Orion Digital Corp. Bolsters Platform Revenue with AI-Driven Wealth and Payments Expansion

Orion Digital reports member growth and evolving revenue mix, driven by AI-enhanced wealth management and expanded European payments infrastructure.

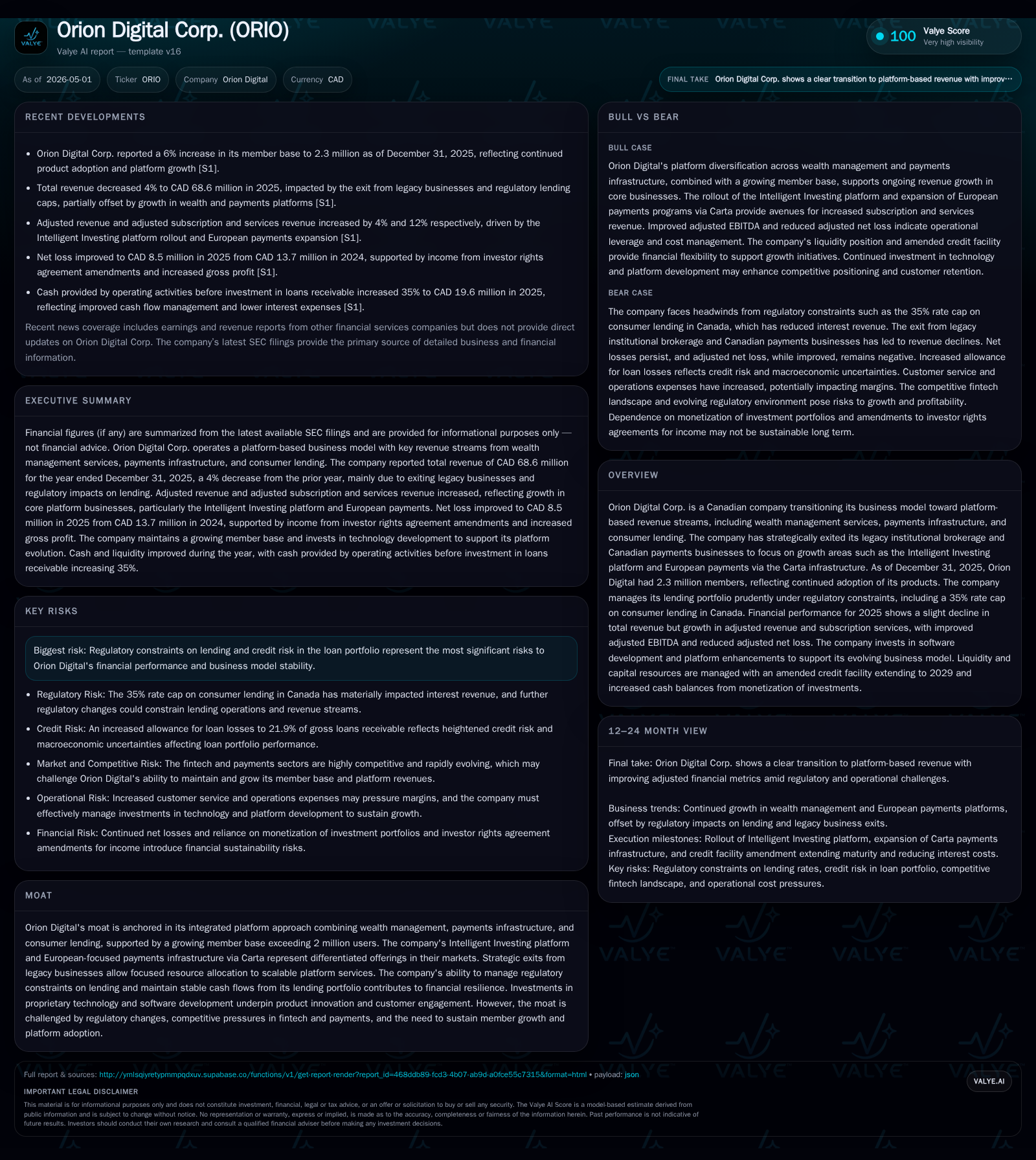

In its latest quarterly filing, Orion Digital Corp. disclosed a growing member base reaching 2.3 million users alongside shifts in revenue composition favoring subscription and platform services despite steady overall revenue contraction. The company continues to advance its strategic pivot away from legacy brokerage operations toward scalable digital platforms comprising the Intelligent Investing wealth service, Carta-powered European payments, and regulated Canadian consumer lending. This transition is supported by targeted investments in AI-driven automation and software development, positioning Orion to capitalize on platform economics while managing credit and regulatory constraints inherent in consumer lending. Key near-term growth drivers include member acquisition momentum, platform adoption rates, and geographic expansion of payments infrastructure. Risks center chiefly on regulatory lending limits and credit portfolio performance amid competitive fintech dynamics.

Latest Operating Developments: Q4 2025 and Q1 2026 Interim Updates

Orion Digital Corp.’s most recent quarterly filing dated April 2, 2026 [S2], complemented by the March interim report [S3], provides a clear snapshot of near-term operational progress underpinning its strategic evolution. Membership expanded approximately 6% year-over-year to 2.328 million users as of December 31, 2025, marking continued consumer adoption momentum despite macroeconomic headwinds.

Revenue trends reflect disciplined portfolio management decisions: total revenues edged down roughly 4% compared with the prior year primarily due to exits from legacy institutional brokerage activities and the impact of a regulatory-imposed cap on consumer loan interest rates (35% APR in Canada). Nonetheless, adjusted subscription and services revenues — driven chiefly by wealth management subscriptions alongside the growing payments business — remained resilient with modest contraction offsetting declines elsewhere.

Operationally, cash provided by operating activities before loan financing showed a strong increase (+46% YoY), boosted by lower interest expenses following credit facility amendments (lowered base rates) and inflows related to amended investor rights agreements (IRAs). Discretionary investments rose modestly to $1.0 million in Q4 reflecting intensified focus on AI-enabled automation in customer support functions and preparation for a unified intelligent investing platform slated for launch within 2026.

The loan portfolio experienced measured growth with gross loans receivable increasing to $77.6 million year-end while maintaining prudent risk controls evidenced by an allowance for loan losses approximating 22% of loan balances; this increase accounted for updated macroeconomic assumptions underscoring proactive credit loss provisioning.

Business Model Evolution: From Legacy Brokerage to Integrated Platform Services

Orion’s operating model has undergone a decisive transformation away from episodic revenues linked to institutional brokerage toward integrated recurring platform income streams anchored in three pillars: wealth management via Intelligent Investing; payment processing infrastructure leveraging Carta’s European network; and regulated Canadian consumer lending.

This transition emphasizes generating stable subscription average revenue per user (ARPU) combined with transaction-based fee income facilitating scalability without commensurate increases in variable cost structures. By strategically exiting less scalable legacy businesses, Orion reallocates capital toward proprietary technology development that underpins differentiated customer experiences across its touchpoints.

Wealth services represent the fastest-growing component as customers increasingly adopt AI-augmented automated portfolio management solutions designed to improve risk-adjusted returns while embedding subscription-measured engagement metrics that reinforce loyalty.

Payments infrastructure leverages complex cross-border clearing capabilities uniquely positioned via Carta’s compliance-focused rails across Europe—an advantageous departure from competitive pressures saturating North American domestic payment corridors.

Meanwhile, regulated consumer lending continues as a stable cash flow engine but is deliberately constrained within strict jurisdictional caps on interest rates ($35$25 APR ceiling) requiring dynamic originations adjustments consistent with regulatory expectations.

Product and Technology Quality: Intelligent Investing, Carta European Payments, and Lending

Product differentiation pivots on Orion's ability to seamlessly integrate advanced technologies across its core offerings:

- Intelligent Investing harnesses machine learning algorithms to drive personalized portfolio rebalancing, tax-loss harvesting optimizations, and risk scenario modeling enhancing user outcomes versus traditional robo-advisor models.

- Carta-powered payments facilitate complex multi-currency settlements compliant with EU Payment Services Directives enabling rapid cross-border transactions optimized for cost efficiency relative to SWIFT-reliant alternatives common among incumbents.

- Consumer Lending products are actively managed for credit performance employing forward-looking macroeconomic indicators embedded within IFRS 9 provisioning models; this prudence balances capital deployment against elevated charge-off risks inherent in unsecured subprime exposures within Canada's regulated framework.

The concerted software development thrust exhibits ongoing investment into automation of customer support workflows using natural language processing bots coupled with data-driven fraud detection systems improving operational efficiency metrics while mitigating losses attributable to fraud or delinquency.

Competitive Positioning Within Fintech and Payment Infrastructure Markets

Orion stakes a middle ground between vertically siloed pure-play fintechs focusing narrowly on either wealth or payments versus broad traditional financial services incumbents struggling with legacy tech drag. Its moat arises from:

- Cross-product integration creating higher switching costs through unified user experiences spanning investing accounts linked naturally with payment capabilities plus access to tailored consumer credit offers without external intermediaries.

- Geographic diversification favoring European payments expansion where Carta's licensed infrastructure confronts less saturated ecosystems compared to highly commoditized North American payment rails.

- Proactive regulatory navigation especially around Canadian lending rate caps differentiates it from looser governance environments that may experience sudden policy shocks affecting risk frameworks.

While competitive pressures persist—from established robo-advisors offering zero-fee models leveraging scale data assets to international payment firms scaling rapidly—Orion's hybridized service set combined with continuous innovation in AI-driven service delivery provides defensible positions across multiple fintech market segments.

Growth Opportunities: Scaling Membership, Platform Adoption, and Geographic Reach

Key avenues for scaling include:

- Member Growth: Expanding beyond the current base of approximately 2.3 million members remains foundational; incremental acquisitions translate directly into stronger network effects across platform services enhancing average spend per user.

- Platform Revenue Upsell: Deeper monetization through tiered subscription upgrades within Intelligent Investing alongside increased payment transaction volume via Carta integrations represents measurable KPIs driving recurring revenues.

- European Payments Expansion: Further geographic rollout leveraging Carta’s licenses offers significant runway given underpenetrated cross-border SME segments seeking compliant yet cost-effective payment partners.

- Software Automation Gains: Initiatives expanding AI-enhanced customer interaction platforms reduce personnel-related costs while increasing responsiveness sustaining margin improvement amid expanding scale.

- Balanced Credit Growth: Judicious expansions of the loan book calibrated against evolving macroeconomic conditions with automated early-warning systems for delinquency minimizing loss severity.

Close monitoring mechanisms including quarterly Board reviews of cyber risks further underscore operational governance priorities mitigating non-financial threats impacting mission-critical systems reliability [S1].

Monitoring Key Milestones: Member Growth Metrics, Product Launches, Regulation Watchpoints

To evaluate the robustness of Orion’s strategy execution post-latest quarter disclosures:

- Track incremental net new member additions exceeding Q4’s reported +36K quarterly gains as a proxy for demand traction [S13].

- Observe roll-out timelines and initial adoption statistics for the unified intelligent investing platform anticipated mid-to-late 2026 reflecting AI integration effectiveness [S15].

- Assess growth metrics for Carta-enabled payment volumes including new merchant onboardings indicative of successful European market penetration [S1].

- Monitor adherence reports on Canadian lending compliance ensuring rate cap observance paired with quality indicators like delinquency ratios signaling portfolio health [S1].

- Watch disclosures around discretionary investment spend trends in software automation alongside attrition or churn rates further clarifying margin sustainability prospects [S10].

These milestones collectively shape a transparent lens into whether operational progress solidifies sustainable growth trajectories aligned with stated long-term objectives outlined in annual filings [S1].

This analysis is drawn strictly from Orion Digital Corp.'s publicly filed SEC disclosures up through April 30, 2026. It does not constitute investment advice but aims to provide an operationally grounded view of business developments relevant for stakeholders assessing company quality amid ongoing industry evolution.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments