Hagerty, Inc.'s Rebound: From Niche Insurance Leader to Expanding Automotive Ecosystem

Hagerty leverages its specialized collector car insurance foundation and community engagement to fuel growth across its marketplace and membership services.

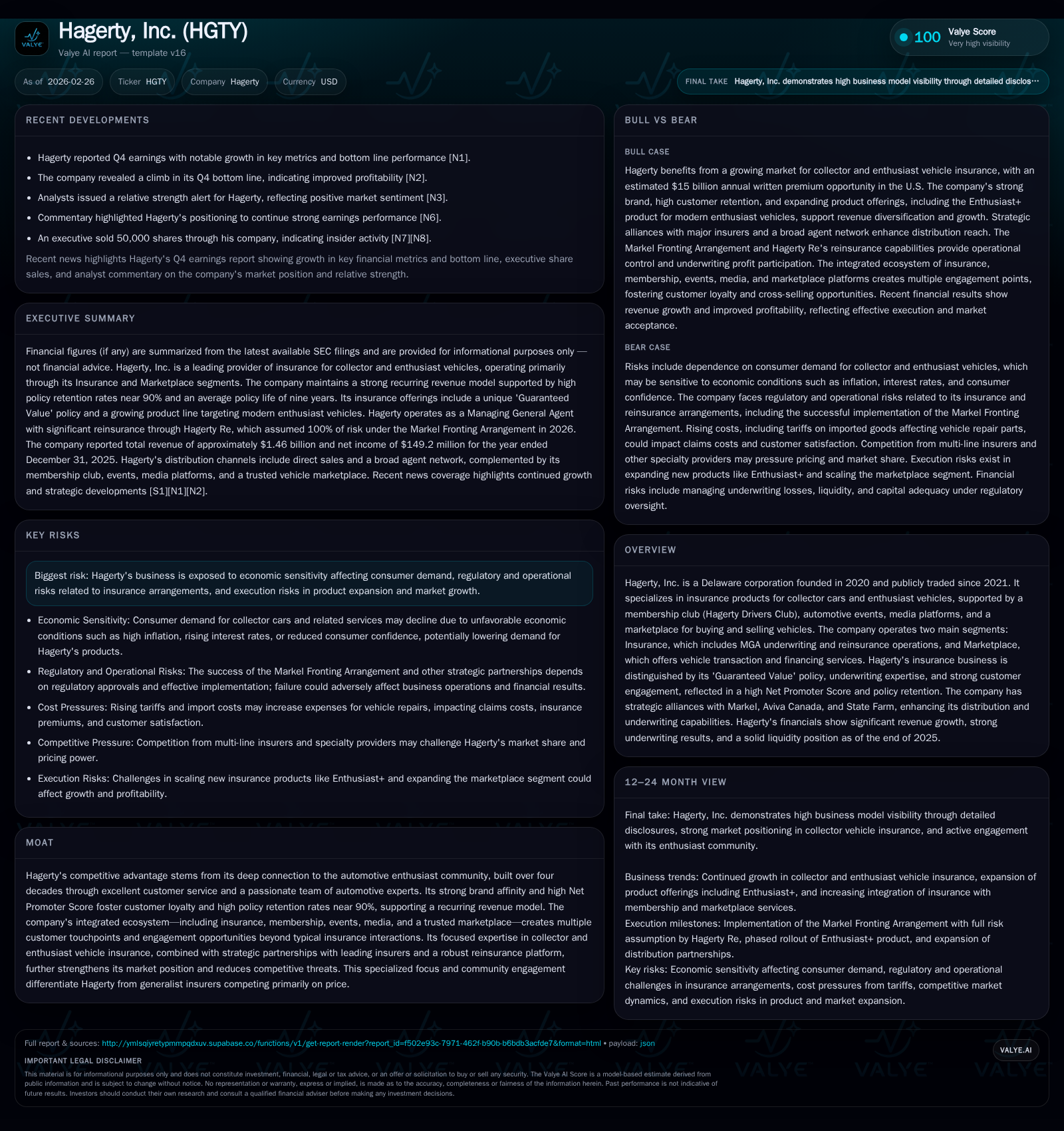

Hagerty, Inc. has evolved from a niche insurer for classic and enthusiast vehicles into a diversified automotive ecosystem integrating insurance, membership clubs, media, events, and a vehicle marketplace. Its exceptional customer loyalty, evidenced by nearly 90% policy retention and strong Net Promoter Scores, underpins recurring revenue growth. The company reported robust financial results in FY2025 with 21.4% revenue growth and a significant operating income turnaround. Strategic partnerships, including an expanded reinsurance alliance with Markel, support underwriting capabilities while new product launches and marketplace expansion offer incremental growth avenues. Despite economic sensitivities and regulatory complexities inherent in specialty insurance, Hagerty’s capital structure remains sound with disciplined allocation and compliance with covenants.

Heritage and Historical Growth Trajectory

Hagerty stands out as a storied player in the collector car insurance market tracing its roots back more than four decades before forming Hagerty, Inc. as a Delaware holding company in 2020 and going public on the NYSE in 2021 under ticker HGTY [S6]. Historically focused on automobile enthusiasts, it has cultivated deep brand loyalty driving sustained revenue gains.

Financially, Hagerty posted substantial growth from $787.6 million revenue in FY2022 to $1.46 billion in FY2025 — a compound annual growth trend highlighted by a 21.4% year-over-year jump in the latest reporting period [F1]. Operating income likewise swung from a loss of $67.6 million in FY2022 to a positive $66.4 million by FY2024 illustrating rapid margin recovery amid scaling operations.

Net income follows this trend: positive $32.1 million in FY2022 improving nearly fivefold by FY2025 (return soared 169.2%) — underpinning profitability improvements coinciding with higher policy retention locking recurring revenue streams near 90%, and an average policy life of approximately nine years [F1][S6]. This historical trajectory reflects successful leveraging of specialist underwriting expertise fused with a passionate automotive community framework.

Historical performance (annual)

| FY | Rev ($mm) | CFO ($mm) | OpInc ($mm) | Capex ($mm) | Rev YoY |

|---|---|---|---|---|---|

| 2025 | 1456 | 219 | 25 | +21.4% | |

| 2024 | 1200 | 177 | 66 | 21 | +20.0% |

| 2023 | 1000 | 134 | 10 | 26 | +27.0% |

| 2022 | 788 | 55 | -68 | 44 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | FCF ($mm) |

|---|---|

| 2025 | 194 |

| 2024 | 156 |

| 2023 | 107 |

| 2022 | 11 |

Source: SEC companyfacts cache [F1].

Note: Latest available operating income is for FY2024; net income figure for FY2025 not available at time of report.

Insurance Product Differentiation and Market Dynamics

Central to Hagerty’s competitive edge is its flagship 'Guaranteed Value' insurance product which insures collector vehicles at pre-agreed values rather than typical depreciated sums seen elsewhere in auto policies [S6]. This value-aligned protection resonates strongly with enthusiast customers who invest heavily into their vehicles both financially and emotionally.

Underwriting sophistication is evident in the company’s Managing General Agent (MGA) role where it crafts policies sold directly or through a broad agent network including nine of the largest U.S auto insurers [S13]. The MGA status combined with reinsurance affiliate Hagerty Re secures quota share arrangements predominantly with Markel-affiliated insurer Essentia — recently expanding its risk assumption from an initial quarter share to up to full program coverage post-2026 [S22].

This fronting arrangement—a term for insurers issuing policies but passing risk to reinsurers—provides additional underwriting margin stability while maintaining appropriate risk-based capital buffers aligned with regulatory solvency requirements like Bermuda Solvency Capital Requirement for Hagerty Re or NAIC RBC for U.S-licensed Drivers Edge entity [S1][S12]. These layered protections construct barriers against ingress by more generic insurers lacking sector expertise.

Expanding the Marketplace and Membership Ecosystem

Beyond core insurance products, Hagerty operates an intertwined ecosystem anchored around its membership club — the Hagerty Drivers Club (HDC). This extends engagement via curated automotive events, specialty media platforms featuring high-quality content across digital and print formats, plus a trusted marketplace platform facilitating buying/selling transactions for both entry-level enthusiast vehicles as well as high-value collectibles [S6].

This integration creates frequent customer touchpoints uncommon in standard insurers who primarily interact around premium billing or claims servicing alone — boosting brand stickiness through continuous engagement across lifestyle aspects underlying enthusiast automotive culture [S21].

The Marketplace segment gradually evolves into an increasing portion of overall revenues as vehicle transaction volumes grow augmented by financing services tailored specifically towards collector cars from vintage classics upwards — fostering long-term community involvement feeding upstream demand for insurance products.

Recent Financial Performance and Drivers of Improvement

Quarterly disclosures for Q4 FY2025 reveal continued momentum surpassing analyst expectations on both top-line premiums collected and bottom-line profitability enhancements driven largely by operational efficiencies coupled with premium rate increases responsive to underlying vehicle valuation trends [N1][N2][N7].

Claims volatility partly influenced by catastrophe events such as Hurricanes Helene & Milton along with California wildfires slightly pressured claims expense; however written premium expansion offset these impacts leading to favorable loss ratio dynamics — critical for sustaining underwriting profitability metrics typical within specialized MGA structures [N11][S3].

Operating cash flow delivered strong growth at +23.7% annually hitting nearly $219 million in calendar year-end results accompanied by moderate capital expenditures mainly invested into technology platform development enhancing customer experience layers vital for marketplace scalability [F1][S1].

Future Opportunities amid Economic and Regulatory Challenges

Moving forward, Hagerty plans portfolio innovation including products like Enthusiast+ aimed at penetrating adjacent segments within its base demographic potentially expanding insured vehicle counts further [N5]. Expanded usage of data analytics driving granular risk segmentation alongside geographic diversification enhances underwriting accuracy mitigating margin pressure risks inherent in specialty lines affected by economic cycles or tariff shocks impacting consumer discretionary spending patterns on collectible vehicles [S2].

Regulatory considerations remain paramount especially navigating approval processes tied to expanding fronting arrangements with large partners such as Markel requiring ongoing compliance with solvency capital mandates alongside careful management of dividend restrictions particularly within Bermuda-based reinsurance entities limiting distributable cash flows without sanctions from regulators [S1][S12].

Capital Allocation Discipline and Shareholder Returns

Hagerty maintains a robust capital structure supported by revolving credit facilities aggregating approximately $450 million combining JPMorgan-led $375 million facility maturing March 2030 plus additional debt under BAC Credit Facility extended through December 2028 ensuring liquidity flexibility needed for working capital continuity alongside investment needs [S4][S5].

Financial covenant compliance remains intact covering minimum fixed charge coverage ratios & maximum leverage ratios providing creditors comfort amidst variable interest rate exposure (~5.57%) generating conservative interest expense profile relative to earnings capacity [S18].

The Company abstains from issuing dividends due chiefly to Bermuda solvency law restrictions governing reinsurance arm payouts & state regulatory approval conditions applicable to U.S carrier subsidiary Drivers Edge constraining direct shareholder returns currently; likewise share repurchase programs remain absent reflecting reinvestment priorities focused on ecosystem growth rather than capital return strategies at this stage [S17][S20].

Notably measured ROE approximates mid-teens near ~14.5% consistent with healthy profitability balanced against capital deployment into growth initiatives supporting long-term value creation fundamentals per latest fiscal year-end disclosures [F1].

Key Milestones and Emerging Risks to Watch

Key upcoming catalysts include finalizing regulatory approvals associated with executing comprehensive fronting agreements enhancing Hagerty Re’s risk absorption scale which promises improved underwriting economics but subject to execution risks inherent during integration phases involving multiple counterparties & jurisdictions [S2][N9].

Legal exposures remain modest yet warrant monitoring as defense costs may elevate depending on outcome scenarios linked to intellectual property claims or contractual disputes common within proprietary content & marketplace domains; management assesses that none currently pose material adverse threats but vigilance remains prudent given potential operational distractions or settlement expenses involved [S7].

Renewal rate trends post recent natural disasters merit close observation as insurance pricing softening or adverse claim development could pressure margins quarterly until normalization occurs reflecting broader specialty lines market behaviors seen industry-wide under inflationary or macroeconomic stress periods [N13].

Disclaimer: This report synthesizes publicly available financial data extracted primarily from SEC filings ([F1], [S#]) supplemented by contemporaneous news releases ([N#]). It intentionally excludes any form of investment advice or price forecasting per internal policy guidance.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments