Genworth Financial Balances Market Risks with Capital Return Amid Slowing Profitability

Stable revenue masks growing pressures on operating income, prompting a cautious capital return strategy despite complex risk exposures.

Genworth Financial reported essentially flat revenues near $7.3 billion in fiscal 2025, continuing a pattern of stagnation since 2024, while its operating income plummeted by over 90% year-over-year. This divergence underscores elevated cost pressures and adverse market dynamics impacting profitability despite a steady top line. The company's capital allocation includes renewed stock buybacks contrasted with a restrained dividend posture, reflecting management's balancing act amid regulatory complexities and embedded derivative risks. Monitoring upcoming quarterly milestones and regulatory developments will be key to assessing whether these trends stabilize or deteriorate further.

Stagnant Top-Line during Mixed Historical Performance

Genworth Financial’s revenue trajectory over the past four fiscal years presents a tale of abrupt expansion followed by an unsettling plateau. After jumping drastically from roughly $1.9 billion in both FY2022 and FY2023 to about $7.3 billion in FY2024 and remaining stable at this level in FY2025 ([F1]), the company shows minimal revenue growth of just 0.1% between 2024 and 2025.

However, beneath the stable revenue lies significant distress. Operating income nosedived by more than 93%, declining from $633 million in FY2022 to approximately $41 million by end-2025 ([F1]). Net income also contracted by nearly 25% year-over-year but stayed positive at $223 million for FY2025 ([F1]). Meanwhile, operating cash flow (CFO) fell sharply by approximately 69% compared to FY2022 levels—down to $327 million in FY2025 from over $1 billion three years earlier ([F1]).

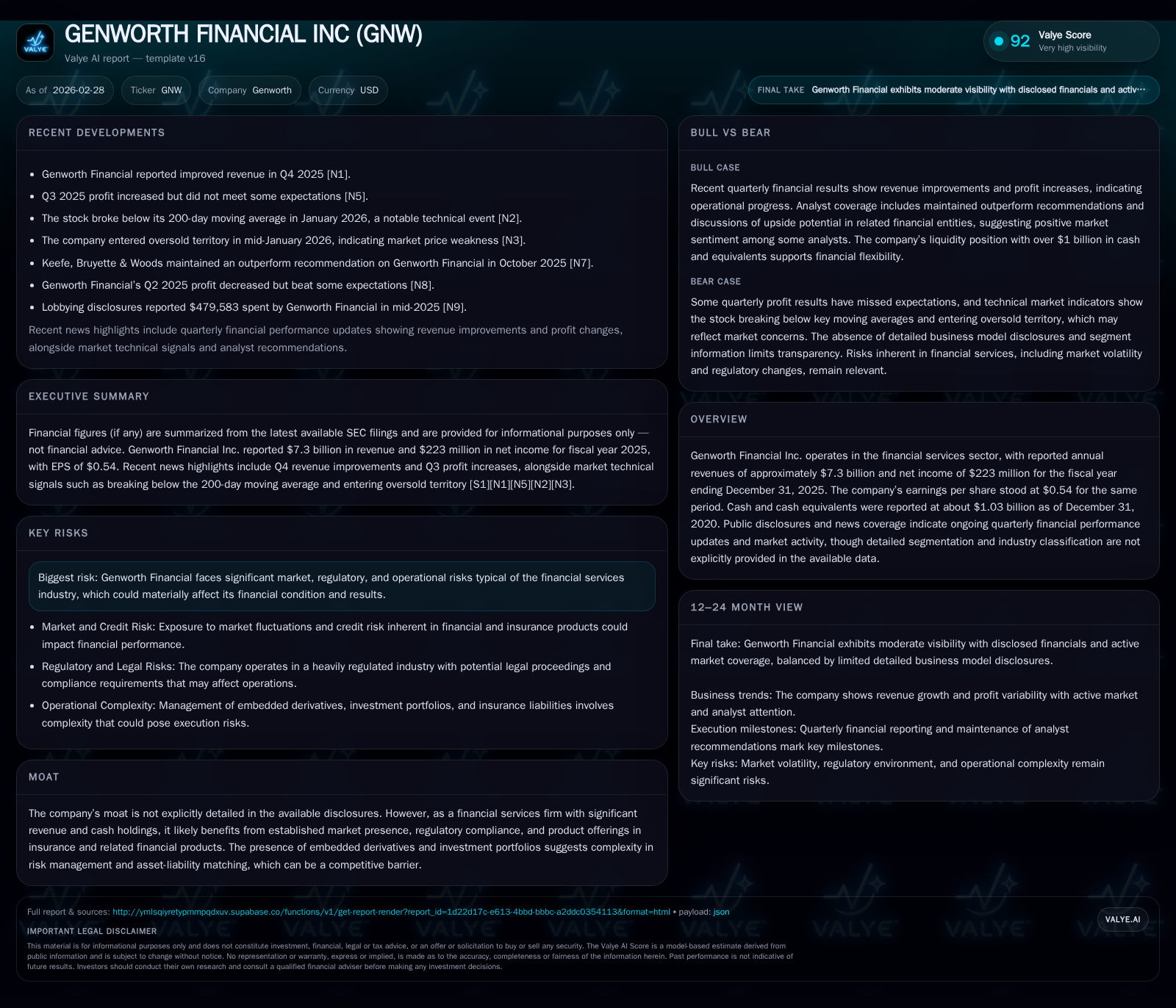

Historical performance (annual)

| FY | Rev ($bn) | Net ($mm) | CFO ($mm) | OpInc ($mm) | Rev YoY | Net YoY |

|---|---|---|---|---|---|---|

| 2025 | 7.3 | 223 | 327 | +0.1% | -25.4% | |

| 2024 | 7.3 | 299 | +281.7% | +241.0% | ||

| 2023 | 1.9 | -212 | 41 | +0.8% | -221.1% | |

| 2022 | 1.9 | 175 | 1049 | 633 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | Buybacks ($mm) | ROE% |

|---|---|---|

| 2025 | 247 | 2.5 |

| 2024 | 189 | 3.5 |

| 2023 | 296 | -2.8 |

| 2022 | 36 | 1.8 |

Source: SEC companyfacts cache [F1].

Note: The substantial increase in revenues starting FY2024 likely reflects changes in reporting scope or consolidation; operating income data for some years is limited.

Dissecting the Operating Income Plunge: Cost Pressures and Market Dynamics

The precipitous drop in operating income signals intensified cost burdens and adverse operational factors overshadowing stable top-line receipts. Though specific drivers are not detailed, sector challenges such as rising claims expenses or underwriting losses may contribute ([S1/N1]). Genworth’s exposure to embedded derivatives within indexed universal life insurance and fixed indexed annuity liabilities complicates earnings recognition due to mark-to-market volatility and hedge accounting complexities ([S10/S12]).

Asset-liability management remains pivotal given duration mismatches between long-term liabilities and investment portfolios—a classic insurer risk heightened here by fair-value measurement challenges especially at level-3 inputs where observable markets are scarce ([S7/S10]). Q4 results showed some revenue improvement but margin compression persists partly due to investment portfolio valuations ([N1]).

Future Revenue Drivers and Regulatory Headwinds

Genworth acknowledges regulatory complexity as a major constraint on growth avenues ([S4/S29]). Ongoing litigation alongside compliance demands increases overhead costs that constrain free cash flow potential ([S4]). While explicit guidance is absent, management cautiously explores product innovations within a restrictive regulatory environment ([N1/S29]).

Pricing discipline pressures and product redesign needs—especially under low-interest rate conditions affecting annuity crediting rates—limit upside potential. New market entries face established competitors and increased capital requirements presenting barriers to rapid scaling.

Navigating Market Volatility: Risk Factors and Embedded Derivatives

Disclosures emphasize how embedded derivatives exacerbate earnings volatility via sensitivity to equity indices or interest rates ([S10/S12]). These instruments require mark-to-market valuation often relying on internal models under level-3 fair value inputs due to lack of direct pricing sources ([S11/S13]). Such valuations introduce model risk amid complex netting arrangements designed to mitigate credit exposure but adding layers to risk frameworks ([S10/S19]).

Risk factors warn that rapid shifts in fair value measurements could impair capital adequacy ratios impacting credit ratings—a critical concern for investors ([S19]). Hedging these exposures requires careful calibration to avoid basis risk or correlation breakdowns during stress.

Capital Allocation Strategy: Buybacks Revive While Dividend Policy Stays Cautious

Genworth emphasizes share repurchases which rose from $189 million in FY2024 to $247 million in FY2025 ([F1]), reflecting management’s focus on deploying excess capital towards buybacks amid constrained profit growth.

Dividend payments remain minimal without recent increases disclosed ([F1/N1]), suggesting prudence driven by earnings uncertainty and regulatory scrutiny over surplus distributions. This approach favors flexible capital returns over fixed payouts amid volatile profits.

Assessing Cash Flow Trends and Equity Returns

Operating cash flow has contracted significantly with nearly a 70% decline from FY2022’s robust level of approximately $1 billion down to $327 million by FY2025, highlighting challenges sustaining liquidity internally ([F1]).

Return on equity (ROE), approximated as net income divided by equity ($223M / ~$8.75B), stands near a modest ~2.5%, lagging typical financial services benchmarks that target mid-to-high single digits ([F1]). This subdued return reflects cost pressures alongside conservative leverage strategies.

Key Milestones to Monitor in 2026 and Beyond

Absent explicit forecasts, key catalysts include:

- Quarterly earnings releases for signs of margin recovery or deterioration following Q4 improvements ([N1/S3]);

- Regulatory outcomes including litigation settlements or compliance changes altering risk-weighted assets ([S4/S29]);

- Updates on capital structure actions such as buyback pace adjustments or dividend policy shifts;

- Market technicals like GNW breaking below its long-term moving average and entering oversold territory signaling investor sentiment changes ([N2/N3]).

Given embedded derivatives complexity coupled with external pressures, close monitoring is essential to determine if profitability headwinds are temporary or structural.

Disclaimer

This analysis is based solely on publicly available data as of February 28, 2026. It does not constitute investment advice or recommendations regarding Genworth Financial Inc.'s securities.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments