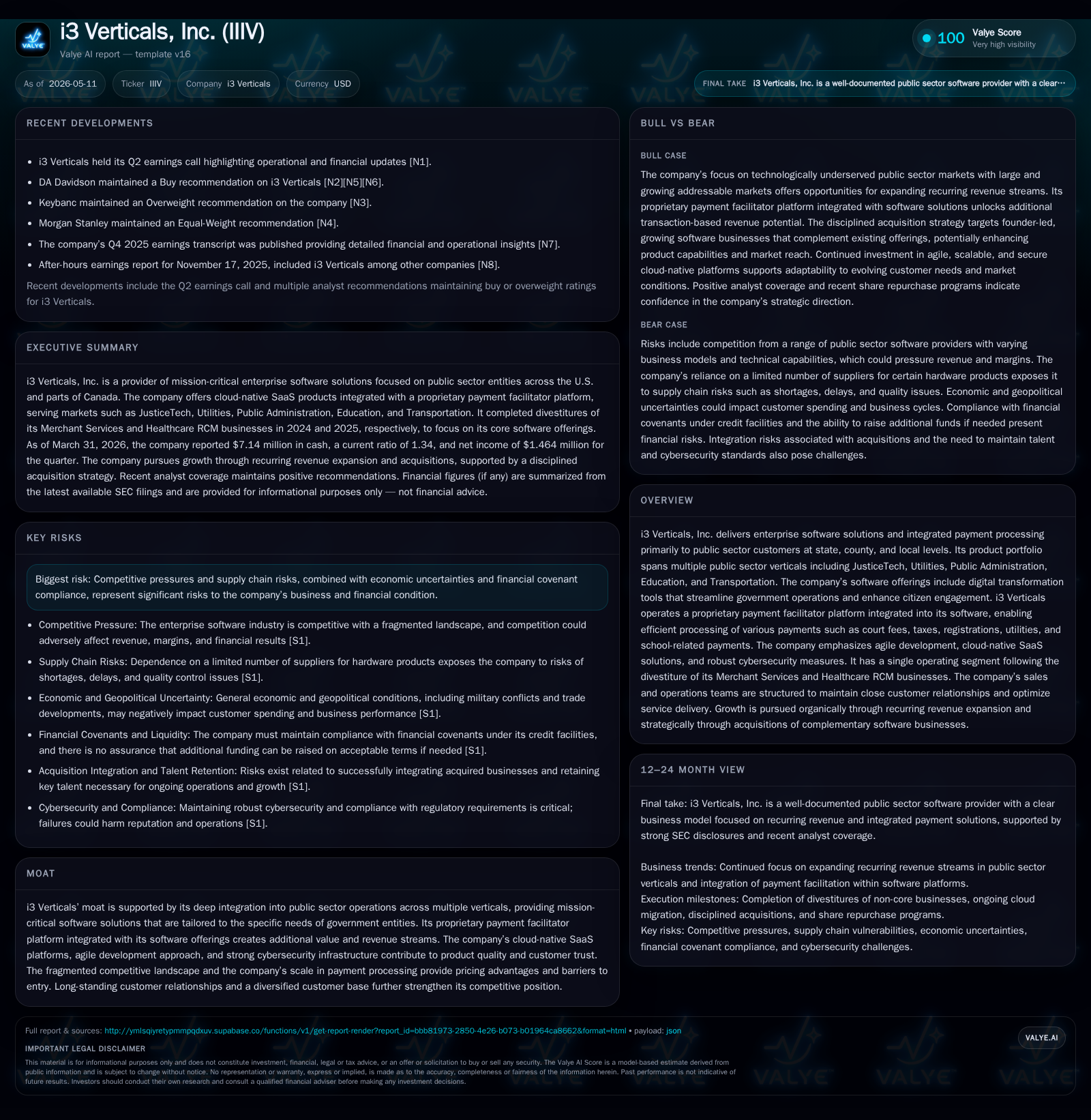

i3 Verticals Recalibrates Growth and Capital Return Focus in Public Sector Software

Latest quarterly results reveal i3 Verticals’ strategic pivot to core public sector SaaS, robust capital return completion, and growth in vertical payment integration.

In the quarter ended March 31, 2026, i3 Verticals completed a significant $51 million share repurchase program, underscoring a disciplined capital return focus amid stable revenue performance after strategic divestitures. The company’s business model centers on cloud-native software solutions integrated with a proprietary payment platform, deeply entwined in public sector verticals like justice, utilities, education, and transportation. This integration creates sticky customer relationships and diversified transactional revenue streams. While the competitive landscape remains fragmented with barriers to entry rooted in regulatory complexity and cybersecurity demands, i3 Verticals leverages scale in payments processing as a moat. Growth opportunities hinge on expanding digital transformation initiatives in state and local governments and increasing payment transaction volume. Key risks include ongoing cybersecurity exposure linked to sensitive data handling and regulatory compliance pressures. Upcoming quarters will be closely watched for evidence of operational scalability and further balance sheet management.

Latest Quarterly Performance Highlights and Their Implications

i3 Verticals' second quarter ended March 31, 2026, marked a pivotal moment with the culmination of two share repurchase programs totaling approximately $51 million spent to buy back about 2.22 million shares at an average price of $22.70 per share [S2][S3]. This aggressive capital return activity occurred without any unregistered equity sales reported during the period [S2], indicating a conservative approach to raising external capital amid strong cash flow generation. Meanwhile, the company maintained revenue stability despite prior strategic divestitures of its Merchant Services segment in late 2024 and the Healthcare Revenue Cycle Management (RCM) business in mid-2025 [S1]. These moves emphasize a clear strategic refocus on core SaaS offerings tightly embedded within public sector domains.

The share repurchases exhaust the authorized August 2025 program early in Q2 before transitioning fully into the new February 2026 buyback authorization that itself reached capacity within the same quarter [S2]. This swift execution signals robust internal cash generation supported by operational discipline without reliance on incremental debt—total debt stood at zero as of September 30, 2025 [F1]. Revenue recognized in the latest available full fiscal year ending September 30, 2025 was just above $54.9 million with positive operating income margins reflecting sustained demand post-divestitures [F1]. The company's ability to simultaneously execute financial returns while consolidating its business portfolio materially shapes investor perception around capital efficiency.

Core Business Model: Public Sector SaaS and Payment Processing Integration

i3 Verticals operates primarily through a single segment focused on delivering enterprise software solutions tailored explicitly for state and local public sector clients across JusticeTech, Utilities, Transportation, Education, and Public Administration verticals [S1][S25]. Its offerings are high-touch cloud-native SaaS platforms developed with an agile methodology emphasizing continuous deployment cycles for feature refinement aligned to client-specific workflows.

A distinctive differentiator is the integrated proprietary payment facilitator platform baked directly into their governmental software suites. This platform powers efficient electronic payment processing for myriad government-related transactions including court fees, property taxes, utility bills, registrations, school lunch payments, licensing fees among others [S25]. This coupling not only broadens revenue sources beyond subscription or license-based models but also fosters strong customer retention due to mission-critical dependency on seamless transaction facilitation coupled closely with operational software.

The revenue mechanics involve contracted recurring fees for SaaS access alongside transactional fees derived from payment volumes processed through their systems. Pricing power benefits from deep vertical expertise—products accommodate regulatory complexity inherent to government agencies—reducing substitution risk and creating switching costs. Agile development ensures responsiveness to regulatory changes or evolving constituent demands enhancing solution relevance over time.

Competitive Landscape and Industry Dynamics in Government Technology Solutions

i3 Verticals operates within a fragmented market largely composed of smaller regional players offering point solutions without cohesive integrated payment capabilities or cloud-native architecture [S1]. The public sector technology environment is characterized by demanding procurement cycles complicated by regulatory scrutiny around data security and compliance requirements mandated by payment networks such as Visa and Mastercard.

Barriers to entry are pronounced stemming from the need for certified secure environments suited to handle highly sensitive personal data (driver’s license numbers, social security numbers), adherence to evolving cybersecurity standards, and tailored productization that matches highly regulated workflows unique to verticals like courts or motor vehicle departments [S1]. Scale emerges as a key competitive advantage given aggregate transaction volumes enhance negotiating leverage with payment networks while funding ongoing R&D investment.

i3 Verticals’ moat therefore combines entrenched customer relationships—often built over decades—and technology integration that embeds deeply into administrative processes reducing ease of replacement. Its agile approach contrasts with legacy competitors still reliant on dated infrastructure giving it time-to-market advantages for new features responsive to government digital transformation initiatives.

Growth Opportunities in Vertical-focused Innovation and Market Penetration

Growth avenues largely stem from accelerating public sector digitalization mandates that push agencies toward modern SaaS solutions complemented by streamlined e-payment options [N1]. The JusticeTech vertical continues upgrading court management systems incorporating enforcement tracking plus online fee collections—a growth vector fueled by court system modernization grants.

In Utilities and Transportation sectors—the addition of compliance management capabilities tied to environmental standards or motor carrier regulations unlocks cross-selling potential within existing client bases [S1]. Education segment innovation includes enhanced meal program management integrated with school event ticketing platforms that increase transaction flow within districts leveraging i3's ecosystem.

Geographically, expansion into underserved localities or Canadian provinces remains possible given the company’s broad North American footprint yet lumpy distribution of modernized agency adoption. Further enhancement of analytics modules providing actionable insights for policy makers could open premium service tiers.

KPIs likely linked to growth include rising transaction counts through the payment platform—directly correlating with revenue uplift—and backlog or customer renewal rates evidencing stickiness amid rising digital engagement mandates [N1]. Post-divestiture focus appears set to intensify investment in R&D fostering sustained innovation designed to capture escalating public spend budgets allocated toward IT modernization.

Key Risks: Cybersecurity, Regulatory Compliance, and Competitive Pressures

i3 Verticals faces pronounced cybersecurity risks given its custodianship of protected personal information across government domains [S1]. Prior litigation concerning alleged cybersecurity inadequacies underscores ongoing exposure—not merely abstract but directly impacting reputation and financial liabilities via potential fines or remediation costs.

Payment processing subjects the company to rigorous compliance regimes imposed by network partners such as Visa/Mastercard along with federal/state regulations governing transaction integrity. Any failure or third-party partner breach could lead to significant sanctions potentially disrupting operations or triggering costly legal proceedings [S1].

Competitive pressures arise as smaller niche providers attempt entry but lack integrative breadth; however some incumbents may seek consolidation via acquisitions targeting i3’s served markets. Economic fluctuations impacting public agency budgets translating into slower IT spending cycles pose cyclical risk aspects particularly when political climates shift priorities away from technology investments.

The company must also navigate financial covenant constraints under its revolving credit facilities although current zero-debt posture mitigates immediate balance sheet leverage concerns [F1]. Emphasis on internal controls and cyber defense investments remains paramount moving forward.

Upcoming Catalysts and Execution Watchpoints

Near-term milestones include monitoring quarterly guidance related to sales pipeline conversion especially following recent product enhancements targeted at justice and transportation verticals mentioned in earnings commentary [N1][S2][S3]. Adoption rates of newly launched SaaS modules integrating advanced payment capabilities should be assessed as proof points for scaling efficiency.

Further capital allocation moves remain anticipatable post-repurchase wave—whether incremental buybacks or potential dividend initiatives pending free cash flow excess after reinvestment priorities [N1][S2]. Tracking KPIs such as net new customers added per vertical or transaction processing volume increments will illuminate market traction magnitude.

Execution risks lie in maintaining seamless migration support amidst continuous deployment frequency without service interruptions—a non-negotiable for public sector clients reliant on uptime for sensitive operations. Cybersecurity incident reporting transparency will also be a focal governance angle moving forward.

Financial Overview and Capital Structure Snapshot

Latest financial snapshot

| Metric | Value | Period |

|---|---|---|

| Cash & equivalents | $7mm | |

| 2026-03-31 | ||

| Current assets | $78mm | |

| 2026-03-31 | ||

| Current liabilities | $59mm | |

| 2026-03-31 | ||

| Current ratio | 1.34x | |

| 2026-03-31 |

Source: SEC companyfacts cache [F1].

i3 Verticals enters Q3 2026 with a clean balance sheet featuring no total debt outstanding as of September 30, 2025 combined with $7.14 million cash & equivalents at March-end 2026 [F1]. Current assets total $78.21 million versus liabilities near $58.57 million yielding a healthy current ratio of approximately 1.34 signaling comfortable liquidity coverage [F1].

The recently completed $51 million share buyback utilized substantial operating cash flow without stretching liquidity buffers—a prudent reflection of confidence in ongoing earnings power while returning value efficiently to shareholders [S2][F1]. No defaults on senior securities were reported during the period reinforcing financial discipline [S2].

| Metric | Value |

|---|---|

| Cash & Equivalents | $7.14M |

| Total Debt | $0 |

| Current Assets | $78.2M |

| Current Liabilities | $58.57M |

| Current Ratio | 1.34 |

| Net Debt | -$7.14M |

| Shares Repurchased Q2 | ~2.22M shares |

| Repurchase Spend Q2 | $51.0M |

This conservative capital structure supports flexibility for selective investment back into key vertical innovations or opportunistic acquisitions aligned with public sector digital transformation themes.

Disclaimer: This analysis is based solely on publicly filed documents including SEC filings (10-Ks/10-Qs/8-Ks) up to May 8, 2026, secondary news sources cited herein dated May 7–8, 2026, and company facts database snapshots contemporaneous thereto.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments