Valero Energy Reports Strong Q1 Margins Reflecting Strategic Refinery Position

Valero’s Q1 2026 earnings demonstrate robust refining margins and liquidity, underpinned by integrated operations and a strong capital structure.

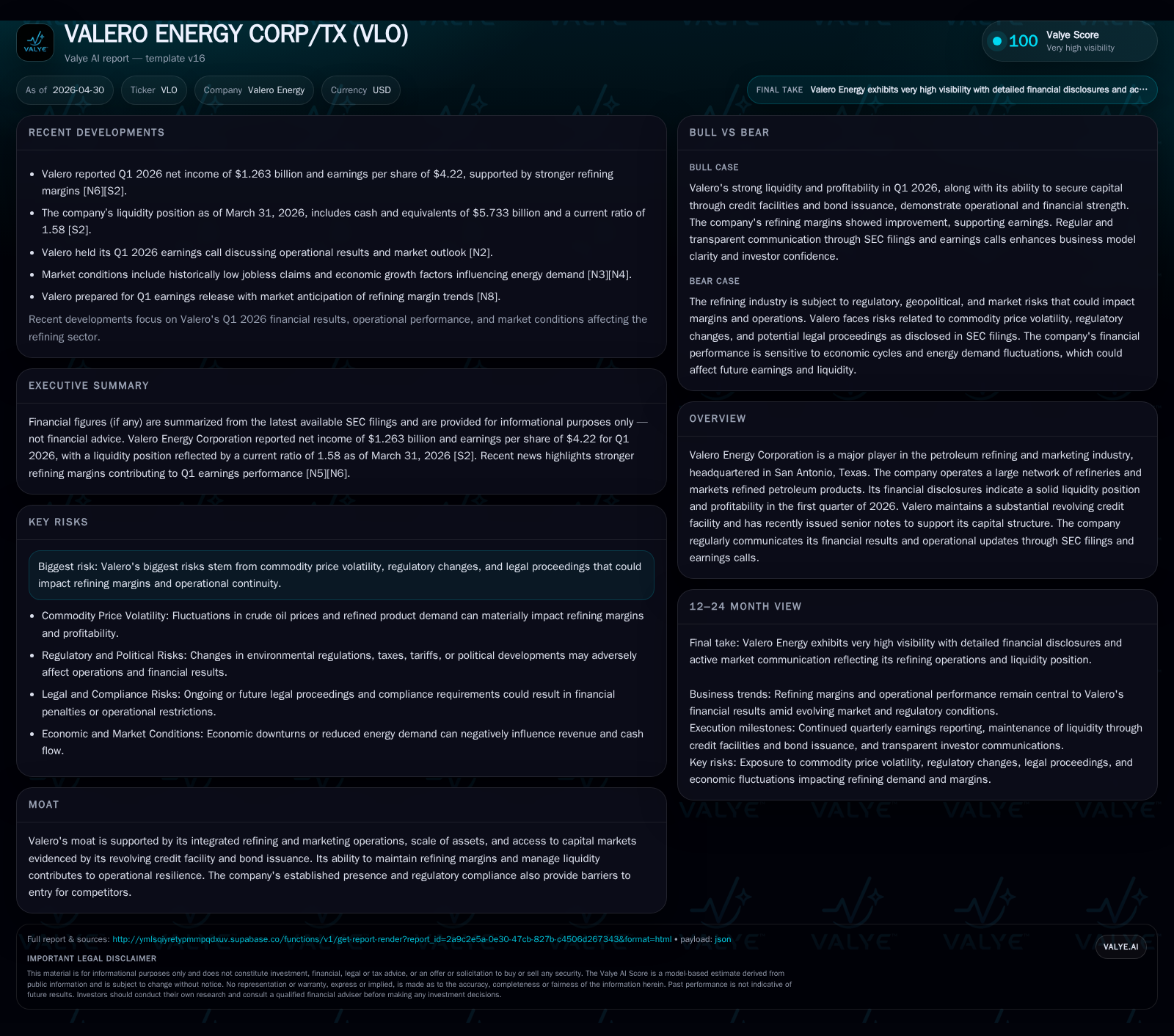

In Q1 2026, Valero Energy Corporation reported improved refining margins driving solid earnings performance amid ongoing commodity market volatility. The company’s vertically integrated business model spanning refining and marketing continues to provide scale advantages and resilience. Regulatory and legal risks persist but are managed within a stable capital framework supported by a sizable revolving credit facility and recent bond issuance. Key growth drivers include optimizing capacity utilization and expanding clean fuel production to capture evolving market demand.

Q1 2026 Operating Performance: Margin Expansion and Earnings Overview

Valero Energy’s latest quarterly filing for the period ended March 31, 2026 [S2][S3] reveals an operational backdrop defined by notably stronger refining margins that drove a positive earnings beat. The firm leveraged its complex refinery assets to enhance crack spreads—the differential between crude oil input costs and refined product prices—boosting profitability despite persistent commodity price volatility.

Operational cash flow generation remained healthy as reflected in the company’s liquidity position supported by cash & equivalents of $5.73 billion and net debt of $4.73 billion as of March 31, 2026 [F1]. Support for continued financial flexibility was reinforced through recent issuance of $850 million senior notes due 2036 [S18] alongside an amended $4 billion revolving credit facility extended through 2030 [S19]. These capital markets actions underpin the balance sheet as Valero navigates cyclical variability.

Business Model and Product Offering: Integrated Refining and Marketing Edge

Valero operates a vertically integrated model combining large-scale refinery operations with extensive downstream marketing channels [S1][S2]. This integration enables the company to optimize margin capture throughout the value chain—from strategically sourcing crude feedstocks to distributing refined transportation fuels and petrochemical feedstocks across diversified customer segments.

The breadth of refinery complexity allows processing of varied crude slates, enhancing feedstock flexibility which is critical amid fluctuating global crude pricing dynamics. Valero’s supply chain logistics and expansive branded retail presence improve end-customer accessibility while fostering consistent product quality and reliability—key differentiators sustaining customer loyalty in a commoditized market.

Industry Context: Refining Industry Dynamics, Competitive Position, and Regulatory Environment

The U.S. petroleum refining sector remains concentrated with sizeable barriers to new entrants due to high capital intensity, environmental permitting requirements, and stringent regulatory compliance related to emissions [S1][S4]. Valero commands a leading position with its asset scale and regional footprint benefiting from cost efficiencies and logistical access.

Industry-wide capacity utilization tends toward high levels, compressing margins during oversupply but benefiting integrated operators who can flex capacities or shift product mixes toward higher-value outputs such as low-sulfur diesel or renewable blendstocks. However, tightening environmental policies aimed at reducing carbon emissions impose ongoing operational challenges and potential cost escalations.

Growth Drivers: Capacity Management, Market Demand, and Margin Opportunities

Valero's growth strategy hinges on disciplined capital deployment targeting modernization and optimization projects that elevate refining yields while enabling cleaner fuel outputs aligned with evolving regulatory frameworks [S2][N8]. Incremental expansions in ultra-low-sulfur diesel processing capacity cater to rising market demand from transport sectors transitioning away from traditional fuels.

Strategic improvements in logistics infrastructure amplify distribution reach particularly in key U.S. regions supporting volume gains and competitive positioning. Additionally, active commodity hedging programs mitigate exposure to crude price swings preserving margin stability amidst cyclicality.

Risks and Headwinds: Commodity Cyclicality, Regulatory Pressure, and Legal Exposure

The firm's risk profile includes susceptibility to fluctuations in commodity prices affecting crack spreads which are inherently volatile given geopolitical tensions and varying demand-supply fundamentals [S21]. Regulatory pressures—particularly from environmental agencies—could further escalate compliance costs or curtail operations if emission targets tighten abruptly.

Legal proceedings detailed in recent filings also add an element of uncertainty impacting future cash flows or necessitating operational adjustments [S21][S4]. These factors represent watchpoints that may constrain growth or increase volatility in earnings.

Key Milestones and What To Watch Next: Guidance, Capital Allocation, and Market Signals

Market participants will closely monitor Valero's upcoming quarterly guidance updates alongside reported margin trajectories as indicators of sustained operational momentum [S2][N2][N14]. Progress reports on refinery upgrade initiatives or potential portfolio optimization moves will signal management’s execution effectiveness.

Additional focus areas include regulatory developments post-reporting period that may influence capital spending priorities or compliance frameworks shaping future returns.

Financial Snapshot and Balance Sheet Strength

Latest financial snapshot

| Metric | Value | Period |

|---|---|---|

| Cash & equivalents | $5.7bn | |

| 2026-03-31 | ||

| Total debt | $10.5bn | |

| 2026-03-31 | ||

| Net debt | $4.7bn | |

| 2026-03-31 | ||

| Current assets | $27.8bn | |

| 2026-03-31 | ||

| Current liabilities | $17.7bn | |

| 2026-03-31 | ||

| Current ratio | 1.58x | |

| 2026-03-31 |

Source: SEC companyfacts cache [F1].

Valero concludes Q1 2026 with robust liquidity reserves marked by cash & equivalents totaling $5.73 billion alongside total debt approximating $10.47 billion resulting in net debt near $4.73 billion [F1]. Recent capital market actions including senior note offerings support ongoing investment capacity while preserving balance sheet strength critical for weathering market fluctuations. This conservative financial posture complements operational resilience inherent in Valero’s integrated business platform.

| Metric | Value (USD billions) | Date |

|---|---|---|

| Cash & Equivalents | 5.73 | |

| 2026-03-31 | ||

| Total Debt | 10.47 | |

| 2026-03-31 | ||

| Net Debt | 4.73 | |

| 2026-03-31 | ||

| Current Assets | 27.83 | |

| 2026-03-31 | ||

| Current Liabilities | 17.65 | |

| 2026-03-31 |

This analysis is based solely on publicly available SEC filings dated up to April 30, 2026 [S1][S2][S3][S4][S18][S19][S21] augmented by companyfacts data snapshot [F1] without speculative forecasts or investment opinions.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments