FrontView REIT Doubles Revenue Amid Profitability and Capital Structure Challenges

The company’s rapid revenue growth in 2025 contrasts with ongoing losses and a new preferred equity issuance impacting financial flexibility.

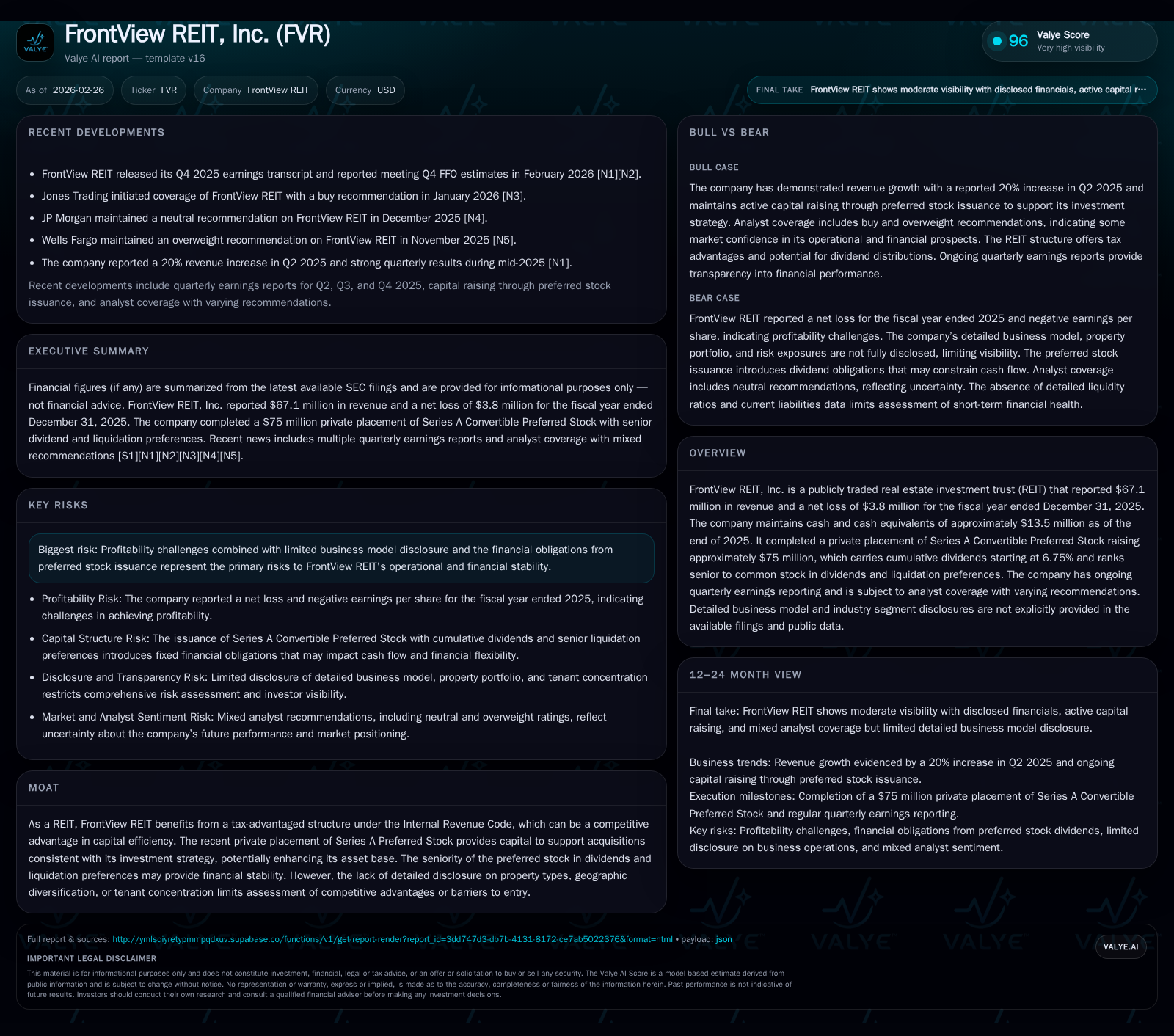

FrontView REIT, Inc. reported a significant revenue surge to $67.1 million for fiscal year 2025, more than tripling from the previous year. Despite this top-line growth, the REIT remains unprofitable, posting a net loss of $3.8 million, reflecting continued operational challenges. The company strengthened its capital base by raising $75 million through a Series A Convertible Preferred Stock private placement, which carries cumulative dividends and senior claims over common shareholders, aiming to support future acquisitions. Investors should watch how FrontView balances growth investments against dividend obligations and whether operational efficiencies emerge to reverse losses.

Historical Performance

FrontView REIT demonstrated striking top-line expansion in fiscal year 2025, generating revenues of $67.1 million compared to just $15.2 million in the prior year—a staggering increase of over 340% year-over-year as per the latest filings [F1]. This leap likely reflects aggressive asset acquisitions or ramped leasing activity, although the company has not disclosed detailed property segment or geographic data to clarify the drivers [S6].

However, despite increased revenues, operating losses deepened from -$4.8 million in 2024 to -$5.6 million in 2025, illustrating that scaling has not yet translated into profitability enhancement [F1]. Net losses widened even more on a percentage basis, reaching nearly $3.8 million or approximately a 28% deterioration versus the previous fiscal year [F1].

Interestingly, operating cash flow surged dramatically to $42.1 million from a modest $2.7 million the direct prior year—an indicator of improved underlying cash earnings despite accounting-level net losses [F1]. This may suggest that non-cash charges contributed materially to losses or that working capital dynamics improved significantly.

Dividends paid totaled about $16.6 million in 2025 despite negative net income, consistent with typical REIT practice requiring distribution of taxable earnings to shareholders but also imposing cash flow demands on the business [F1].

Historical performance (annual)

| FY | Rev ($mm) | Net ($mm) | CFO ($mm) | OpInc ($mm) | Rev YoY | Net YoY |

|---|---|---|---|---|---|---|

| 2025 | 67 | -4 | 42 | -6 | +342.2% | -27.8% |

| 2024 | 15 | -3 | 3 | -5 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | ROE% |

|---|---|

| 2025 | -1.0 |

| 2024 | -0.9 |

Source: SEC companyfacts cache [F1].

Revenue growth outpaced improvements in operating efficiency leading to deeper losses.

Capital Structure and Governance Changes

To enhance its financial capacity for further acquisitions aligned with its investment strategy, FrontView completed a private placement raising approximately $75 million through issuance of Series A Convertible Preferred Stock priced at $100 per share [S8][S9][S13]. This preferred equity carries cumulative dividends starting at an annual rate of 6.75%, increasing after four years up to a maximum of 12%, and holds seniority over common stock dividends and liquidation rights [S9][S11].

The preferred shares are convertible into common stock at an initial conversion rate implying a conversion price of about $17 per share—raising potential dilution concerns if conversions occur subject to stockholder approval and liquidity conditions [S22][S21]. Additionally, associated warrants provide holders options for incremental common shares exposure.

Governance shifts followed this capital raise with the appointment of Charles Fitzgerald—a managing partner at Maewyn Capital Partners (a key investor)—to the company’s board as a non-employee director [S25]. This move likely reflects increased investor oversight linked to the preferred stock arrangement.

Liquidity and Covenants

The Investment Agreement imposes restrictions requiring consent from preferred shareholders for incurring additional indebtedness beyond specified leverage ratios (7:1 debt-to-equity ceiling) or altering core corporate governance without approval [S10][S19][S23]. These covenants limit FrontView's financial flexibility but provide protections for preferred investors.

Future Growth Prospects

Future growth hinges substantially on FrontView’s ability to deploy capital raised via preferred equity effectively into accretive real estate acquisitions or developments aligned with its investment mandate [N2][N3]. Improved operating cash flows provide some buffer for reinvestment and obligations servicing.

However, absence of detailed disclosures about property types (e.g., office vs industrial vs retail), geographic diversification or tenant concentration restricts clear visibility into sustainable competitive positioning or resilience against cyclical downturns [S6]. The persistent operating losses highlight ongoing profitability challenges that could cap upside unless management improves operational efficiency or enhances leasing spreads.

Additionally, cumulative preferred dividends represent fixed financial burdens that must be met quarterly ahead of common stock dividends; failure could constrain dividend flexibility and shareholder returns [S9]. Any large-scale dilution risk tied to preferred conversion would affect existing common shareholders’ value.

Market analysts noted the company meeting quarterly funds from operations (FFO) estimates recently but continue divergent views on growth trajectory given operational opacity and capital cost considerations [N2][N3]. Watching capital deployment pace relative to accretive returns will be crucial milestones.

Returns and Capital Allocation

Although FrontView reported net losses (-$3.8M) for fiscal year ended December 31, 2025 , it delivered positive operating cash flow ($42.1M), indicating solid underlying cash generation necessary for sustaining dividends and reinvestments [F1].

The payout of $16.6 million in dividends during the same period aligns with traditional REIT obligations but arguably pressures retained earnings and internal funding availability given persistent unprofitability.

No buybacks are indicated post preferred issuance; indeed repurchasing common shares is restricted under terms while cumulative dividends on Series A Preferred remain unpaid or declared limiting opportunistic capital returns outside dividend commitment [S8][S11].

Return on equity is negative (~-1%), reflecting ongoing losses versus expanded equity base post-capital raise ($391 million equity end-2025) [F1]. This suggests immediate shareholder returns remain challenged absent operational turnaround.

Industry Context Analysis (Non-company specific)

REITs like FrontView leverage favorable tax treatment under U.S. Internal Revenue Code Section 856 which mandates distributing most taxable income as dividends but allows avoidance of corporate income taxes at entity level—this advantage is mitigated if net incomes remain negative or weighted by financing costs such as high coupon preferred shares.

Sector-wide trends indicate selective appetite for well-located industrial assets driven by e-commerce logistics demand while office space faces headwinds due to hybrid work preferences. Without segment disclosure it's hard to benchmark FrontView’s exposure effectively which is pivotal for forecasting sustainable AFFO trajectories critical for dividend coverage.

Preferred stock issuances have become more common among growth-stage REITs seeking flexible non-debt capital but introduce complexities around layered capital structures affecting balance sheet risk profiles.

Risks Summary

FrontView faces pronounced risks related to its lack of profitability persistence amid rising operational scale countered by mounting cumulative dividend liability from new preferred stock issuance creating mandatory cash outflows surpassing current earning capacity [S4][S5]. Limited transparency on asset types and geographical exposure adds uncertainty about consistency or defensibility of earnings base.

Furthermore, restrictions imposed through investor rights agreements limit strategic maneuvers regarding new debt creation or structural corporate changes without investor approval possibly slowing agile responses in dynamic real estate markets.

What To Watch Next (Analysis)

- Quarterly earnings releases for progress toward operating profitability or narrowing losses.

- Announcements regarding acquisitions funded by Series A Preferred proceeds clarifying asset class focus and expected yields.

- Changes in dividend policy on common shares relative to preferred obligations signaling cash flow comfort levels.

- Movements around preferred stock conversion triggers impacting shareholder dilution.

- Updates on Board composition reflecting governance influence from new institutional investors.

- Any disclosures improving clarity around portfolio composition enabling better competitive assessment.

Disclaimer: This analysis is based solely on publicly available information as of February 26, 2026 including SEC filings and news releases cited herein; it does not constitute investment advice or recommendations.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments