iQSTEL Inc Advances Revenue and Market Presence with 2025 Financial Highlights

The company disclosed its full-year 2025 financial results alongside operational commentary underscoring revenue growth and marketplace milestones.

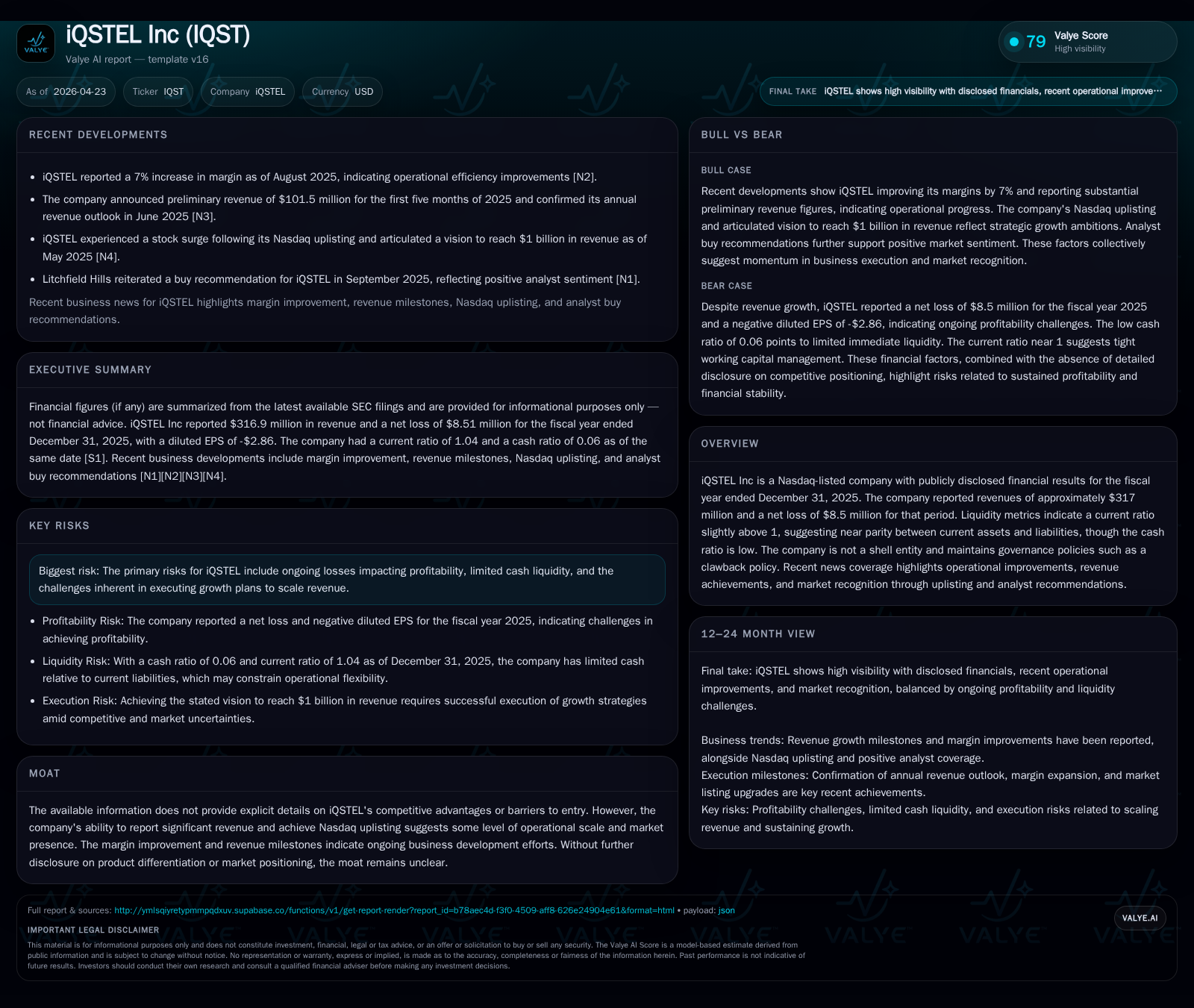

iQSTEL Inc announced record revenues of approximately $317 million for fiscal year 2025, marking double-digit top-line growth while incurring a net loss of $8.5 million. The recent Nasdaq uplisting reflects the firm's expanding operational footprint, although profitability and liquidity metrics reveal ongoing challenges. Its telecom-centric service offering underpins revenue expansion, but margin pressures and modest cash reserves present constraints. Going forward, execution on scaling clients and managing financial flexibility will be critical determinants of sustained progress.

2025 Financial Results and Recent Company Updates

iQSTEL Inc publicly released its fourth quarter and full year ended December 31, 2025 financial results via an April 6, 2026 Form 8-K filing [S3]. The company reported total revenues of approximately $316.9 million for the fiscal year, representing an 11.9% increase over the prior year’s top line of $283.2 million [F1]. This marks a solid revenue milestone evidencing sustained demand traction in iQSTEL’s core service segments.

However, despite the topline gains, the company recorded a net loss of about $8.5 million in 2025, exacerbating the prior year's loss of roughly $6 million [F1]. Operating income was negative $4.25 million, deteriorating substantially compared to a smaller loss in 2024. The widening losses reflect pressure on margins, possibly from rising costs or aggressive sales investments outlined during the accompanying earnings conference call held April 7th, as summarized in exhibits to the filing [S3].

The company's recent uplisting to the Nasdaq Capital Market is a noteworthy step indicative of growing market recognition and operational scale; it potentially enhances liquidity profiles for investors but also implies heightened reporting rigor [S3][S1]. This listings milestone aligns with the firm's expanding footprint yet contrasts with persistent profitability headwinds.

iQSTEL's Business Model: Revenue Sources and Customer Value

iQSTEL primarily operates within telecommunications infrastructure and cloud connectivity solutions tailored for enterprise clients and global carriers [S1]. Its revenue streams derive from services such as international long-distance voice traffic transit, interconnection services among multiple carrier networks, IP/MPLS network services, and cloud-based communications platforms.

The company’s business model involves aggregating telecom voice routes and cloud connectivity to resell capacity at scale — effectively acting as an intermediary facilitating global communication flows. This demands robust network integration capabilities coupled with regulatory compliance across multiple jurisdictions.

Customer retention benefits from contractual relationships with carriers requiring reliable traffic transit and cloud interconnectivity solutions that often entail switching costs due to technical integration complexity and quality-of-service commitments. While explicit proprietary technologies or exclusive agreements are not highlighted in filings, iQSTEL positions itself around network quality assurance and flexible service packages tailored to client needs [S1].

Overall unit economics depend on volume transmission margins that can be thin due to commoditized telecom wholesale environments but can improve through scale and premium service add-ons.

Competitive Environment and Industry Positioning

the telecommunications intermediary space where iQSTEL competes is marked by fragmented providers ranging from large-scale incumbents to regional wholesalers. Pricing power tends to be limited because voice and IP transit services commoditize quickly under competitive pressure.

The industry is also shaped by regulatory compliance requirements that demand operational agility to navigate cross-border data handling and licensing rules.

Though iQSTEL lacks explicit disclosure of strong moats such as patented technology or exclusive market access, its revenue scale approaching $317 million indicates competitive capability sufficient to sustain Nasdaq listing standards [S1][S3]. However, margin compression evident in operating losses suggests pricing or cost competitiveness remains challenging.

There is no direct indication of severe supply chain limitations or network capacity constraints in filings; however, incremental network upgrades or partnerships likely require capital allocation decisions impacting profitability.

Key Drivers Accelerating Growth and Potential Headwinds

iQSTEL’s growth prospects rest on increasing global data traffic volumes driven by enterprise digitization trends, rising cloud adoption requiring inter-network connectivity, and expanding international communication needs that boost long-distance voice traffic volumes [S1][S3]. These drivers are fundamentally structural rather than cyclical given ongoing demand for digital interconnectivity.

Management’s commentary emphasizes pursuing new contracts leveraging cloud service integrations alongside enhancements in network visibility tools showcased during investor presentations [S3]. Such initiatives aim at broadening service relevance beyond commoditized voice transit.

Conversely, persistent net losses reflect cost structure challenges including investment overheads in technology platforms and sales efforts. Additionally liquidity constraints—with cash barely above $2 million against over $4 million debt—limit financial flexibility for growth investments or unexpected expenses [F1].

The current ratio around 1.04 indicates tightly balanced working capital with little buffer for volatility or adverse events [F1],[S3]. These factors represent execution risk layers capable of slowing trajectory if not addressed through effective capital management or operational efficiencies.

Upcoming Catalysts and Execution Risks to Monitor

Going forward, key performance indicators for iQSTEL will include contract renewal rates, customer acquisition metrics especially tied to cloud service offerings, regulatory compliance achievements given international telecom jurisdiction complexities, and any announced financing efforts to shore up liquidity [S3][S10].

Investor materials stress governance improvements such as adoption of a clawback policy as corporate risk mitigation aligned with Nasdaq standards [S1], signifying attention to oversight quality which could affect investor confidence levels.

Failure to convert new bookings into positive operating leverage or inability to manage debt maturities could materially impact outlooks. Monitoring quarterly updates (when available) for cash flow trends along with strategic partnership announcements will offer useful progression markers.

Consolidated Financial Overview and Liquidity Profile

Historical performance (annual)

| FY | Rev ($mm) | Net ($mm) | CFO ($mm) | OpInc ($mm) | Rev YoY | Net YoY |

|---|---|---|---|---|---|---|

| 2025 | 317 | -9 | -4 | -4 | +11.9% | -42.0% |

| 2024 | 283 | -6 | -3 | -1 | +96.0% | -685.0% |

| 2023 | 145 | -1 | -1 | 0 | +55.0% | +87.2% |

| 2022 | 93 | -6 | -2 | -3 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | FCF ($mm) | ROE% |

|---|---|---|

| 2025 | -4 | -52.3 |

| 2024 | -3 | -83.0 |

| 2023 | -2 | -9.1 |

| 2022 | -2 | -88.3 |

Source: SEC companyfacts cache [F1].

Data reflect continuing revenue growth (+11.9%), yet escalating operating losses (-409.8%) causing net losses deepening by over 40%. Operating cash flow remains negative highlighting ongoing capital consumption exceeding depreciation levels despite modest capex spend reflecting a lean asset base typical for software/telecom resellers [F1].

iQSTEL’s equity increased compared with prior year but serves primarily as buffer against losses not yet supporting profitability returns given negative ROE (~-52%) calculated from annual net income relative to shareholder equity [F1]. Capital structure shows moderate leverage with net debt roughly $2 million above cash balances illustrating manageable but non-negligible financial risk given slim liquidity ratios [F1].[S6][S7]

In sum,the financial profile supports narrative of a growth-focused telecom/cloud intermediary striving for scale amid margin pressure compounded by tight liquidity which must be carefully managed through disciplined execution.

Disclaimer: This report is for informational purposes only; it does not constitute investment advice or recommendations.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments