aside from 2015 is not explicitly reported.

Business Model and Market Focus

Barfresh serves predominantly institutional clients via national accounts, regional accounts, and foodservice distributors targeting school districts under federal nutrition programs and military contracts [S9][S10]. Product packaging formats cater to different client needs: single-serve beverage packs offer portion control and ease of use beneficial in settings with minimal on-site capital investment; bulk concentrated formulas serve high-volume dispensing sites efficiently [S11]. The Pop & Go™ ready-to-eat juice pops launched recently aim for seasonally complementary demand within school lunch programs [S10].

This diversified product portfolio aims to create competitive advantages based on convenience and quality assurances especially important for institutional buyers bound by nutritional regulations.

Operational Shifts Post-Acquisition

The acquisition of Arps Dairy brought internal manufacturing capability previously absent from Barfresh's model that relied entirely on contract manufacturing [S15][S16]. Initially contributing about 18% of total case production in Q4-2025, this marks incremental mitigation against supply chain vulnerabilities exposed when two major contract manufacturers ceased production relationships late last year—one responsible for roughly half of output in prior years [S16].

Owning the processing facility allows Barfresh greater control over ingredient procurement, production scheduling, freight logistics, cold storage costs as well as potential cost synergies. However, it also exposes the company to new operational risks intrinsic to dairy processing such as regulatory compliance under FDA standards, dependency on stable raw milk supplies affected by seasonal or market fluctuations, equipment reliability issues, labor availability constraints especially given rural facility location, environmental regulations on effluents/wastewater discharge and product safety protocols critical for perishable goods handling [S4][S23][S24][S17].

A newly constructed larger facility is underway set to expand capacity substantially but completion delays or budget overruns could negatively influence expected adjusted EBITDA forecasts [S8][S14][S21].

Financial Performance Nuances

The operating loss trend improved slightly year-over-year (-$3.43M operating income FY25 vs -$2.77M FY24), though remains significant against still modest revenues recorded most recently at $437K FY2015 benchmark figure—later years lack explicit revenue detail but growth inferred via scale expansion strategies and operational disclosures [F1][S29]. Net income followed a similar pattern showing sustained annual net losses (-$2.69M net income FY25), but slightly less severe than earlier years where net losses exceeded $6M (FY22). Cash flow from operations improved moderately though remains negative (-$1.67M FY25), producing persistent free cash flow deficits once capex is accounted for (-$1.789M FCF FY25), signaling continued funding requirements from external sources or equity financing [F1]

Liquidity metrics underscore financial constraints; the current ratio stood at roughly 0.38 at end-2025 reflecting current liabilities ($11m) substantially outweighing current assets ($4.2m), magnifying working capital pressure that could limit agility for expansion or inventory buildup ahead of demand surges [F1][S8].

Equity raised marginally over prior year ($1.33m FY25 vs $578K FY24) perhaps signifying fresh capital injections or retained earnings buffering balance sheet absorption of losses although return on equity remains deeply negative (~-203%), illustrating that shareholder value destruction persists amidst ongoing reorganization efforts [F1][S26]. Dividend payments have never been declared nor are planned amid these conditions confirming reinvestment priority towards scaling operations rather than shareholder distributions.

Risks That Could Cap Future Growth

The company faces several interconnected risks:

- Integration Complexity: Combining Arps Dairy's geographically distant operations while scaling up the new facility presents managerial execution challenges with risk of delayed cost synergies or disruptions [S1][S24].

- Regulatory Compliance: Operating under stringent FDA food safety protocols and environmental rules exposes Barfresh to potential fines or restrictions impacting production continuity if not met satisfactorily [S23][S4].

- Raw Milk Supply Volatility: Supply interruptions or price spikes due to weather events or agricultural market dynamics could inflate costs or curtail output affecting margins materially [S23][S22].

- Supply Chain Disruptions: Historic reliance on contract manufacturers ended abruptly placing strain on inventory availability; while acquisition provides backstop capacity some transitional uncertainty remains higher than average for comparable players in fragmented food manufacturing ecosystems [S16][S13].

- Intellectual Property Expiration: Key patents protecting product formulations expired mid-2025 potentially inviting increased competition reducing pricing power even if Barfresh maintains brand-based differentiation strategies centred around convenience factors unusual among commodity smoothiebased products[S9][S20].

- Liquidity Strain: Low current ratio plus continuing negative cash flows necessitate access to external financing; failure or unfavorable financing terms could restrict growth investments or force operational cutbacks[S8][S14].

- Product Liability Exposure: As new products are developed or deployed broadly especially in institutional markets increasing risk exists related to quality failures leading to recalls, litigation expenses or reputational damage[S4].

What To Watch Going Forward (Analysis)

Key milestones include timely completion and ramp-up of the New Facility currently under construction projected for late 2026 – its success will be pivotal not just operationally but financially where deferred capex or operational scaling would delay margin improvement trajectories flagged historically by management commentary.

Monitoring order intake patterns particularly from large institutional distributors within USDA programs and military contracts will shed light on demand sustainability amidst an increasingly competitive landscape post-patent expiry.

Evaluating working capital management effectiveness alongside debt or equity financing activities will provide insight into how well Barfresh copes with cash burn pressures during scale-up phases.

Innovation efforts appear modest with R&D spend under $132K annually yet remain critical especially if Barfresh seeks menu diversification beyond core smoothie categories towards more seasonally balanced offerings such as juice pops meant to improve quarterly revenue smoothing.[S10][F1]

Summary

Barfresh Food Group stands at an inflection where strategic vertical integration via the Arps Dairy acquisition sets a foundation for operational control benefits absent previously reliant solely on third-party manufacturers. The diverse product portfolio addressing niche institutional segments creates defensible positioning supported by government program certifications. However fundamental challenges persist including pronounced operating losses compounded by liquidity crunches which underscore heavy execution risk surrounding expansion capex projects alongside inherent vulnerabilities typical in dairy processing sectors linked to regulatory rigor and input supply dependencies. Improvement hinges largely upon timely realization of scale economies through successful plant commissioning coupled with steadyening institutional sales volumes while navigating intensifying competition post-patent expirations. Absent observable guidance quantification from disclosed materials, close attention should be given to updates about capacity utilization rates post-new facility launch along with working capital trends signaling financial stabilization warranted for any meaningful profitability inflection.

This analysis is based solely on publicly available financial disclosures through latest SEC filings as of April 17th, 2026 ([F1],[S#]) without offering investment advice.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments