InfuSystem’s Financial Upswing and Strategic Risks in Medical Infusion Tech

InfuSystem Holdings reports significant profit and cash flow growth bolstered by favorable regulatory changes, while confronting reimbursement uncertainties and liquidity considerations.

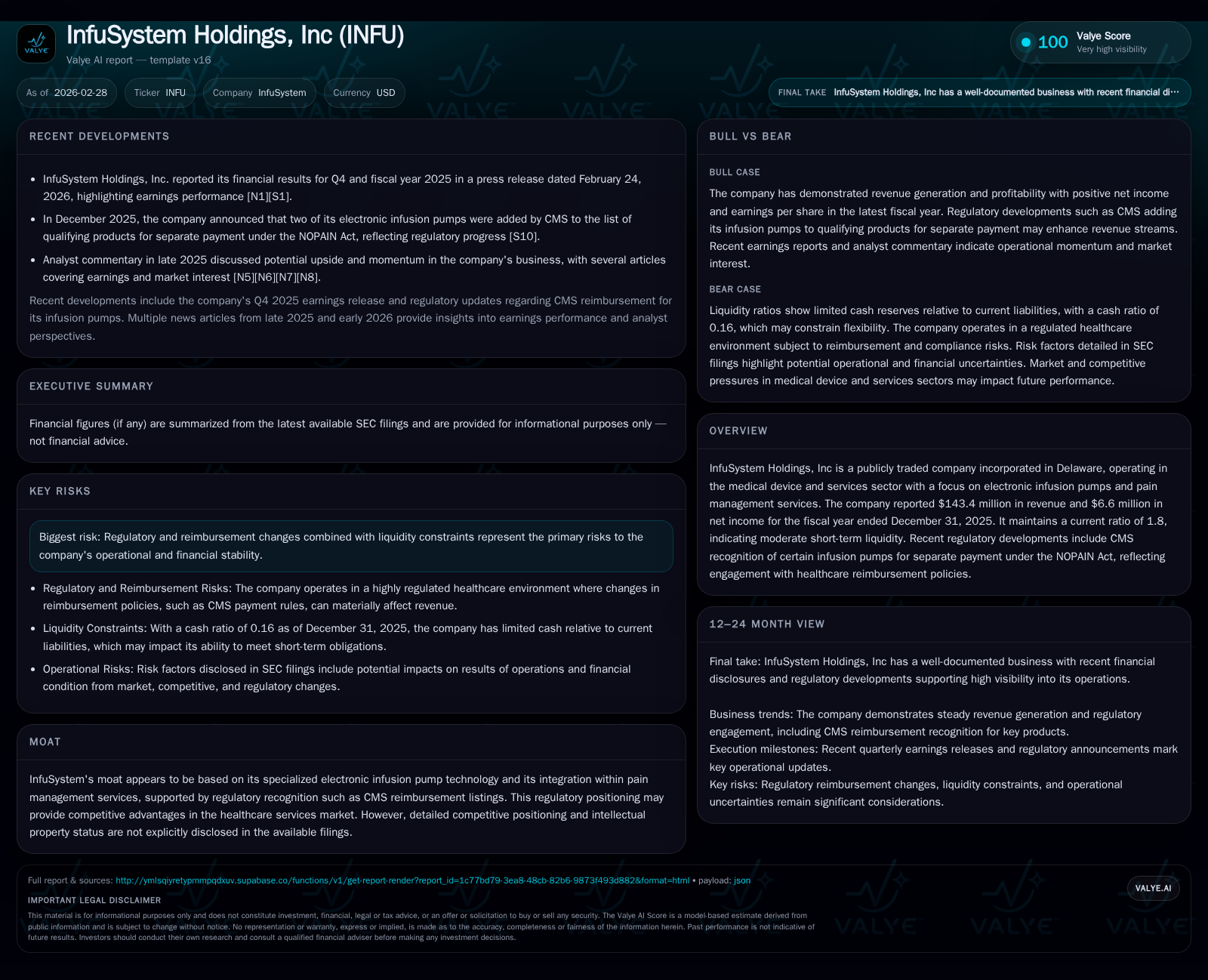

InfuSystem Holdings, a provider of electronic infusion pumps and pain management services, delivered solid financial results for FY2025 with revenue growing 6.4% to $143.4 million. Operating income surged 73% and net income more than doubled, reflecting enhanced operational efficiency and favorable payer dynamics, including CMS’s recognition of select infusion pumps under the NOPAIN Act. Despite robust free cash flow supporting an aggressive $9.9 million share repurchase program, the company faces ongoing risks from regulatory shifts and liquidity constraints. Monitoring future reimbursement policies and capital deployment will be critical for assessing InfuSystem’s sustainability in a competitive healthcare equipment niche.

InfuSystem’s Growth Trajectory: Revenue and Profit Momentum

InfuSystem Holdings’ latest fiscal year showcased marked top-line and bottom-line improvements reflecting strengthening demand for its electronic infusion pumps and related pain management services.[F1] Revenue climbed to $143.4 million in FY2025 from $134.9 million the prior year, representing a solid 6.4% growth rate that outpaces several legacy healthcare device peers navigating slower adoption cycles.[F1] This growth was supported by gradual market penetration expansions and sustained service contract contracts within core clinical settings.

Profitability metrics accelerated sharply during the period: operating income leapt by 73% year-over-year, reaching $11.9 million from just $6.9 million in FY2024.[F1] This uplift corresponds with operational leverage gains and tighter cost controls amid rising revenues. Net income exhibited an even more striking advance—surging over 180% to $6.6 million compared to $2.3 million the previous year.[F1]

From a cash flow perspective, InfuSystem demonstrated enhanced efficiency and cash conversion: operating cash flow rose to $24.4 million in FY2025, up approximately 19%, while capital expenditures contracted nearly half (down ~49%), yielding robust free cash flow of nearly $23.9 million.[F1] The substantial reduction in capex points toward more asset-light operational models or completed investment cycles which favor sustainable free cash generation.

These financial trends occur against the backdrop of strategic investments into electronic infusion pump innovation—an area where product reliability and compliance with evolving regulations are key drivers for customer retention across ambulatory and hospital settings.

Historical performance (annual)

| FY | Rev ($mm) | Net ($mm) | CFO ($mm) | OpInc ($mm) | Rev YoY | Net YoY |

|---|---|---|---|---|---|---|

| 2025 | 143 | 7 | 24 | 12 | +6.4% | +182.6% |

| 2024 | 135 | 2 | 20 | 7 | +7.2% | +168.9% |

| 2023 | 126 | 1 | 11 | 4 | +14.4% | +4744.4% |

| 2022 | 110 | 0 | 18 | 2 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | Buybacks ($mm) | FCF ($mm) | ROE% |

|---|---|---|---|

| 2025 | 10 | 24 | 11.6 |

| 2024 | 1 | 19 | 4.1 |

| 2023 | 0 | 10 | 1.7 |

| 2022 | 5 | 17 | 0.0 |

Source: SEC companyfacts cache [F1].

Financial figures in millions USD; YOY = Year-over-Year percentage change.

Regulatory Developments Fueling Competitive Edge

A pivotal catalyst underpinning InfuSystem’s improved performance is the Centers for Medicare & Medicaid Services (CMS) designation of select electronic infusion pumps used in its Pain Management service line as eligible for separate payment under the Non-Opiods Prevent Addiction in the Nation (NOPAIN) Act.[S16][N1] This regulatory acknowledgment effectively integrates these devices into established reimbursement codes offering incremental payer coverage beyond bundled payments.

Within medical device reimbursement landscapes, such coding recognition creates durable pricing power — enabling InfuSystem to command differentiated pricing via enhanced clarity in payer reimbursement pathways.[S16] The company highlighted this as a strategic enhancement facilitating broader clinical adoption at institutions mindful of cost transparency and compliance mandates.

This regulatory moat reduces customer switching incentives while leveraging CMS standards as a market access barrier for competitors lacking similar code designations or integration expertise.[S1][S3] Given growing scrutiny on opioid alternatives for pain mitigation, medical providers increasingly prioritize devices compliant with federal initiatives such as NOPAIN, which elevates InfuSystem’s positioning in pain management ecosystems.

Capital Allocation: Buybacks, Free Cash Flow, and Returns

Free cash flow strength empowered InfuSystem to substantially expand share repurchases during FY2025 relative to preceding years.[F1] The company bought back nearly $9.9 million worth of stock—up markedly from just over $1 million repurchased in FY2024.[F1] Such capital return signals management confidence grounded in robust operating cash flows without compromising liquidity.

With free cash flow estimated at roughly $23.85 million (operating cash flow less capex), InfuSystem maintains room for balanced reinvestment alongside shareholder distributions.[F1] Dividend distributions do not appear prominent or material based on filings,[F1] placing buybacks front-and-center as the chosen mechanism for returning value.

The firm also reported an approximate return on equity (ROE) of 11.6%, calculated from trailing net income over average equity values—reflecting improved utilization efficiency given rising net profits coincident with stable equity levels around $57 million.[F1] This ROE magnitude aligns with mid-tier medtech peers emphasizing steady returns amid moderate growth phases.

Liquidity Position and Balance Sheet Health

InfuSystem manages a current ratio of approximately 1.8x at fiscal year-end 2025,[F1] underscoring reasonable short-term financial flexibility with current assets significantly outstripping liabilities ($36 million vs ~$20 million).[F1] Cash plus equivalents amounted to about $3.2 million—a moderate liquidity buffer within overall working capital balances.[F1]

Although the company has heightened liquidity ratios since earlier periods,[S8][S12] SEC risk disclosures emphasize inherent exposure stemming from reimbursement policy uncertainties and operational financing demands.[S4][S5] While no significant long-term debt stress is evident,[F1] management remains attentive to safeguarding capital structure amid ongoing margin pressures linked to healthcare policy flux.

Forward Outlook: Market Positioning and What to Watch

Explicit forward guidance remains limited; however, InfuSystem’s February 27, 2026 investor presentation underscores continued focus on leveraging FDA clearance pipelines alongside CMS reimbursement alignments as key strategic drivers.[S3][N1]

Future catalysts likely revolve around expansion of reimbursable device portfolios under evolving federal programs targeting non-opioid pain therapies, alongside potential partnerships or service line optimizations hinted at but not yet detailed publicly.[S3]

Relevant indicators include shifts in revenue composition favoring higher-margin pump rentals or maintenance contracts, trajectory of capital expenditure plans reflecting tech upgrades versus legacy system phase-outs,[F1][S3] plus buyback cadence adjustments reflecting free cash evolution.

Risk Factors: Reimbursement Shifts and Operational Challenges

In its most recent 10-K filings dated February 27, 2026,[S4][S5] InfuSystem cites typical healthcare sector risks centering on payer reimbursement volatility substantially influencing operating margins and service income sustainability.

Ongoing legislative or regulatory rule modifications could alter coverage policies unexpectedly, compressing revenue streams tied directly to device payment codes especially within federal healthcare programs such as Medicare/Medicaid.[S4]

Legal proceedings disclosed are not characterized as material but underscore industry-wide litigation risks affecting medtech companies broadly.[S4]

Operationally, the costs associated with stringent compliance adherence—ranging from manufacturing quality controls to cybersecurity of connected infusion systems—pose continuous cost pressures that may constrain profitability absent offsetting revenue gains.[S5]

Liquidity pressures cited reflect a need for prudent balance sheet stewardship amidst unpredictable payer behavior and potential contract renegotiations with hospital networks or outpatient centers.[S7]

This report presents an impartial review based solely on publicly available financial data and regulatory disclosures pertaining to InfuSystem Holdings, Inc., without recommending any investment actions.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments