GreenTree Hospitality Group’s 2025 Operating Shift Highlights Challenges and Strategic Opportunities

GreenTree’s latest quarterly results reveal near-term operational pressures balanced by asset-light franchise growth and solid liquidity.

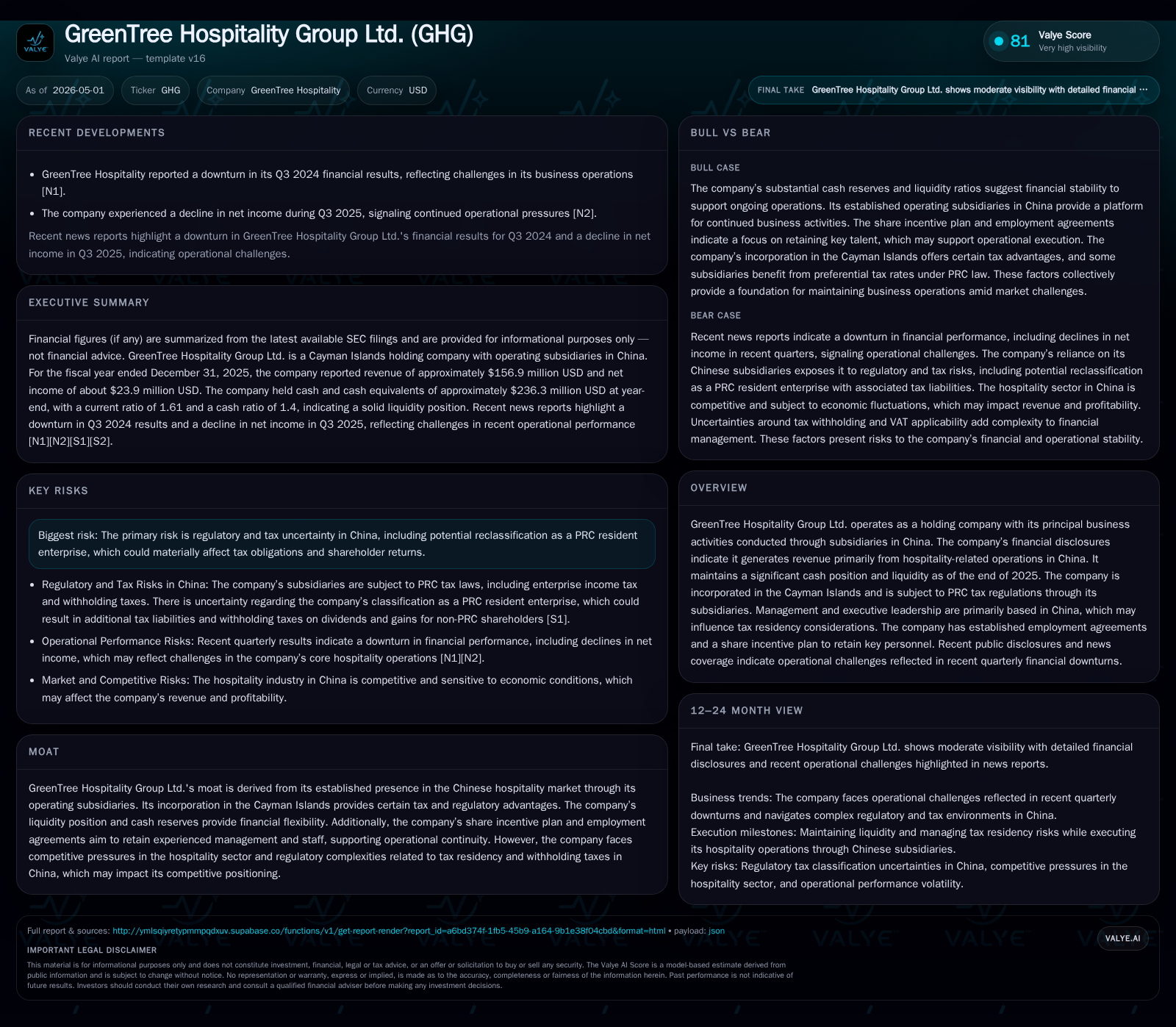

GreenTree Hospitality Group Ltd. reported Q3 2025 results indicating slower hotel openings and a margin impact from ramp-up costs of newer franchised hotels. The company’s pure-play franchise model drives revenue primarily through management fees across a large, diversified brand portfolio targeting economy to mid-upscale tiers in China. While its broad network expansion underpins structural growth, regulatory uncertainties over PRC tax residency and lease rights pose material risks. Financially, GreenTree maintains strong liquidity with $236 million in cash and modest net debt, providing a buffer amid profitability pressures. Key watchpoints include execution on new hotel maturation, franchisee recruitment stability, and management responses to regulatory challenges.

Recent Quarterly Financial Results and Operational Update

GreenTree Hospitality Group’s Q3 2025 filing ([S2]) disclosed a slowdown in net hotel openings, with only 255 hotels opened against 100 closures during the year. This marks a deceleration from prior years where net additions were higher, reflecting cautious expansion amid evolving market conditions. Revenue drivers remained consistent with the franchise model; however, operating income margins experienced pressure due to the cost structure of newly opened hotels still within their typical six-month ramp-up period. These ramp-up hotels yield lower franchise fees as occupancy rates build gradually, diluting margin expansion found in mature properties.

Despite these operational headwinds, GreenTree maintained robust cash reserves as confirmed by year-end balance sheet data ([F1]), suggesting disciplined financial management amid growth challenges.

Business Model and Brand Portfolio Driving Growth

GreenTree operates as a pure-play franchised hotel operator in China ([S1]). Unlike asset-heavy competitors, it leverages an asset-light model where revenue is largely derived from franchise management fees charged to franchised-and-managed hotels. As of December 31, 2025, its network encompassed 4,580 hotels with over 327,000 rooms spread across all major Chinese provinces and municipalities.

The company’s diverse brand portfolio includes economy, mid-scale, business-oriented, and mid-to-upscale offerings tailored to various consumer segments and franchisee capabilities. This segmentation allows GreenTree to address multiple market needs while facilitating partner selection aligned with location demographics.

Supporting this model is a scalable franchise management system bolstered by direct sales channels, an established loyalty program, and proprietary technology solutions designed to optimize operational efficiency for franchisees and enhance guest satisfaction.

Additionally, GreenTree’s restaurant division complements its hospitality footprint with a growing number of street stores delivering affordable dining options that serve mass consumer demands, although this segment remains smaller relative to its core lodging business.

Competitive Dynamics in Chinese Hospitality Franchising

China's hotel franchising industry remains highly fragmented with numerous regional players competing on price and location access ([S1]). GreenTree ranks fourth nationally by room count—a significant scale advantage—but must continuously defend market share against rivals expanding aggressively.

Its geographically diversified network encompassing over 355 cities mitigates concentration risk but introduces complexity regarding local regulations and property leasing arrangements. Legal challenges linked to leased property usage have emerged as notable operational risks that may increase costs or force closures if contested ([S1]).

Pricing power exhibits typical softness seen in highly competitive segments like economy hotels; thus maintaining brand standards and service consistency is critical for customer retention.

Key Growth Drivers: Network Expansion and Franchisee Ecosystem

GreenTree’s long-term top-line growth depends on increasing its mature hotel base—those operational beyond six months where stable fees contribute positively—and recruiting quality franchisees who can sustain brand standards ([S1]). The transition from ramp-up to mature operation marks a pivotal margin inflection point.

From 2012 through 2025, the group grew hotel count at a CAGR of approximately 14.5%, while room growth maintained near 12.5%, signaling sustained expansion backed by franchise demand.

Technological tools that streamline booking systems, pricing intelligence, and customer relationship management underpin improved revenue generation across fragmented franchise locations.

Restaurant expansions through street stores present incremental revenue diversification potential by leveraging the existing customer base adjacent to hospitality sites.

Risks Spotlight: Regulatory, Tax Residency, and Lease Challenges

Among GreenTree's most material risks is regulatory ambiguity concerning its classification under China's Enterprise Income Tax (EIT) Law ([S1]). Specifically, if deemed a "resident enterprise" based on where its de facto management body residesin this case potentially Chinaits global income could be subjected to tax implications including higher withholding taxes on dividends affecting shareholder returns.

Further complicating matters are disputes over leased property rights integral to the operation of franchised hotels ([S1]), where changes in land-use approvals or enforcement actions could disrupt revenues or require costly legal responses.

The regulatory environment remains dynamic with incomplete precedents governing these issuesfueling uncertainty that directly impacts strategic agility.

Near-Term Watchpoints: Execution and Market Conditions

Key upcoming monitoring points involve quarterly reporting updates on net hotel growth trajectories post-Q3 moderation ([N1], [S2]). Observers should closely track occupancy improvements for recently launched hotels exiting ramp-up phases alongside maintenance of franchise recruitment momentum.

Management commentary on dealing with margin pressures induced by slower scaling or rising costs will be scrutinized for strategic shifts such as price adjustments or brand repositioning.

The ability to navigate regulatory headwinds while sustaining operational cadence may dictate confidence in longer-term forecasts.

Latest Financial Position: Liquidity, Leverage, and Profitability Snapshot

Latest financial snapshot

| Metric | Value | Period |

|---|---|---|

| Cash & equivalents | $236mm | |

| 2025-12-31 | ||

| Total debt | $37mm | |

| 2025-12-31 | ||

| Net debt | $-200mm | |

| 2025-12-31 | ||

| Current assets | $271mm | |

| 2025-12-31 | ||

| Current liabilities | $169mm | |

| 2025-12-31 | ||

| Current ratio | 1.61x | |

| 2025-12-31 |

Source: SEC companyfacts cache [F1].

Financially, GreenTree entered 2026 with a solid liquidity position holding $236 million in cash & equivalents versus approximately $36.6 million total debt—yielding a favorable net cash posture of about $200 million ([F1]). Operating income for the full year ended December 31, 2025 was $8.1 million on revenues nearing $157 million. Net income came in at roughly $24 million reflecting margin pressure but maintaining profitability ([F1]).

Cash flow from operations declined sequentially from prior years ($40.2 million in 2025 vs higher levels earlier), partly attributable to increased impairment charges linked to goodwill and long-lived assets during gradual portfolio adjustments ([S2], [S7], [S8]).

Capital expenditure outflows primarily related to prepayments for property & equipment underscore continued investment into network infrastructure albeit within disciplined bounds ([S20]).

Overall financial metrics indicate resilience supportive of growth investments despite near-term profitability headwinds rooted in operating scale dynamics.

Disclaimer: This analysis is based solely on disclosed SEC filings and publicly available information as of May 2026. It does not constitute investment advice.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments