General Mills Faces Sales Pressure and Margin Challenges with Steadfast Capital Returns

General Mills navigates recent sales declines and margin compression while maintaining disciplined capital allocation.

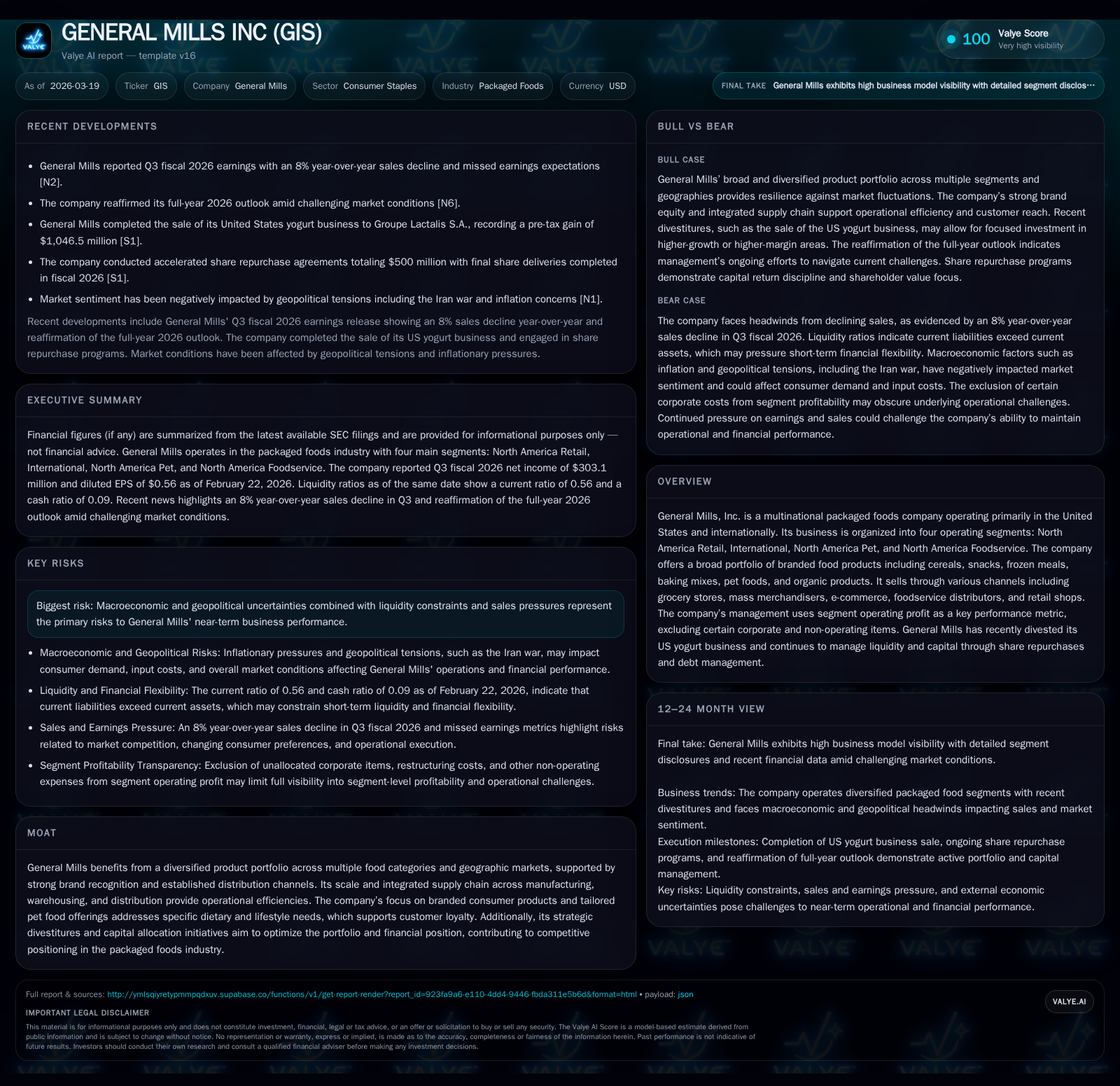

General Mills reported a decline in revenues and net income, driven by lower volume and higher costs impacting margins in core food categories. Recent divestitures and portfolio optimization efforts mark a strategic pivot toward higher-margin business lines, including pet foods and international markets. While sales pressures persist amid inflationary headwinds and changing consumer patterns, the company sustains robust cash flow generation and prioritizes shareholder returns through dividends and share repurchases. Investors will watch execution on restructuring initiatives and potential stabilizing trends in demand as key milestones in coming quarters.

Historical Performance Overview

General Mills ended fiscal 2025 with revenue of approximately $20.38 billion, growing 4.1% compared to fiscal 2024's $19.57 billion [F1]. This improvement was predominantly driven by price increases across its portfolio rather than volume expansion, as demand softness persisted amid inflationary and competitive pressures. Despite top-line growth, operating income declined by 3.7% to $3.3 billion from $3.43 billion the prior year reflecting margin compression caused by rising input costs related to commodities and transportation combined with supply chain complexity [F1].

Net income saw an especially steep decline of 47%, shrinking to just $294 million from over half a billion dollars the previous year. The deterioration was amplified by restructuring costs linked to strategic transformation initiatives including portfolio pruning (notably the US yogurt business divestiture) [N1][S3]. Operating cash flow remained solid at nearly $2.92 billion but was down roughly 12%, while free cash flow held up better at about $2.3 billion after capex outlays of $625 million which declined year-over-year as spending discipline increased [F1].

Historical performance (annual)

| FY | Rev ($bn) | Net ($mm) | CFO ($bn) | OpInc ($bn) | Rev YoY | Net YoY |

|---|---|---|---|---|---|---|

| 2025 | 294 | 2.9 | 3.3 | -47.3% | ||

| 2024 | 2.0 | 558 | 3.3 | 3.4 | +4.1% | -9.3% |

| 2023 | 2.0 | 615 | 2.8 | 3.4 | -8.3% | -25.3% |

| 2022 | 2.1 | 823 | 3.3 | 3.5 | -2.5% |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | Div ($mm) | Buybacks ($bn) | FCF ($bn) |

|---|---|---|---|

| 2025 | 1339 | 1.2 | 2.3 |

| 2024 | 1363 | 2.0 | 2.5 |

| 2023 | 1288 | 1.4 | 2.1 |

| 2022 | 1245 | 0.9 | 2.7 |

Source: SEC companyfacts cache [F1].

Note: Revenue YoY for FY24 vs FY23 was negative reflecting mix changes post-pandemic recovery dynamics.

Segment Dynamics

The company reports financials across four segments representing distinct markets:

- North America Retail: Large grocery chains, mass merchandisers, natural foods outlets mainly selling cereals, snacks, frozen meals including organic lines.

- International: Diverse region-focused product offerings including super-premium ice cream brands exporting from the U.S., as well as direct retail to consumer frozen dessert shops.

- North America Pet: Growing segment targeting premium pet nutrition aligning products with life-stage needs via dry/wet/fresh foods driving loyalty.

- North America Foodservice: Distribution into foodservice operators encompassing cereals, snacks, bakery products designed for bulk channels.

Recent divestitures notably sold off the U.S.-based yogurt businesses affecting North America Retail’s reported sales but allowing focus on higher margin categories like pet food and international expansions [S9][S13]. Segment operating profits have been pressured especially in North America Retail due to lower volumes but partially offset by gains in Pet and International segments supported by innovation and expanded distribution networks.

Future Growth Prospects

Growth catalysts center around several strategic initiatives:

- Accelerating innovation within pet foods aligns with consumer trends favoring healthful human-grade ingredients addressing dietary/lifestyle needs; this segment offers improved growth visibility given category expansion tailwinds globally [S13].

- International markets are a focus area leveraging proprietary premium frozen desserts brand reputation alongside tailored retail concepts for greater direct-to-consumer penetration.

- Continued portfolio optimization via selective divestitures (e.g., yogurt) streamlines brand portfolio aiming for sustainable margin enhancement.

- Efficiency efforts under restructuring programs target manufacturing integration improvements that should support margin recovery over medium term.

Conversely, persistent macro risks loom: inflation may continue to erode raw material cost benefits and compress margins; geopolitical uncertainties affect export markets; consumer retrenchment around discretionary spending could limit volume gains especially in competitive grocery aisles [N1][S2].

Forward-Looking Expectations & Milestones

Management reaffirmed FY26 outlook emphasizing commitment to structural cost saving initiatives while anticipating some near-term top-line softness due to channel repricing impacts post-yogurt exit [N13][S2]. Close monitoring of Q4 fiscal results will be critical to gauge efficacy of operational changes and demand stabilization.

While explicit guidance details are limited in filings, key milestones include:

- Completion of remaining accelerated share repurchase agreements originally funded via proceeds from yogurts business sale providing balance sheet flexibility [S6][S11].

- Measurable improvement in segment operating profit margins across North America Retail from integration projects.

- International revenue growth acceleration driven by targeted marketing investments.

- Pipeline launches within North America Pet emphasizing premiumization.

Capital Allocation & Returns

General Mills' capital allocation underscores solid shareholder return policy balanced against investment needs:

- Dividend payments have remained stable at ~$1.34 billion annually with steady yield focus despite earnings volatility demonstrating confidence in cash flow generation capacity [F1][S15].

- Share repurchases totaled circa $1.2 billion in fiscal 2025 after a peak re-purchase spend of about $2 billion in prior year; recent purchases included accelerated share repurchase programs amounting to roughly half a billion dollars funded partly by divestiture proceeds—reflecting disciplined opportunistic repurchase activity amidst market volatility [S5][S6][S15].

- Free cash flow conversion remains strong facilitating self-funded investment capex alongside returns reconciliation.

- Leverage metrics indicate manageable long-term debt levels (~$13 billion), predominantly fixed-rate notes with staggered maturities through mid-2030s plus short-term commercial paper usage kept low or zero at recent balance sheet points enhancing liquidity buffer [S10][S14].

Return on equity calculated from last reported net income over embedded equity balances stands near modest low single-digit levels (~3%) largely reflecting transient profitability pressures while underlying operational cash flows remain robust [F1].

Reconciliation Notes

Reported figures reflect annual periods concluding May each year versus quarterly updates presented through February periods referenced in interim filings—this occasionally leads to timing differences particularly impacting liquidity measures or debt balances discussed across different documents ([F1],[S10],[S14]). Further earnings discrepancies arise from non-cash charges including restructuring expenses localized principally within Q3 fiscal cycles ([N1],[S2]). These variances are standard for diversified multinational packaged food companies undergoing active portfolio reshaping.

Conclusion

General Mills grapples with the dual challenge of top-line softness amid rising input costs that have impaired earnings momentum notably in its staple North America Retail segment following strategic divestitures such as yogurt operations removal—intended to sharpen portfolio focus towards more resilient high-growth categories like pet foods internationally.

Its large-scale integrated supply chain coupled with fortified liquidity positions underpin continued capacity for tactical investments alongside shareholder returns execution via dividends plus buybacks supported by sizable free cash flows generated consistently even during turbulent industry cycles.

The near-term outlook warrants cautious observation with primary performance inflection points resting on ability to restore volume growth post restructuring while mitigating inflationary cost burdens through efficiency improvements—the company’s response will shape competitive positioning going forward within an increasingly dynamic global packaged food landscape.

This memo is prepared solely for informational purposes based on available SEC filings and reputable news sources as of March 2026 without providing investment advice.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments