Peering into the Shadows: International Media Acquisition Corp.'s Financial Ambiguity and Liquidity Peril

A comprehensive analysis of IMAQ’s scarce disclosures reveals a fragile financial footing overshadowed by opaque operations and investor withdrawal.

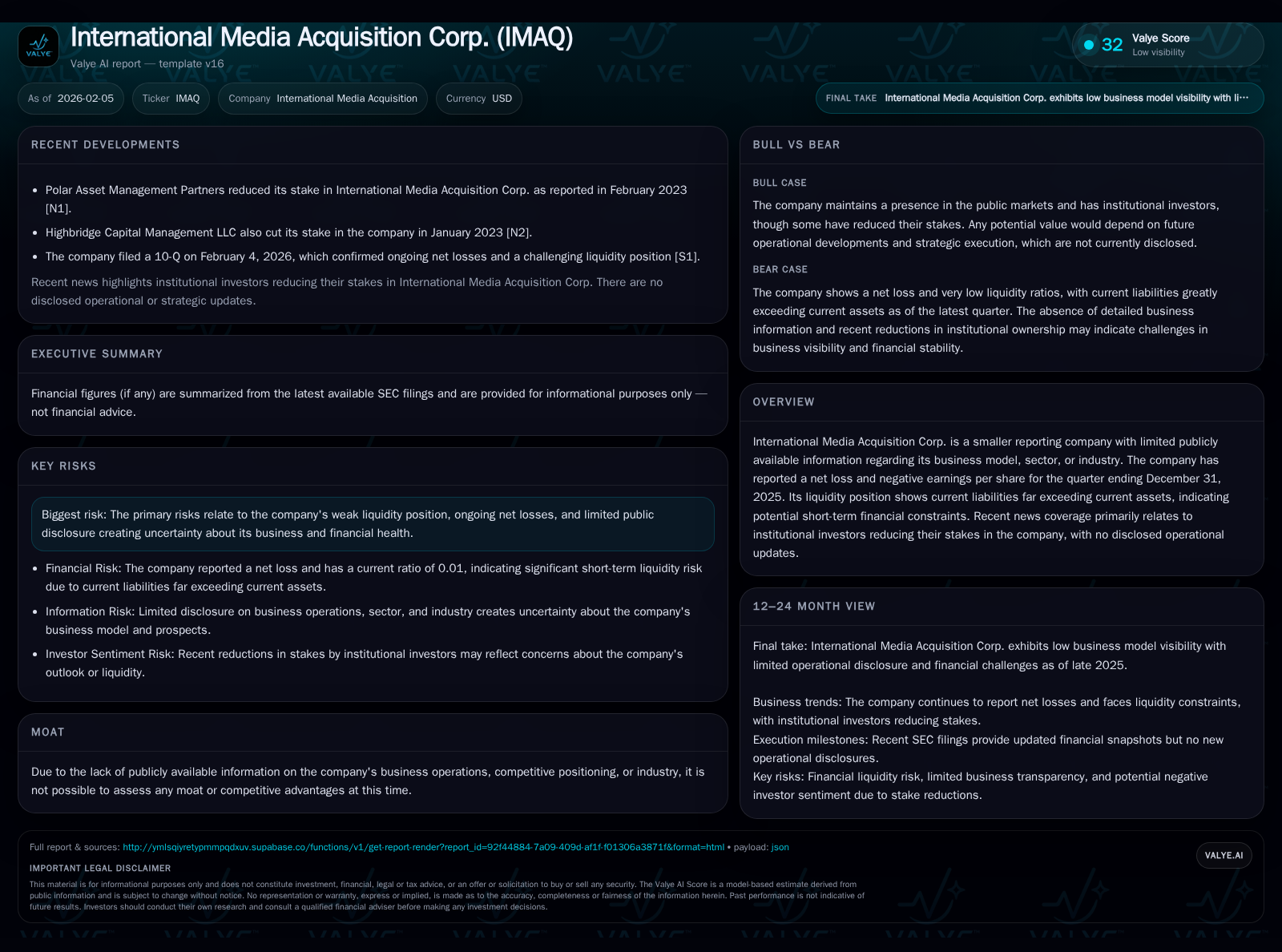

International Media Acquisition Corp. remains shrouded in opacity, with limited public disclosure hindering typical business assessment. Its balance sheet exposes stark liquidity challenges, including current liabilities vastly exceeding assets, coupled with persistent quarterly net losses. Institutional investors have been retreating despite no new operational revelations, underscoring market skepticism amid unclear strategic direction. Without identified competitive advantages or clarity on its business model, the company’s near-term outlook hinges on addressing financial vulnerabilities and enhancing transparency.

A Company Behind the Veil: Limited Disclosures and Their Implications

International Media Acquisition Corp. (IMAQ) presents itself as an enigma within publicly accessible financial landscapes. The company classifies as a smaller reporting entity but diverges sharply from standard disclosure expectations. Absent are clear indications of its sector affiliation, industry focus, or specific operational modalities. This scarcity handicaps any conventional analytical approach that relies on contextualizing metrics within industry benchmarks or competitive dynamics.

Such opacity raises immediate concerns for stakeholders attempting to gauge viability or growth prospects. Without foundational knowledge of what the company actually does or the markets it serves, assessing trajectory moves beyond conjecture into speculation. Even basic sector or industry classification fields remain unpopulated across filings and databases [F1], spotlighting an unusual lack of granularity.

Dissecting the Balance Sheet: A Crisis in Liquidity

Delving into the latest reported financials unveils a pronounced imbalance on IMAQ's balance sheet dated December 31, 2025. The company's current assets stand at approximately $75,916 while current liabilities tower near $7.19 million — an alarming mismatch that translates into a current ratio approximating 0.01 [F1].

This ratio implies severe short-term solvency issues, signaling that immediate obligations outweigh liquid resources by nearly two orders of magnitude. Such a position could impede routine operational financing and cast doubt over going-concern assumptions if unaddressed promptly.

Cash and equivalents specifically registered just $1,177 at year-end 2023 [F1], an amount negligible relative to outstanding payables. The data suggests either reliance on imminent financing events or internal measures yet uncommunicated to stakeholders.

Persistent Losses and What They Reveal

Alongside liquidity woes, IMAQ reports continuing negative earnings momentum. The net loss recorded for Q4 2025 was about $59,590 [F1], modest in absolute terms but emblematic of an absence of meaningful revenue generation or cost control breakthroughs.

Without disclosed revenue trends or segment reports, this loss figure cannot be dissected further but clearly indicates ongoing operational expenditures exceeding income streams. In isolation, such a loss might be manageable; combined with the liquidity crisis it magnifies sustainability doubts.

Investor Behavior: Institutional Exodus Without Operational News

Market behavior adds another dimension to IMAQ's predicament. Recent partial unwindings of institutional holdings have been noted despite a lack of fresh updates concerning new contracts, product launches, strategic partnerships, or leadership changes [valye_report_excerpt].

This divergence between investor retreat and stagnant corporate messaging exposes an unsettling information asymmetry. It suggests institutional stakeholders may harbor deteriorating confidence based on non-public insights or reassessments driven purely by adverse balance sheet and earnings data.

Contextualizing Risk Factors From Historical Filings

While quarterly filings omit new risk factor disclosures due to smaller reporting status [S2], earlier Annual Reports shed light on enduring vulnerabilities. The last comprehensive filing confirmed risks centered on fragile financial condition and opaque business operations remain intact without material amendments.

These persistent risk outlines emphasize challenges related to capital adequacy, dependency on external funding sources, uncertain cash flow generation capabilities, and lack of established competitive foothold—all key axes for potential adverse impacts on future results.

The Elusive Moat: Can a Competitive Advantage Be Found?

Attempts to isolate any proprietary edge or durable competitive advantage falter against IMAQ's informational void. No identifiable business lines, intellectual property assets, customer bases, or market differentiators emerge from public documents.

Without clarity regarding its operational domain or strategic initiatives, the notion of a moat is purely hypothetical at best. This absence heightens exposure to market competitiveness and constrains bargaining power in financing dialogues.

Speculating on Strategic Intentions Amidst Data Silence

In the absence of explicit corporate communication outlining future plans or strategic pivots, only cautious inference can be offered regarding possible paths forward. Potential strategies might involve equity injections to bolster liquidity; asset sales; mergers; restructuring; or even winding down operations if capital avenues close off.

However, these scenarios remain abstract constructs given limited factual anchors—underscoring an imperative for the company to enhance disclosure practices to bridge stakeholder information gaps.

What Lies Ahead? Potential Scenarios Rooted in Current Facts

Looking ahead longitudinally through the prism of present facts reveals several probable developments:

- Liquidity management will dominate priority as bridging massive short-term liability coverage gaps demands urgent attention.

- Investor patience may wane further, escalating share price pressure absent transparent turnaround narratives.

- Operational continuity depends heavily on securing additional capital resources or restructuring agreements in coming quarters.

- Disclosures enhancing transparency could mitigate mistrust, potentially stabilizing investor relations if substantive progress occurs.

- Failure to act decisively risks exacerbating downward spirals, leading to deeper financial distress or eventual insolvency procedures.

Altogether, IMAQ stands at a crossroads where obscurity compounds fiscal fragility — creating a complex scenario demanding informed scrutiny and prudent monitoring rather than traditional performance-based optimism.

Disclaimer: This analysis solely synthesizes publicly available information without offering investment opinions or forecasts. Readers should conduct independent due diligence before deriving conclusions.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments