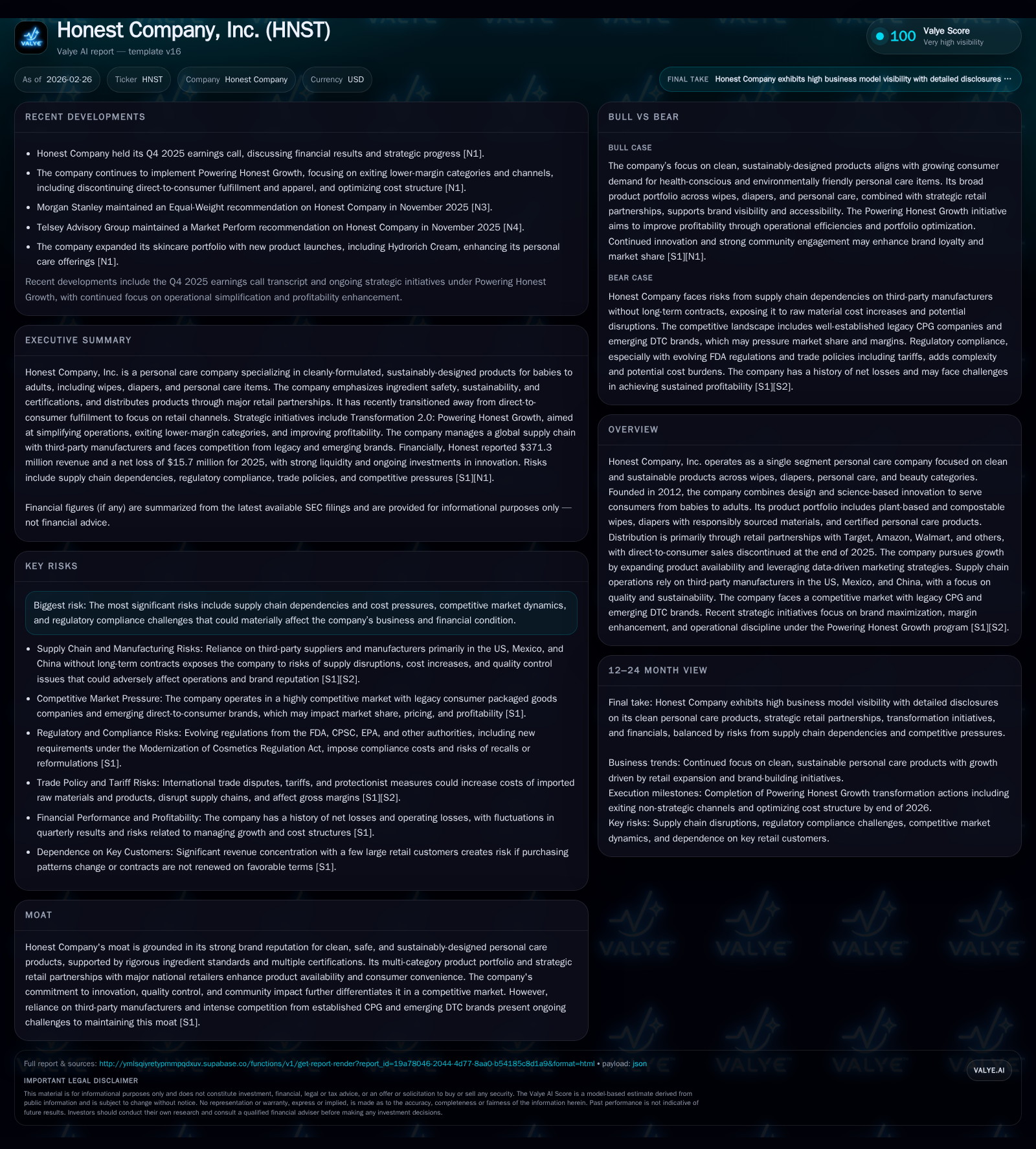

Honest Company Focuses on Retail Expansion and Margin Improvement Post-DTC Exit

Shifting from direct-to-consumer to retail partnerships, Honest Company pursues growth through expanded distribution and product innovation amid profitability challenges.

Honest Company, Inc., a personal care brand rooted in clean and sustainable products, reported mixed financial results for fiscal 2025 with modest revenue decline and ongoing operating losses. The company strategically exited its direct-to-consumer channel at the end of 2025 to improve gross margins, reinforcing reliance on retail partnerships with major retailers such as Target, Amazon, and Walmart. While revenue slightly declined year-over-year, operating cash flow surged sharply due to operational efficiencies and cost management initiatives. Honest is investing in marketing, product innovation, and share repurchases as it seeks to strengthen brand awareness and expand physical and digital availability despite competitive pressures and supply chain risks.

Historical Performance

Honest Company's financial performance for fiscal year 2025 reflected strategic changes amid ongoing profitability challenges. Annual revenue declined modestly by about 1.9%, from $378.3 million in 2024 to $371.3 million in 2025 [F1]. This decrease was partly attributable to the discontinuation of the direct-to-consumer (DTC) channel at year-end 2025 — prior sales through Honest.com contributed materially but incurred high shipping and fulfillment costs that pressured margins [S1][S24]. Despite this top-line softness, the company achieved notable improvement in operational cash flow.

Operating income deteriorated significantly: losses widened from -$6.3 million in FY24 to -$18.5 million in FY25 [F1]. Net losses deepened similarly from -$6.1 million to -$15.7 million over the same period [F1], underscoring persistent challenges with profitability despite transformation efforts.

Meanwhile, operating cash flow surged from a modest positive $1.5 million in FY24 to $15.1 million for FY25 — an increase exceeding 880% — supported by non-cash items such as an apparel inventory write-down and stock-based compensation alongside tighter working capital management [F1][S6]. Capital expenditures rose but remained moderate at approximately $1.51 million for FY25 reflecting continued investments in technology and fulfillment [F1][S11].

Historical performance (annual)

| FY | Net ($mm) | CFO ($mm) | OpInc ($mm) | Capex ($) | Net YoY |

|---|---|---|---|---|---|

| 2025 | -16 | 15 | -18 | 1510000 | -156.1% |

| 2024 | -6 | 2 | -6 | 530000 | +84.4% |

| 2023 | -39 | 19 | -39 | 1838000 | +20.0% |

| 2022 | -49 | -76 | -50 | 1617000 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | Div | FCF ($mm) | ROE% |

|---|---|---|---|

| 2025 | 14 | -9.2 | |

| 2024 | 1 | -3.5 | |

| 2023 | 0 | 18 | -31.9 |

| 2022 | 0 | -78 | -33.5 |

Source: SEC companyfacts cache [F1].

Note: Negative operating and net income reflect ongoing losses while improving cash flows indicate enhanced liquidity generation.

Business Model & Operational Shifts

Founded in 2012 with a focus on cleanly formulated personal care products spanning wipes, diapers, personal care, and beauty categories, Honest has built brand equity grounded in sustainability standards like plant-based materials for wipes and responsibly sourced fluff pulp for diapers [S28]. The company operates as a single reportable segment focused primarily on the U.S., with all long-lived assets located domestically even though manufacturing occurs across the U.S., Mexico, and China [S10][S19].

A pivotal strategic shift during FY25 was ending the DTC model that relied on sales via Honest.com since inception but became financially unsustainable due to high fulfillment shipping costs relative to retail models [S24]. The website remains active solely as an educational platform directing consumers toward partner retailers’ online portals.

Retail partnerships thus constitute the core growth vector: agreements with Target (since 2014), Amazon (since 2017), Walmart (since 2022), among others provide extensive physical store presence and online availability [S28]. While these alliances enhance brand exposure and operating leverage, diaper sales faced setbacks related to retailer footprint changes or exclusive SKU preferences adversely impacting volumes with expectations that these trends will persist near term [S24].

Product innovation remains integral within this retail framework to reinforce margins—recently demonstrated by launching Hydrorich Cream expanding skincare options targeting adult consumers which complements core wipes and diaper lines known for clean ingredient certifications including National Eczema Association endorsements [N3][S28][S11]. The company prioritizes accretive product launches focusing on wipes and personal care segments that generally carry better margin profiles compared to other categories.

Marketing & Brand Development

Marketing investments increased year over year reflecting efforts to modernize customer acquisition leveraging paid, owned, earned media channels supported by proprietary consumer insights analytics [S22]. This multi-channel approach aims at deepening engagement within existing customers while efficiently attracting new consumers during aggressive physical retail expansion.

Cost control remains delicate — Honest continuously targets operational improvements as part of its Brand Maximization Transformation initiative focusing on logistics and marketing spend optimization without compromising brand trust or product quality critical for consumer loyalty given baby care sensitivities [S1][S22].

Financial Position & Capital Allocation

Cash and equivalents stood robust at $89.6 million at end-2025 providing ample liquidity alongside undrawn availability of approximately $31.6 million under a revolving credit facility maturing April 30, 2026 [F1][S4][S7]. No borrowings were outstanding under this facility at year-end supporting prudent leverage management.

The company currently does not pay dividends reflecting reinvestment priorities toward growth initiatives rather than shareholder cash distributions [S25]. However, it authorized a $25 million share repurchase program starting February 2026 intended to be funded from operating cash flows and existing liquidity — signaling confidence in capital efficiency amidst strategic repositioning efforts [S25].

Improving operating cash flows amid ongoing net losses suggest advancing financial health post-restructuring though sustained profitability remains a key milestone.

Risks & Litigation Exposure

Operational dependencies on key third-party manufacturers represent critical supply chain risks alongside potential cost inflation pressures that could further compress margins if unmanaged effectively [S17][S23]. Notably all diapers are sourced from one supplier while wipes rely predominantly on another single vendor raising concentration concerns atypical for companies of Honest’s scale compared to diversified peers.

Legal proceedings include settlements totaling $20 million related to securities class action claims fully covered by insurance receivables; derivative litigation matters have been provisionally settled pending court approval involving smaller amounts [S8][S12]. Ongoing disputes with suppliers post-contract terminations introduce potential operational or financial volatility though currently at early stages with uncertain impacts [S12].

Regulatory risks encompass compliance with evolving environmental sustainability standards that serve both as competitive differentiators and sources of incremental compliance costs across jurisdictions plus trade tariffs affecting imported components manufactured outside the U.S., potentially increasing supply costs unpredictably [S18][S20]. Privacy regulations impose additional compliance requirements given reliance on digital marketing necessitating robust cybersecurity measures against breaches that could damage reputation or incur penalties.

Future Growth Outlook & Milestones To Watch

While explicit management guidance is limited publicly, key areas monitored include:

- Continued shelf space expansion across mass retailers including Target/Walmart/Amazon plus penetration into specialty/drugstore/club retailers;

- Scaling newer skincare product lines contributing incremental margin-accretive revenue;

- Execution efficiencies improving gross margins post-DTC exit focused on inventory management and logistics;

- Effectiveness of marketing spend applying data analytics driving customer acquisition versus cost ratios;

- Outcomes of supplier litigations potentially impacting apparel or ancillary portfolio contributions;

- Realization of announced share buyback impacts on capital structure;

- Consumer preference shifts towards sustainable clean-label products amid intensifying competition.

Absent explicit numeric guidance beyond general commentary on distribution expansion imperatives investors must evaluate results against stated priorities while considering macroeconomic impacts on discretionary consumption patterns typical of personal care sectors.

Conclusion

Honest Company navigates a critical juncture balancing growth ambitions rooted in sustainability branding against persistent profit deficits stemming from channel transitions and competitive pressures within personal care markets. Exiting direct-to-consumer sales represents a decisive move toward wholesale-led scale advantages aimed at improving gross margins amidst supply chain complexities.

Revenue contraction paired with strong operating cash flow improvement suggests enhanced structural efficiency bolstered by disciplined working capital tactics though profitability remains fragile pending consistent earnings above breakeven.

Robust cash reserves alongside undrawn credit facilities plus a new buyback program underscore conservative financial stewardship committed to long-term value creation.

Nevertheless, material risks related to concentrated supplier relationships alongside ongoing litigation require sustained management focus while investing adequately into innovation pipelines essential for differentiation as consumer demand shifts increasingly favor sustainable clean-label products amidst fierce competition from established incumbents and digitally native brands transitioning into brick-and-mortar channels.

Disclaimer: Analysis based solely on information available through February 26, 2026 from company filings ([F1],[S#]) and recent news reports ([N#]). It does not constitute investment advice or recommendations regarding Honest Company stock or securities.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments