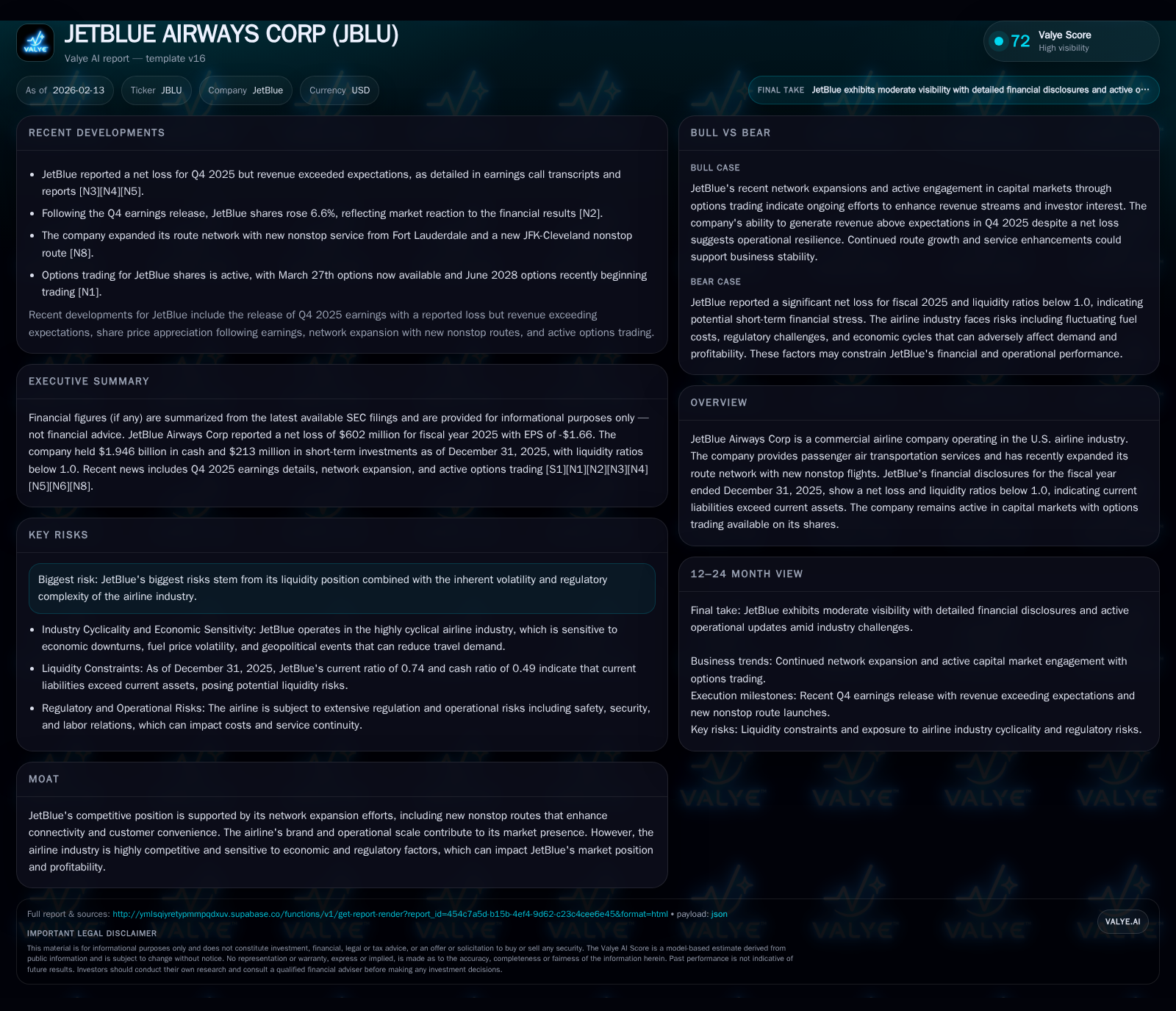

JetBlue’s Bold Route Expansion and Financial Strains Amidst Industry Headwinds

JetBlue pushes aggressive growth with new nonstop routes even as liquidity pressures highlight operational challenges.

JetBlue Airways embarked on a notable expansion of its route network into early 2026, launching nonstop services from Fort Lauderdale and JFK to Cleveland to deepen market penetration and enhance customer convenience. Despite revenue beats in Q4 2025, the company reported a substantial net loss, stressing the tension between growth ambitions and escalating cost structures. Liquidity metrics reveal current liabilities outpacing current assets, underscoring short-term financial strains in a volatile industry landscape. JetBlue’s strategic resilience will depend on balancing brand leverage and operational discipline amid regulatory complexities.

JetBlue's Expansion Drive: New Routes and Market Reach

Entering 2026, JetBlue Airways has demonstrated assertive momentum in broadening its route network, notably inaugurating nonstop flight services from Fort Lauderdale and between JFK and Cleveland [N12][N14]. These routes are emblematic of JetBlue's strategic intent to deepen its connectivity footprint within key U.S. hubs and secondary markets. The Fort Lauderdale addition taps into a vibrant leisure and business corridor in South Florida—traditionally dominated by legacy carriers—while the JFK-Cleveland link strengthens presence in the Northeast to Midwest trajectory.

This expansion is not merely an exercise in adding destinations; it underlines JetBlue's commitment to enhancing passenger convenience through nonstop options that reduce travel time and increase itinerary appeal. Such moves bolster JetBlue’s operational scale, an important competitive moat highlighted in the latest Valye News overview [valye_report_excerpt]. The incremental network breadth potentially improves asset utilization for existing fleets, optimizes gate usage at congested airports like JFK, and enriches the loyalty proposition by offering customers seamless alternatives.

However, expansion efforts also come with elevated capital deployment and operational complexity. Entering newer markets requires ramping up sales channels, negotiating airport slots, calibrating staffing needs, and adapting marketing strategies—all factors contributing to short- and medium-term cost increases.

Financial Snapshot: Navigating Losses Amidst Competitive Skies

Despite these growth ventures, JetBlue’s fiscal year ending December 31, 2025, closed with a material net loss of $602 million [F1]. This sizable deficit contrasts with concurrently reported revenue figures that managed to beat expectations during Q4 earnings [N4], presenting an intricate profitability puzzle.

Revenue improvement signals ongoing demand recovery post-pandemic disruptions with higher load factors on popular routes and enhanced ancillary revenues such as baggage fees or onboard sales. Yet, intensifying competition amid aggressive capacity expansions across the U.S. airline space exerts downward pressure on fares. Simultaneously rising operational costs further crush margins. Fuel price volatility remains one volatile expense line item, compounded by wage inflation as airlines compete for scarce pilots and cabin crew.

The disconnect between revenue gains and net losses may reflect structural inefficiencies or elevated fixed costs that do not scale proportionally with top-line growth. Additionally, impairment charges or extraordinary expenses tied to restructuring could weigh on bottom-line results; however, detailed disclosures are necessary for confirmation [S1].

Liquidity under Pressure: The Current Ratio and Its Implications

A critical financial data point underscoring JetBlue’s challenges is its current ratio of approximately 0.74 as of year-end 2025 [F1], signaling that current liabilities outstrip current assets by a significant margin. Such a ratio below 1 denotes limited short-term liquidity cushion.

Practically speaking, this means JetBlue might face tightness in meeting imminent obligations such as vendor payables, debt maturities due within one year, or operating expenses without relying on external financing sources or asset liquidations [S1]. It raises red flags about operational flexibility especially if unexpected cash outflows arise or if revenue generation slows unexpectedly.

The filing notes the company maintains $1.946 billion in cash and equivalents; however, given the $4.402 billion in current liabilities outstanding there is reliance on continuous capital market access or liquidity facilities to bridge gaps [F1]. This state poses risk in scenarios where credit conditions tighten or investor sentiment sours rapidly.

Revenue Beats but Losses Deepen: Earnings Highlights from Q4 2025

The Q4 earnings released in late January 2026 provide a nuanced performance narrative. Revenue beats relative to analyst estimates were acknowledged positively by investors resulting in a share price uptick shortly after the announcement [N3][N4][N1]. Nonetheless, the quarter also saw losses widen compared to previous periods—a sign that cost escalation outpaced revenue improvements [N10].

During the earnings call transcript highlights [N2], management emphasized several points: strong demand recovery underpinning higher ticket sales; fuel hedging programs moderating exposure; but also highlighted ongoing investments in customer experience enhancements adding short-term costs.

There was candid acknowledgement around margin pressure attributable to labor costs including pilot staffing plans aligned with expansion targets plus inflationary effects on maintenance contracts. Forward guidance was cautious without specific quantitative targets beyond reiterating focus on disciplined capacity management.

This duality—revenue growth paired with expanding losses—is indicative of an airline still trying to optimize its leverage between scaling operations profitably versus maintaining service levels demanded by a competitive market.

Operational Footprint: Cost Structure and Human Capital Insights

Insight from the 10-K provides granular detail on JetBlue's cost drivers beyond headline figures [S1]. Labor remains the largest expense category consuming a substantial portion of operating costs through wages for pilots, flight attendants, ground staff, and corporate employees; all segments heavily unionized fostering complex negotiation dynamics.

Fuel expenditures continue to be significant given airline exposure to commodity price swings combined with growing emphasis on sustainability initiatives that may require new technology investment or fleet upgrades. Maintenance costs align closely with fleet age profile—JetBlue operates a mix of newer Airbus A320 family jets alongside regional jets requiring variable upkeep cycles.

Human capital management strategies emphasize training programs for skill retention amid industry-wide talent shortages plus diversity efforts aimed at employee inclusion enhancing organizational culture robustness.

Regulatory compliance expenses also factor heavily—ranging from safety audits to environmental standards adherence—which while mandatory increase fixed overheads irrespective of passenger volumes.

Collectively these elements shape an elevated cost base demanding stringent operational discipline amid expansion phases.

Risk Landscape: Regulatory Complexity and Industry Volatility

JetBlue faces several intertwined risks rooted in sector-specific regulatory frameworks along with macroeconomic headwinds documented extensively in filings [S1] and the Valye report excerpt. Regulatory layers encompass FAA oversight for safety compliance; TSA mandates influencing security protocols impacting scheduling; environmental regulations introducing carbon emissions controls possibly requiring offsets or fleet renewals.

Simultaneously economic cycles exert influence via fuel pricing shocks triggered by geopolitical tensions or supply disruptions; fluctuating consumer confidence affecting discretionary travel budgets; interest rate environments shifting debt servicing burdens; plus labor market tightness creating wage inflation traps.

Liquidity weakness compounds vulnerability here—should unexpected policy changes elevate capital demands or trigger fines JetBlue would be less cushioned than financially healthier peers. Combined industry cyclicality means sudden downturns can sharply degrade cash flow causing forced capacity cuts or restructuring which erode customer trust and brand equity further [valye_report_excerpt][S1].

Options Activity and Market Sentiment: What Traders Are Saying

Post-Q4 earnings release saw marked options-market vibrancy around JetBlue shares with new March expiration contracts becoming available signalling trader anticipation of elevated share price movement or strategic developments [N8]. Correspondingly shares climbed approximately 6.6% following earnings dissemination underscoring positive albeit tempered investor reaction amidst mixed fundamentals [N1].

Volume analytics from broader transportation ETFs including JetBlue components reflected unusual trading activity consistent with heightened speculative positioning near earnings season endings [N9]. This confluence suggests market participants are girding either for volatility swings driven by operational updates or potential corporate maneuvers (e.g., fleet adjustments or alliance partnerships).

Importantly these sentiments must be parsed alongside fundamental realities—the options surge does not revise underlying financial fragilities but instead signals opportunity taking behaviors under uncertainty.

Strategic Outlook: Can JetBlue Leverage Its Brand to Sustain Growth?

Weaving together internal disclosures with recent market developments paints a picture of an airline ambitiously pursuing growth yet constrained by financial fragility [valye_report_excerpt][S1][N12]. The fresh nonstop routes exemplify attempts at bolstering competitive moats through geographically targeted connectivity augmentations enhancing customer value propositions.

Nonetheless balancing expansion with profitability remains an unresolved equation given persistent net losses coupled with restrictive liquidity metrics undermining operating flexibility amidst external risks. Management rhetoric conveys awareness of this tightrope requesting investor patience as investments mature toward realized returns.

Longer term viability will hinge upon whether incremental revenues generated by network extensions can scale faster than associated incremental costs—particularly under ongoing external pressures from regulation and macroeconomic volatility. Should JetBlue succeed in stabilizing cost bases through efficiency measures while capitalizing on brand appeal present notably in dense domestic corridors it can create positive feedback loops improving cash flows gradually.

However absence of meaningful improvement could force retrenchments curtailing growth aspirations damaging franchise momentum irreversibly.

In sum JetBlue sits at a poignant strategic inflection point negotiating tradeoffs between ambition-driven expansion strategies tempered pragmatically by necessary financial stewardship within an unforgiving industry environment.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments