In-Depth Analysis of Home Federal Bancorp Inc of Louisiana’s Regional Banking Dynamics

A comprehensive review of HFBL’s recent performance, business model, competitive positioning, and economic levers within the regional banking sector.

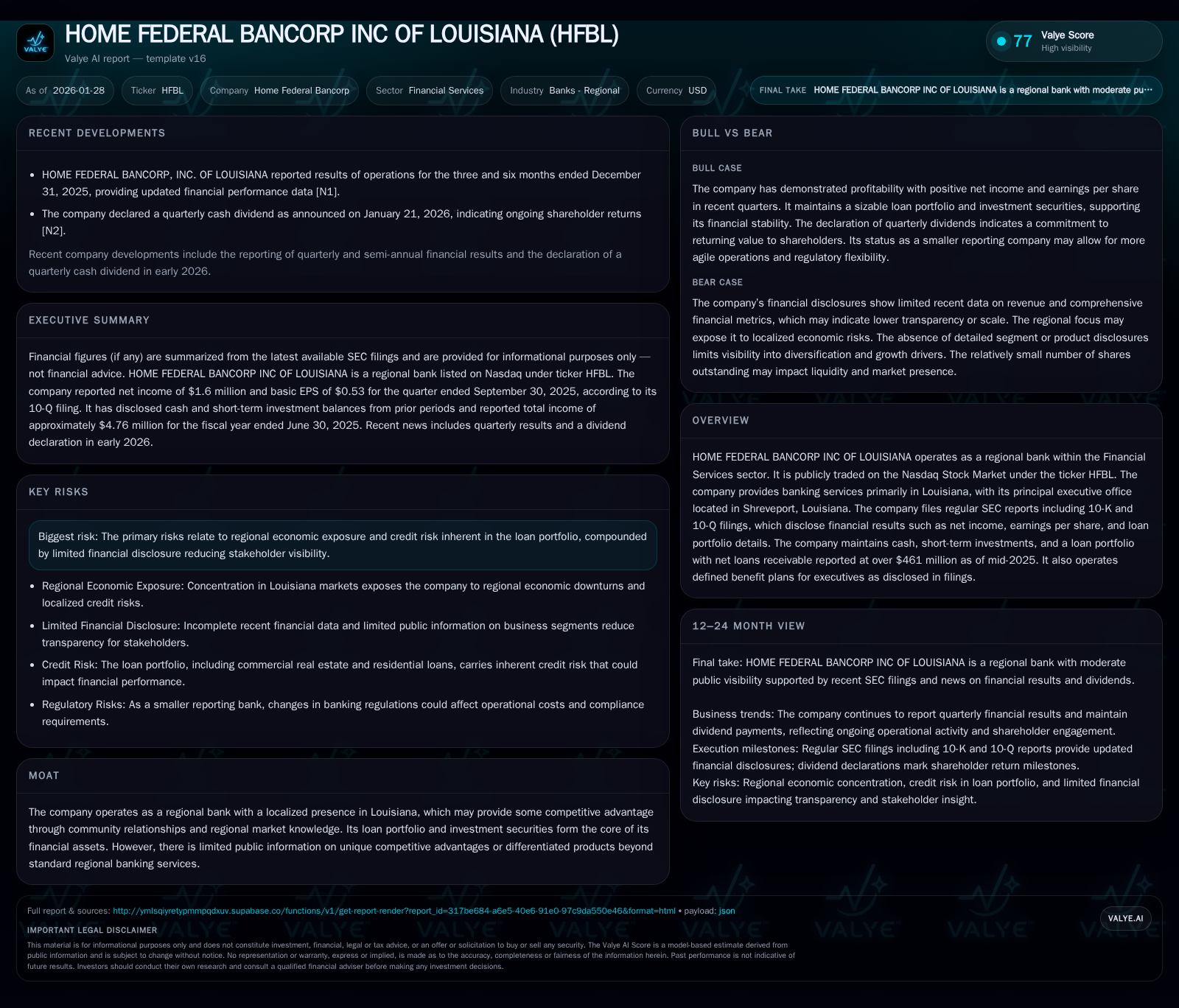

Home Federal Bancorp Inc of Louisiana (HFBL) operates as a regional bank focused primarily on Louisiana, with a loan portfolio dominated by real estate secured loans. Recent earnings reports show stable operations with consistent dividend payouts. The company’s business model centers on originating and managing a mix of fixed and adjustable rate residential and commercial real estate loans, with geographic concentration creating both opportunity and risk. Competitive pressures stem from larger regional and community banks, while economics hinge on loan underwriting quality, interest rate management, and asset-liability composition. Key diligence areas include credit concentration risks and limited public disclosure.

What Changed Recently

Home Federal Bancorp Inc of Louisiana reported its results of operations for the three and six months ended December 31, 2025, highlighting continued stable financial performance [N1, N5]. The company declared a quarterly cash dividend of $0.135 per share, reflecting a steady shareholder return policy [N2, N3, N4, N6, N7, N8]. These announcements signal consistent earnings generation and capital management, important for a regional bank with concentrated geographic exposure.

The earnings release did not disclose material shifts in strategy or portfolio composition but reaffirmed the bank’s focus on its core regional banking services. The declared dividend and operational updates suggest a confidence in current income streams and balance sheet health.

Business Model as a System

HFBL operates primarily as a regional bank serving Louisiana, with a business model centered on originating, holding, and managing a loan portfolio composed mainly of residential and commercial real estate loans [S1, S2]. The company’s customers are local individuals and businesses requiring mortgage and commercial financing.

The loan portfolio composition as of June 30, 2025, shows approximately 32% of one-to-four family residential loans are adjustable-rate loans, which feature interest rate adjustments capped annually at 1% and cumulatively at 6% above or below the initial rate. These loans are underwritten based on the initial rate plus 2%, reflecting a cautious approach to interest rate risk [S1].

Commercial real estate loans account for approximately 29.8% of the total loan portfolio, with the majority (about 62%) secured by owner-occupied properties. These loans are originated with a maximum loan-to-value of 85% and terms typically no longer than five years, though amortization may extend up to 20 years [S1]. The bank generally holds a first lien position, reducing credit risk exposure.

The company’s revenue is largely derived from net interest income generated by the loan portfolio and investment securities, minus loan origination fee amortization and credit loss provisions. Tangible capital stands at about $56.7 million, supporting balance sheet growth and regulatory requirements [S13, S14].

Operating leverage is moderate, with the bank balancing growth ambitions against capital constraints and maintaining conservative underwriting practices. The company also manages defined benefit plans for executives, a factor in overall expense management [Valye report excerpt].

Industry Map & Competitive Battlefield

The regional banking industry in Louisiana is characterized by a mix of community banks, regional players, and larger national bank branches. HFBL’s competitive set includes other banks offering mortgage, commercial real estate, and deposit services within the same geographic footprint.

Competitive differentiation is limited, with most institutions competing on customer relationships, local market knowledge, pricing, and service quality. Larger banks may have scale advantages and broader product offerings, whereas smaller community banks may excel in personalized service.

HFBL’s moat appears to be its localized presence and established customer relationships within Louisiana, but there is no public evidence of unique technology platforms, specialized lending niches, or significant brand power beyond the regional level. This positions the bank in a highly competitive, commoditized market segment where operational efficiency, credit discipline, and customer retention are critical to maintaining profitability.

Economic and regulatory environments at the state and federal level also shape competitive dynamics. Louisiana’s economy, influenced by energy, manufacturing, and agriculture sectors, impacts loan demand and credit risk profiles. Regulatory scrutiny on capital adequacy, loan concentrations, and compliance costs is a constant factor for regional banks.

Where the Economics Become Real

HFBL’s core economic drivers hinge on the quality and composition of its loan portfolio, interest rate management, and operational cost control. The bank holds over $461 million in net loans receivable as of mid-2025, indicating a substantial asset base generating interest income [Valye report excerpt].

The mix of fixed and adjustable-rate loans provides some natural hedge against interest rate fluctuations, though the concentration in real estate loans exposes the bank to local market cycles and credit risk. The underwriting caps on adjustable loans and conservative loan-to-value ratios on commercial loans are critical levers for managing potential credit losses.

Loan origination fees and their amortization affect net interest margin calculations, with reported amortization of deferred loan origination fees in the range of $70-110 thousand quarterly [S10, S11]. Loan loss allowances, reported in the low millions for residential and commercial segments, reflect the bank’s assessment of credit risk and economic conditions [S11].

Tangible capital of approximately $56.7 million supports balance sheet growth but also constrains aggressive expansion or risk-taking. Maintaining capital ratios consistent with regulatory expectations is a key operational focus.

Dividends, such as the recent $0.135 per share quarterly payout, illustrate the balance between returning capital to shareholders and retaining earnings for growth and loss absorption [N2, N3].

Operating expenses include personnel costs, technology investments, and regulatory compliance, with executive defined benefit plans adding complexity to long-term cost structures.

Diligence Questions / Disconfirming Signals

- What is the detailed breakdown of loan portfolio credit quality metrics, including non-performing loans and charge-offs, especially in the commercial real estate segment?

- How sensitive is HFBL’s net interest margin to rising interest rates, given the mix of fixed and adjustable-rate loans?

- What are the geographic and sectoral concentrations within the loan book beyond the broad Louisiana focus?

- How does HFBL’s efficiency ratio compare to peer regional banks in Louisiana and the broader Southern U.S.?

- Are there any emerging regulatory or legal risks disclosed in filings not captured in current public news?

- How does HFBL manage deposit base stability and cost, and what is the competitive landscape for core deposits?

- What is the strategy regarding potential loan sales or securitization, given past references to selling loans in unfavorable interest rate environments?

- Is there clarity on the impact of executive defined benefit plans on future cash flows?

- How robust is the company’s technology infrastructure in supporting digital banking services and operational scalability?

Conclusion

Home Federal Bancorp Inc of Louisiana operates a focused regional banking business with core strength in residential and commercial real estate lending within Louisiana. Recent earnings and dividend announcements confirm stable operations, while the bank’s conservative underwriting and capital management practices mitigate risk in a competitive, cyclical environment. The absence of detailed public disclosures on credit quality and operational metrics limits full transparency, underscoring the importance of continued monitoring of portfolio performance and regulatory developments.

This analysis is based on publicly available information as of early 2026 and does not constitute investment advice or recommendations.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments