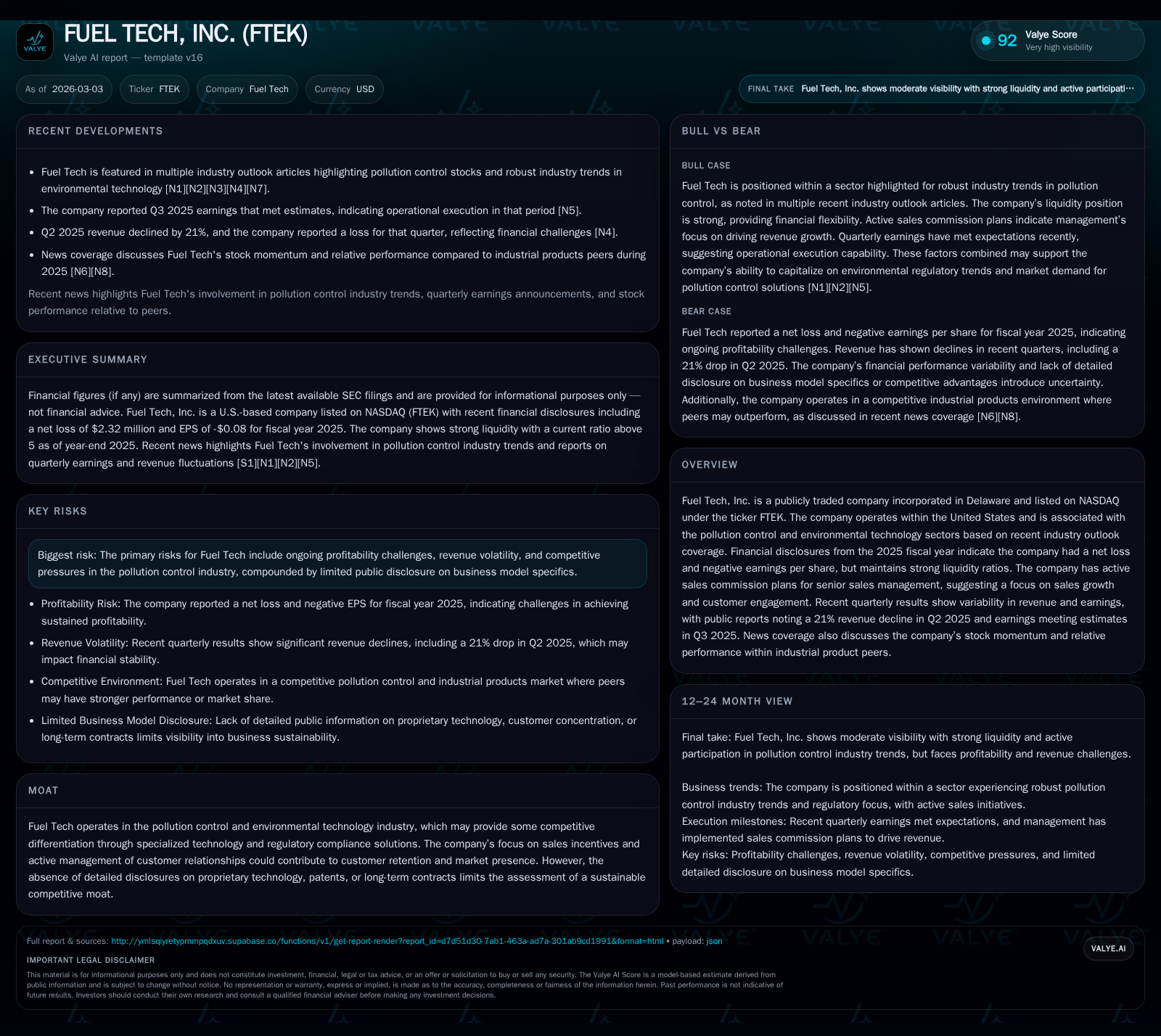

From Revenue Declines to Operating Recovery: Fuel Tech, Inc.’s Financial Pulse in Environmental Solutions

Fuel Tech’s steep revenue contraction through 2025 contrasts with improving operating losses and cash flow, underpinned by new sales incentives and robust liquidity.

Fuel Tech, Inc. has experienced significant volatility in revenue, culminating in a nearly 70% drop by fiscal year 2025. Despite the sharp decline, the company improved its operating income loss by roughly 22%, reflecting tighter cost control amid challenging market conditions. Operating cash flow turned positive and increased substantially in 2025 despite ongoing net losses, supported by strategic investments and a conservative capital structure. The introduction of targeted sales commission plans for senior management underscores a prioritization of top-line growth through enhanced customer engagement at its core product lines. Nonetheless, Fuel Tech faces persistent risks from regulatory headwinds and limited evidence of a durable competitive moat within the pollution control sector.

Historical Growth Trends and Performance Drivers

Fuel Tech has experienced pronounced volatility and downward pressure on its top-line performance over recent years. Revenues peaked near $15.8 million in FY2018 before declining sharply to approximately $4.9 million as of fiscal year-end 2019 according to SEC XBRL data [F1]. Available annual figures reveal an extreme contraction culminating in an approximate 69% year-over-year drop between FY2024 and FY2025 — a staggering decline that significantly redefines the company’s scale.

This precipitous revenue erosion was accompanied by persistent operating losses. Operating expenses exerted considerable pressure on margins throughout this period; however, incremental operational improvements are evident with operating income losses narrowing sequentially from -$4.7 million in FY2024 to -$3.7 million by the end of FY2025, an improvement of roughly 22% despite adverse revenue dynamics [F1], [S15]. This suggests deliberate cost containment or efficiency initiatives partially offsetting top-line deterioration.

Net income trends mirror this pattern but remain negative with modest widening losses (approximately -$2.3 million in FY2025 versus -$1.9 million prior year), reflecting both operational performance and non-operating factors common among smaller publicly traded industrial tech companies battling cyclical demand shifts and product mix effects.

Historical performance (annual)

| FY | Net ($mm) | CFO ($mm) | OpInc ($mm) | Capex ($) | Net YoY |

|---|---|---|---|---|---|

| 2025 | -2 | 3 | -4 | 674000 | -19.6% |

| 2024 | -2 | -3 | -5 | 378000 | -26.3% |

| 2023 | -2 | 1 | -3 | 418000 | -6.7% |

| 2022 | -1 | -4 | -2 | 206000 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | FCF ($mm) | ROE% |

|---|---|---|

| 2025 | 2 | -5.8 |

| 2024 | -4 | -4.6 |

| 2023 | 0 | -3.5 |

| 2022 | -4 | -3.2 |

Source: SEC companyfacts cache [F1].

Note: Revenue prior to FY2019 is documented but less comparable due to business shifts.

2025 Financial Analysis: Revenue Declines Amid Operating Improvements

The fiscal year ended December 31, 2025 stood out for Fuel Tech as a paradoxical blend of severe top-line deterioration alongside improved income statement leverage on costs and expenses.

While total revenues contracted drastically, the company succeeded in shrinking its operating loss by over one-fifth relative to the prior year—a significant margin gain when viewed against the backdrop of nearly two-thirds revenue shrinkage ([S15]). This dynamic points toward concerted efforts on overhead reduction or potential restructuring such as streamlined production or SG&A trimming often seen when environmental tech vendors recalibrate during demand troughs.

Quarterly commentary released alongside year-end results indicated earnings roughly aligned with analyst forecasts despite these challenges ([S15]), underlining consistent management guidance execution even amid adverse market forces.

Sales Commission Structures as Growth Levers

Decisive moves towards reactivating sales capacity were evidenced by Fuel Tech’s Compensation Committee adoption on December 11, 2025 of two new senior sales commission plans targeting its Senior Vice President of Sales ([S13]).

The first incentive scheme—the APC Plan—ties commissions directly to contract values for all sales under Fuel Tech’s APC product line within U.S. and Canadian territories; the second—the FUEL CHEM Plan—links payments to net revenues from customer units similarly located.

These align compensation explicitly with selling outcomes amidst traditional industrial environments where ordering cycles can be protracted, facilitating stronger customer engagement focus among senior sales executives.

Such structures could materially influence future order backlog buildup—especially critical for smaller-scale suppliers dependent on project-driven purchase dynamics—and reflect proactive steps toward top-line recovery amidst structural industry headwinds.

Analyzing Operating Cash Flow Recovery and CapEx Patterns

A notable highlight emerges forward from prior years’ negative cash flows: Fuel Tech posted a substantial positive swing in operating cash flow (CFO) during FY2025.

Operating cash inflows rose approximately 188% year-over-year—from negative $3.43 million in FY2024 to +$3 million reported at FY-end ([F1]). This reversal evidences better working capital management or profit cycle improvements sufficient to overcome stated net losses.

Interestingly, capital expenditures increased materially (+78%) reaching $674 thousand in FY2025 alone ([F1]). This step-up signals continued reinvestment into technology assets or equipment vital for maintaining competitive capabilities or meeting regulatory standards—an important consideration for environmental technology equipment providers adapting products for evolving emissions norms.

The strong liquidity posture supports this balance between spending stimulus and financial prudence: a current ratio exceeding five times (current assets vs current liabilities) stands as a significant cushion unusual for companies sustaining consistent net deficits ([F1]).

Capital Structure, Liquidity, and Shareholder Returns Overview

Fuel Tech maintains an equity base just shy of $40 million as of end-2025 versus declining equity figures previously noted ([F1]). Despite recorded net negativity—approximately -5.8% return on equity based on latest annual net loss relative to shareholders’ equity—the company preserves stable balance sheet fundamentals critical for access to debt markets or vendor credit lines common within the pollution control industry.

No dividends were declared nor share repurchases executed since at least the mid-2010s according to available records ([F1]), aligning with conservative capital policies typical for firms prioritizing liquidity during protracted operational loss phases.

Cash reserves totaling nearly $12 million provide an ample runway though sustained profitability remains uncertain without demonstrable top-line resumption ([F1]).

Future Outlook: Industry Positioning and Growth Constraints

Industry perspectives sourced from recent analyst commentary outline generally robust demand drivers within pollution control sectors fueled by mounting regulatory scrutiny requiring installation or upgrades of emissions reduction technologies ([N1], [N2]).

However, Fuel Tech’s valuation of its own competitive positioning highlights absence of explicit patent portfolios or contractual exclusivity arrangements that conventionally serve as protective moats within niche technological markets ([S4], [S5]).

Given this landscape, growth opportunities hinge largely upon successful sales activations—hence newly implemented commission incentives—and potential product innovations not yet specifically disclosed.

Market constraints such as increasing competition among providers targeting similar environmental compliance mandates may cap upside absent distinctive differentiation or scalability advantages.

Key Risks from Regulatory and Market Dynamics

Fuel Tech faces multiple risk vectors documented meticulously across recent SEC filings including contingent legal proceedings potentially related to contractual disputes or environmental compliance matters ([S4], [S7]).

Regulatory dynamics pose unpredictability given evolving pollution standards which can both create opportunities and impose costly adaptations.

Cybersecurity risks feature prominently given internal data dependency although mitigations appear integrated per disclosures ([S1]).

Macro sector uncertainties resembling pandemic-related supply chain disruptions from earlier years still linger as wildcards impacting manufacturing cycles and installation projects relevant to industrial pollution control assets ([S5], [S6]).

Monitoring Metrics That Could Signal Turnaround or Further Volatility

Key performance indicators worth close observation include:

- Quarterly revenue trajectory vis-à-vis historically volatile demand patterns noted across fiscal periods ([N1], [N2]).

- Operating margin progression reflecting further cost discipline or scaling efficiencies post new incentive program implementation ([S3]).

- Operating cash flow sustainability beyond typically seasonal fluctuations particularly following structural capex commitments.

- Order backlog metrics revealing tangible traction tied directly or indirectly to commissioned sales management plans introduced late-2025 ([S13]).

- Fluctuations within legal/regulatory environment developments potentially affecting project timelines or compliance costs ([S4], [S7]).

Taken together these factors offer insights into whether Fuel Tech can translate administrative shifts into durable operational rebound or will face continued cyclical pressures inherent within pollution control technology provision.

This report synthesizes publicly filed financial statements with recent corporate disclosures and industry commentaries without attempting any forward-looking investment recommendations or speculative forecasts beyond evidenced facts.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments