Alphabet Inc: Navigating Growth Amid Regulatory and Cost Pressures in Internet Content and Cloud

Alphabet's 2025 results highlight robust growth in advertising and cloud services, offset by heightened costs and regulatory risks.

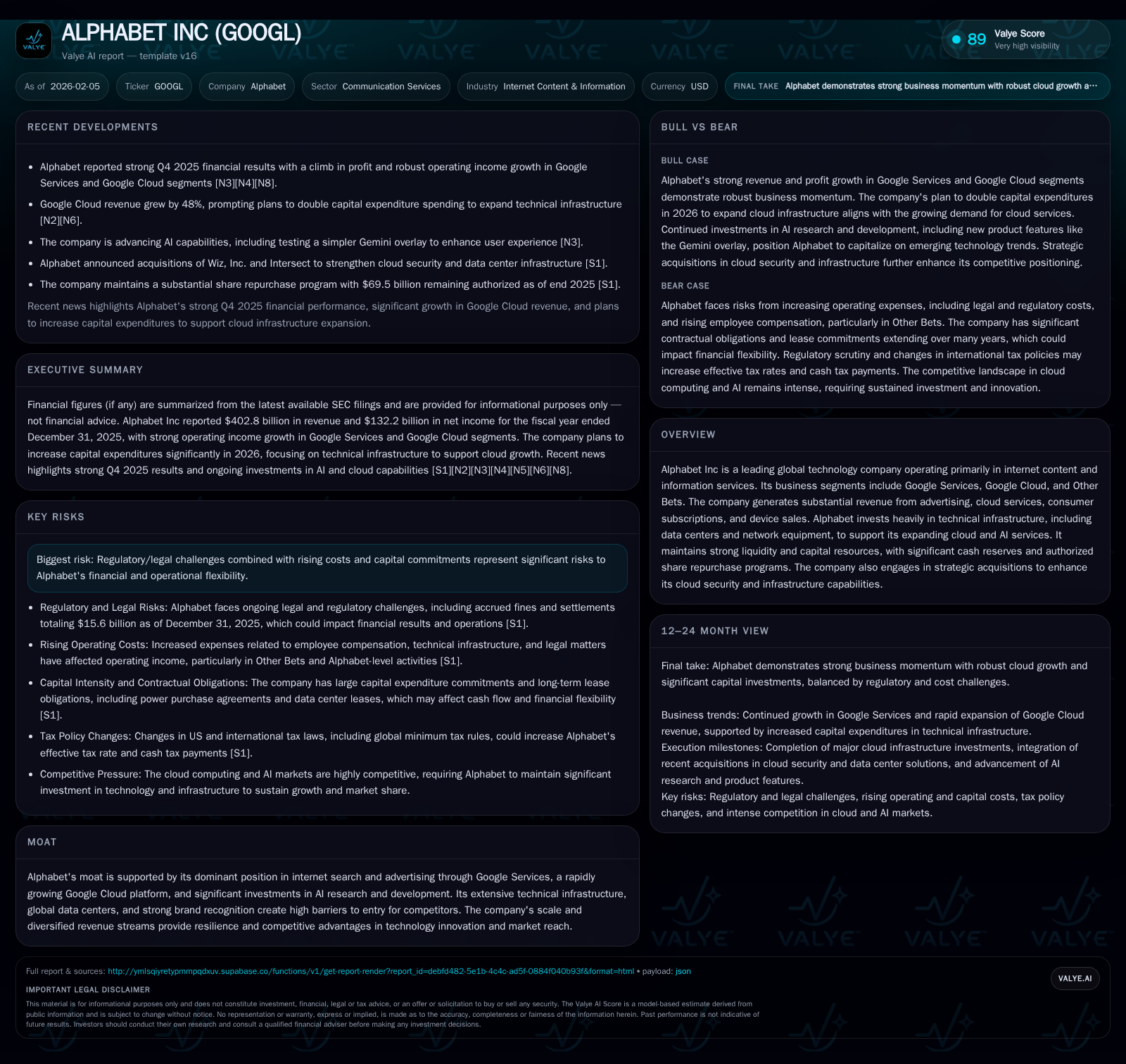

Alphabet Inc demonstrated significant revenue and operating income growth in its Google Services and Google Cloud segments during 2025, driven by strong search advertising demand and expanding cloud adoption. Despite these gains, rising employee compensation, legal expenses, and an increasing operating loss in Other Bets highlight challenges amid intensifying regulatory scrutiny. The company’s strategic investments in AI research, infrastructure expansion, and acquisitions underpin its competitive moat but also contribute to capital commitments that could pressure future margins. Alphabet’s sizable cash reserves and diversified revenue streams provide resilience as it balances innovation with escalating operational complexities.

Business Overview

Alphabet Inc operates across multiple business segments namely Google Services (including advertising, subscriptions, platforms, and devices), Google Cloud, and Other Bets—emerging technologies with longer-term horizons such as Waymo autonomous vehicles. As of the end of 2025, Alphabet solidified its status as a dominant force in the Communication Services sector under the Internet Content & Information industry category [S1][F1]. The company’s core revenue engines remain high-margin digital advertising through search and YouTube, coupled with fast-growing cloud infrastructure services catering to enterprise clients.

2025 Financial Performance Highlights

Fiscal year 2025 marked a period of impressive top-line expansion for Alphabet, culminating in $402.8 billion of total revenues—a figure reflecting sustained advertiser demand globally as well as expanded consumption of cloud offerings by enterprises [F1][S1]. Operating income increased significantly to $129.0 billion from $112.4 billion in 2024 [S1]. Notably:

- Google Services contributed $139.4 billion of operating income (up $18.1 billion YoY), reflecting strong ads sales offset partially by higher content acquisition and traffic acquisition costs.

- Google Cloud almost doubled its operating profit to $13.9 billion (up $7.8 billion), driven by revenue gains despite heavier infrastructure expenses.

- Other Bets recorded an increased operating loss of $7.5 billion (up $3.1 billion), notably impacted by elevated valuation-based employee compensation related to Waymo.

The firm experienced an increase in corporate or Alphabet-level expenses related mainly to shared AI research initiatives—expenses attributable beyond individual business segments—that rose from $10.5 billion in 2024 to $16.8 billion [S1]. These reflect Alphabet's strategic priority on pioneering advances in artificial intelligence and machine learning across its product lines.

Revenue Composition & Monetization Dynamics

Google Services

This segment mainly comprises advertising via Google Search properties including partner search engines, YouTube ads, and network properties (such as AdSense and AdMob). Additionally, it integrates consumer subscription revenues (YouTube Premium/TV/Music), platform sales (Google Play apps/in-app purchases), device sales (Pixel smartphones), and other products/services [S1].

Paid clicks on search-based properties remained a critical metric indicating user engagement levels driving ad monetization; cost-per-click saw fluctuation due to competition intensity for keywords. Factors influencing advertising revenues include geopolitical events affecting advertiser budgets as well as evolving ad formats/policies requiring continual adaptation [S1].

Google Cloud

Google’s rapidly growing cloud business encompasses infrastructure-as-a-service (IaaS), platform-as-a-service (PaaS), application offerings, and related security solutions enhanced through recent acquisitions aiming at strengthening enterprise cloud security capabilities [N1][S1]. Despite escalating capital spending—data centers construction and network equipment upgrades—the unit improved profitability significantly through economies of scale combined with higher revenue realization.

Other Bets

Though currently loss-making, Other Bets represents Alphabet’s exploratory venture into disruptive technologies such as autonomous driving via Waymo [S1]. The increased losses primarily arose from share-based compensation which is valuation sensitive alongside ongoing R&D expense escalation.

Capital Structure & Liquidity Position

At year-end 2025, Alphabet held approximately $30.7 billion cash and cash equivalents within total current assets of $206 billion against current liabilities of around $103 billion—translating into a healthy current ratio above 2x which signals solid short-term financial flexibility [F1]. This liquidity buffer supports continued investments in cutting-edge technology infrastructure while providing options for opportunistic share repurchases given authorized programs noted in recent filings [S1].

Competitive Moat & Strategic Advantages

Alphabet’s moat is multifaceted encompassing:

- Dominance in search-engine advertising supported by unmatched scale of indexed content and user data,

- Expanding Google Cloud platform bolstered by continuous service innovation,

- Extensive investments in AI research powering superior product features,

- Global data center network ensuring performance reliability,

- Strong brand equity fostering trust among advertisers, developers, and users alike. These factors impose significant barriers for smaller competitors attempting to enter or disrupt Alphabet’s core markets [Valye Report Excerpt].

Challenges & Risks

Notwithstanding extraordinary financial success, Alphabet faces notable headwinds:

- Regulatory/legal environment: Increased antitrust scrutiny particularly concerning monopolistic practices relating to ad sales dominance; stringent privacy regulations impacting targeted advertising efficacy;

- Rising operational costs: Escalating employee remuneration particularly stock-based compensation has inflated SG&A expenses;

- Capital commitments: Heavy spending on infrastructure expansion creates near-term margin pressure;

- Geopolitical uncertainties: Variable advertiser demand linked to global macroeconomic conditions may induce revenue volatility;

- Taxation changes: Reforms such as OECD global minimum tax efforts alongside local US tax law adjustments affect effective tax rates and reported results [S1].

Industry Context & Competitive Landscape Analysis (Analysis)

The broader communication services industry remains intensely competitive with peers like Meta focusing heavily on metaverse initiatives while AWS and Microsoft Azure vie aggressively in enterprise cloud computing—a direct battleground for Google Cloud [N14][N12]. Rapid digital transformation trends continue propelling cloud adoption though market share gains require significant continuous investment.

Moreover, shifts toward privacy-first ad technologies following regulatory policy tightenings challenge historically data-driven advertising models Nielsen-style measurement methods seek replacement prompting innovation demands.

Within AI research especially large language models and generative AI forms compete at scale among major technology companies where Alphabet’s open investments into Gemini models signify attempts to maintain technological leadership [Valye Report Excerpt].[N3]

Recent Developments & Earnings Insights

The Q4 2025 earnings call revealed optimism centered around resilient search ad performance combined with robust Google Cloud bookings growth that reportedly exceeded consensus estimates [N7][N8][N13]. However, management highlighted increased legal expenses reflecting ongoing investigations along with cautious commentary on near-term cost inflation risks impacting profitability.

Investor discourse since has focused on whether strong search plus accelerating cloud momentum can offset these pressures underpinning confidence in the underlying business model sustainability amidst external challenges [N6][N3][N1]. Strategic M&A activity continues selectively enhancing the company’s secure cloud capabilities further bolstering competitive positioning [Valye Report Excerpt].

Summary

Alphabet Inc stands as an exemplar of enduring innovation-driven growth balanced against emerging risks inherent to its scale and industry position. Its dominant search-advertising franchise coupled with accelerating enterprise cloud adoption create durable revenue engines while significant investments in AI research aim at sustaining long-term leadership. Nevertheless rising legal/regulatory scrutiny along with increasing costs require pragmatic management attention. Strong liquidity affords maneuvering room enabling sustained capital expenditure programs aimed at maintaining technological preeminence amidst evolving market dynamics. Ultimately Alphabet exemplifies a complex technology conglomerate navigating a shifting landscape where continuous innovation underpins competitive defenses but heightens operational demands.

This report is prepared solely for informational purposes without offering investment advice or recommendations regarding any securities.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments