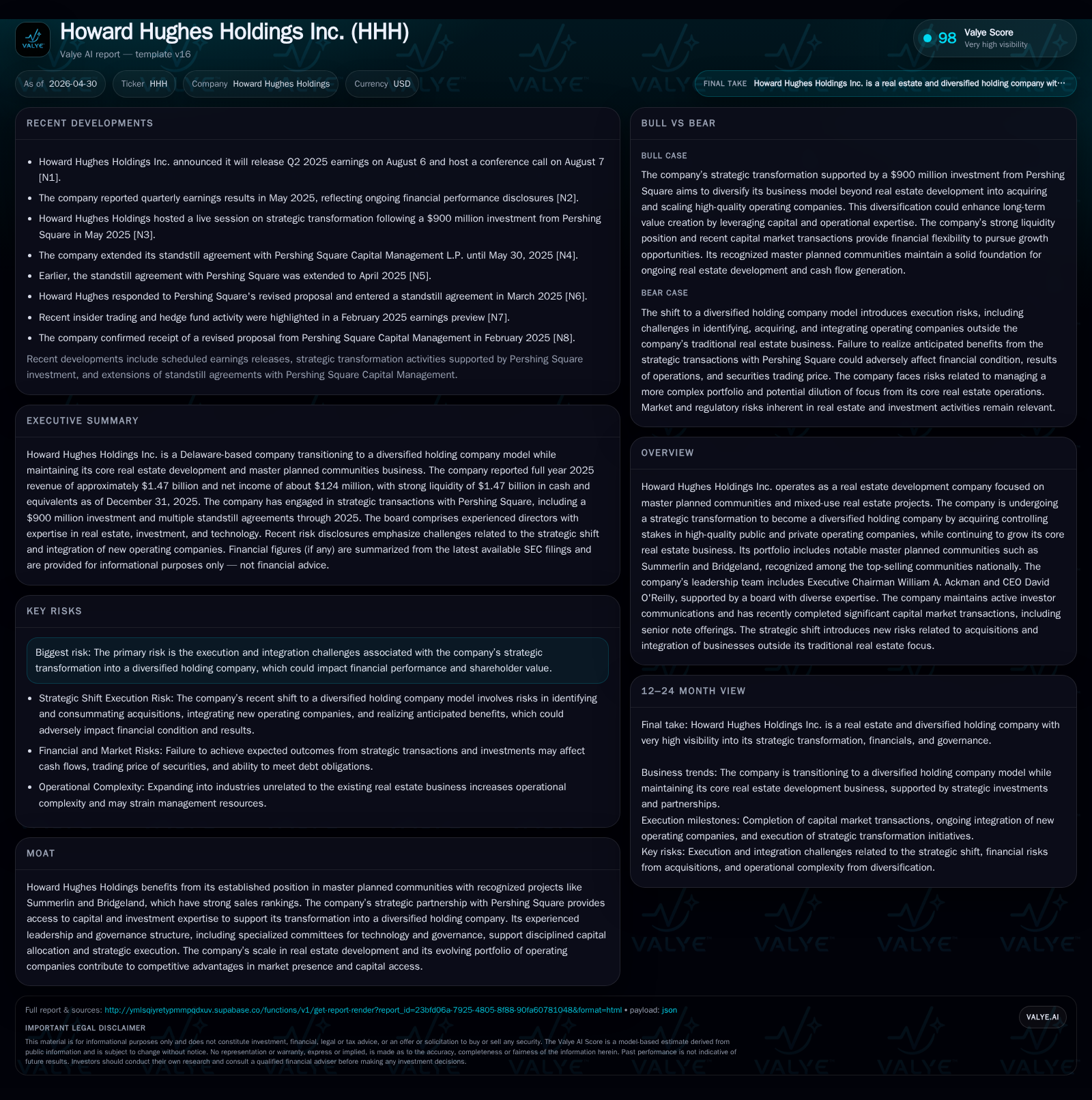

Howard Hughes Holdings Accelerates Diversification Strategy with Capital Market Moves

Howard Hughes Holdings is morphing from a pure-play master planned community developer into a diversified holding company, leveraging capital market tools and a strategic partnership with Pershing Square.

In its latest quarterly disclosure, Howard Hughes Holdings (HHH) announced a strategic pivot to acquire controlling stakes in high-quality public and private operating companies, moving beyond its traditional real estate development focus. This transformation leverages a capital backing partnership with Pershing Square and includes recent warrant issuances and significant senior note offerings to finance growth. While the core business remains concentrated on master planned communities such as Summerlin and Bridgeland, the company’s evolving portfolio aims at durable growth segments. Execution risks in integration and diversification remain the primary concerns as HHH navigates this multi-industry expansion.

Latest Operating Update Highlights Strategic Pivot

Howard Hughes Holdings’ most recent quarterly report filed on November 10, 2025 (Form 10-Q) marks a distinct inflection point in the company's operational narrative [S2]. The firm disclosed an announced transaction with Pershing Square involving an ambitious corporate strategy shift: evolving from primarily a real estate developer focused on master planned communities toward a diversified holding company with active investments in public and private operating firms across multiple sectors. This updated model involves acquiring controlling stakes in high-quality, durable-growth companies while continuing measured investments in its core real estate assets.

Further reinforcing the transformation trajectory, an April 21, 2026 Form 8-K noted execution of a warrant agreement involving a substantial private placement with accredited investors, exemplifying fresh equity-related capital deployment mechanisms supporting the diversification plan [S3]. These strategic financial maneuvers highlight material changes in Howard Hughes’ operating scope and financial engineering aimed at funding acquisitions and expanding portfolio breadth.

This transformative agenda implies a complex layering of business models that significantly broadens Howard Hughes Holdings’ operational footprint beyond previously well-understood real estate revenue streams.

Core Business Model and Established Master Planned Communities

Howard Hughes Holdings has traditionally generated revenues through the development and sale of master planned communities (MPCs), which represent large-scale residential land developments combining residential housing, retail centers, parks, schools, and infrastructure planning under unified designs. Flagship projects include Summerlin in Nevada and Bridgeland in Texas — communities recognized among top national sellers due to their integrated amenities and thoughtful urban planning [S1],[F1].

The economic engine derives primarily from land development economics: subdividing parcels into buildable lots sold to homebuilders or end buyers at premium prices reflecting location desirability amplified by community branding. This model benefits from relatively predictable sales absorption rates tied to regional housing demand fundamentals and secures long life-cycle returns via phased development over multiple years.

Summerlin's status as one of the highest-selling MPCs nationally imbues pricing power and enduring demand resilience, supporting steady cash flow generation even amidst macroeconomic housing cycles. Its high visibility also creates intangible brand equity aiding customer retention and builder partnerships.

Industry Structure and Competitive Positioning

Within the MPC sector, barriers to entry include securing land parcels at scale with entitlements, extensive regulatory approvals for zoning and infrastructure, plus significant upfront capital investment. Howard Hughes Holdings’ established scale provides competitive moats built on these hurdles combined with developed community reputations driving buyer preference.

By extending into diversified holdings beyond real estate—leveraging the partnership with Pershing Square—the company also accesses specialized investment expertise and enhanced capital availability that smaller or purely real estate-focused competitors lack [S1],[S7]. This hybrid positioning creates differentiated access to public markets capital via senior notes issuance ($1 billion aggregate principal amount issued through its subsidiary) supporting acquisition wings while maintaining core asset development [S8],[F1].

The evolving portfolio mixes recurrent real estate earnings with growth-oriented stakes in other industries expected to provide more stable income or upside potential not correlated directly with residential housing cycles.

Growth Drivers Underpinning Diversification and Real Estate Expansion

Growth is anchored by two intertwined engines:

- Acquisition Pipeline: Enabled by Pershing Square’s investment framework, HHH targets durable-growth public/private firms for controlling stakes intended to deliver stable cash flows complementary to the cyclical MPC revenues [S2],[S7]. The pace of consummating these deals will be a leading indicator for transformational success.

- Core Residential Demand: Sales momentum within Summerlin and Bridgeland continues to generate foundation revenues essential for internal funding capacity. Stable housing market dynamics in these geographies provide steady absorption rates supportive of phased lot sales at attractive price points [F1].

Capital deployment flexibility expanded through recent senior notes offerings enhances liquidity for both portfolio expansion and refinancing older debt tranches—the latter improving leverage profiles despite gross debt levels hovering above $5 billion due to scale-intensive development expenses [F1].

Risks and Execution Challenges in Transformation

The primary risk facing Howard Hughes Holdings lies squarely in execution complexity intrinsic to transitioning from a mono-industry developer into a multi-sector holding entity. Integration challenges loom large: identifying suitable acquisitions consistent with quality standards, cultural assimilation of diverse industry operators, achieving anticipated synergies without diluting focus on core MPC operations—all constitute material uncertainties outlined in risk disclosures [S2],[S7].

Moreover, cyclicality endemic to residential real estate markets could pressure margins if sales absorption weakens or input cost inflation intensifies even as new non-real-estate acquisitions bring their own sector-specific volatility.

Governance adjustments are underway reflecting this strategic pivot; notably, Director Ben Hakim’s announced resignation effective May 2026 introduces board-level succession dynamics amidst leadership recalibration linked intimately to Pershing Square involvement [S3],[S1]. Such transitions could momentarily disrupt oversight continuity during sensitive integration phases.

Upcoming Milestones and Near-Term Catalysts

Market participants should watch several forward-looking indicators closely:

- Subsequent announcements regarding acquisition targets finalized post-Pershing Square transaction completion will signal tangible progress towards diversification goals [S3].

- Further equity issuance activity via warrants or private placements could indicate ongoing capital raise success or appetite management from sophisticated investors [S3].

- Quarterly earnings releases will serve as barometers for integration performance metrics—profits contribution from new holdings plus sustained MPC sales volumes remain focal points.

- Board committee compositions to support increased governance complexity including technology and transaction oversight committees may be revisited in upcoming proxy filings ahead of the June 2026 annual meeting [S1],[S25].

Financial Snapshot: Balance Sheet Leverage and Liquidity Overview

Latest financial snapshot

| Metric | Value | Period |

|---|---|---|

| Cash & equivalents | $1469mm | |

| 2025-12-31 | ||

| Total debt | $5.1bn | |

| 2025-12-31 | ||

| Net debt | $3.7bn | |

| 2025-12-31 |

Source: SEC companyfacts cache [F1].

|| Metric | Value (USD) | |-----------------|--------------------| | Revenue | 1,474,892,000 | | Operating Income| 331,515,000 | | Net Income | 123,897,000 | | Cash & Equivalents | 1,468,507,000 | | Total Debt | 5,144,214,000 | | Net Debt | 3,675,707,000 |

Liquidity remains strong with cash balances near $1.47 billion juxtaposed against total debt exceeding $5.14 billion reflecting substantial ongoing investment activity typical for large-scale land developers undertaking multi-year phased builds [F1]. Net debt after accounting for cash reduces leverage but signifies cautious balance sheet management priorities aligned with upcoming acquisition spend requirements fueled by capital markets issuance.

Short-term refinancing risk is mitigated given recent successful senior note offerings (due in early 2030s) that allow incremental borrowing capacity while managing cost of funds prudently amidst prevailing interest rate environments [S8].

DISCLAIMER: This analysis is intended solely for informational purposes based on publicly available filings as of April 2026. It does not constitute investment advice or recommendations concerning securities of Howard Hughes Holdings Inc. Readers should perform their own due diligence before making any financial decisions.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments