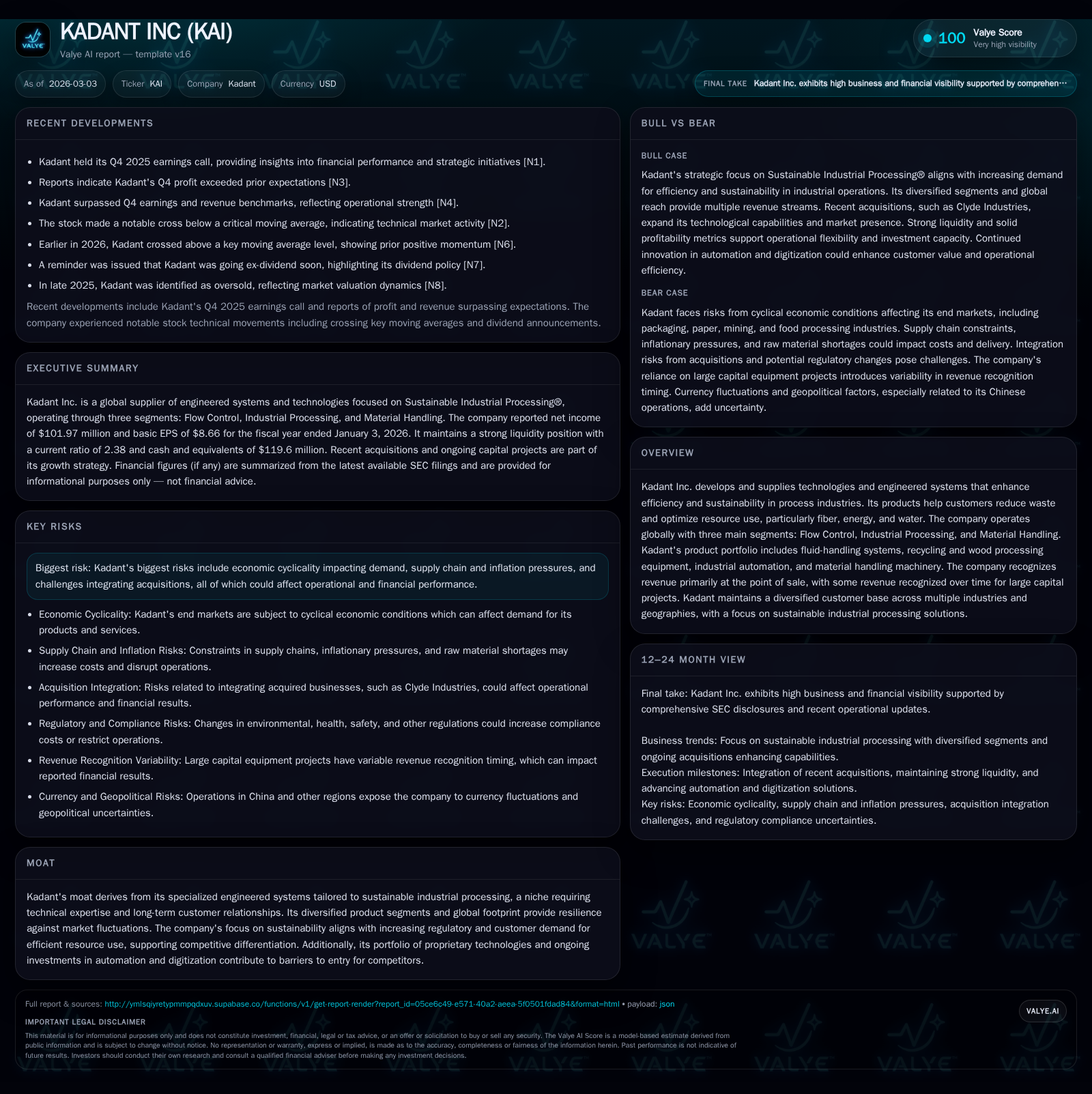

Kadant Inc. Elevates Sustainable Industrial Processing Amid Mixed Profit Trends

Robust revenue stability contrasts with profit margin contractions as Kadant advances its niche in sustainability-driven industrial technologies.

Kadant Inc. demonstrated steady revenue around $271 million per quarter during fiscal 2025, underpinning its position in engineered solutions for sustainable industrial processing. Despite this revenue resilience, operating and net incomes declined about 8% YoY, reflecting margin pressures likely stemming from inflationary costs, product mix shifts, and integration expenses. The three core segments—Flow Control, Industrial Processing, and Material Handling—displayed varied profitability profiles, with Flow Control delivering the highest margins. Large capital equipment projects recognized over time introduce revenue timing volatility that complicates quarter-to-quarter comparisons. Kadant’s disciplined capital allocation sustains dividend growth and manages leverage prudently, supporting an approximate 10% ROE and sizable free cash flow generation. Going forward, sustainability demand and automation investments could fuel growth, though economic cyclicality, supply chain constraints, and acquisition integrations warrant close monitoring.

Steady Revenue Base Meets Profit Margins Challenge: The Recent Past

Kadant Inc.'s fiscal 2025 showcased resilience in revenue generation despite operating headwinds that compressed profits. Quarterly revenue hovered near $271.6 million for Q3 2025, essentially flat versus the year prior period [F1][S2]. However, operating income declined by approximately 8%, falling to $53.7 million for the quarter from $59 million a year earlier [F1][S10], signaling challenges in managing cost inflation and segment mix changes.

Net income followed the same downward trajectory at -8.6% YoY for FY2025 compared to FY2024 ($101.97 million vs $111.6 million) [F1]. Such profit compression hints at margin pressures due to increased selling, general & administrative expenses as well as higher amortization charges linked to recent acquisitions.

This dichotomy between a stable top line and shrinking bottom line suggests operational leverage is uneven across business units and cost dynamics require prudent management going forward.

Historical performance (annual)

| FY | Net ($mm) | CFO ($mm) | OpInc ($mm) | Capex ($mm) | Net YoY |

|---|---|---|---|---|---|

| 2025 | 102 | 171 | 157 | 17 | -8.6% |

| 2024 | 112 | 155 | 171 | 21 | -3.9% |

| 2023 | 116 | 166 | 166 | 32 | -4.0% |

| 2022 | 121 | 103 | 171 | 28 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | Div ($mm) | FCF ($mm) | ROE% |

|---|---|---|---|

| 2025 | 16 | 154 | 10.4 |

| 2024 | 15 | 134 | 13.2 |

| 2023 | 13 | 134 | 15.0 |

| 2022 | 12 | 74 | 18.5 |

Source: SEC companyfacts cache [F1].

Note: Revenue reflects sums of quarterly data scaled; percentages approximate given reported quarterly figures [F1]

Breaking Down Segment-Level Performance: Flow Control, Industrial Processing, Material Handling

Kadant's three segments reveal differentiated profit dynamics that collectively shape overall performance:

Flow Control: This segment leads with the highest gross profit margin of roughly 51.9% in Q3 2025 and operating margins near 23.6%, highlighting efficiency in fluid-handling products like rotary sealing devices critical for packaging, tissue, and energy sectors [S10]. Margins here remained resilient despite slight revenue dip fluctuating around $95 million. The specialized nature of these products confers pricing power amid inflationary environments.

Industrial Processing: Encompassing fiber recovery systems and wood processing machinery including recently acquired boiler cleaning tech from Clyde Industries, this largest segment saw revenues around $106 million but exhibited a more moderate operating income margin near 17.7%, down from prior year margins of about 23%. Inventory absorption costs and integration expenses partially depress profitability [S10][S29].

Material Handling: Focused on conveyors and balers for mining and aggregates sectors posted lowest margins — gross around 38.5%, operating near 17.8% — yet contributes meaningful diversification to Kadant’s portfolio [S10]. This unit's exposure to commodity markets subjects it to greater cyclicality.

The variance in segment-level operating income margins illustrates how product mix nuances increasingly impact consolidated profits amid rising input prices.

Capital Project Revenue Recognition: Impact on Financial Results

Revenue recognition methodology plays a pivotal role in financial periodicity owing to Kadant’s customized large capital equipment projects typically accounted via 'over-time' recognition using input methods related to incurred costs against total expected project costs [S4].

In Q3 2025 these 'over-time' revenues declined materially to about $17 million from nearly $33 million a year earlier while point-in-time revenues (standard product sales) grew modestly to approximately $254 million [S4]. This shift can create timing volatility between quarters especially when long-cycle projects start or complete unevenly.

Such nuances require investors to interpret short-term earnings cautiously since backlog conversion does not always align neatly within fiscal reporting windows.

Growth Drivers Underpinning Kadant’s Market Position

Historical growth has been propelled by several factors:

- Expanding international footprint notably across Europe where revenues increased modestly from $57 million to nearly $66 million quarterly reflecting strategic geographical diversification beyond North American core [S9].

- Acquisition integration boosting capabilities especially with industrial boiler efficiency technologies via Clyde Industries acquisition ($175 million cash payment October '25) expanding relevance in energy optimization markets globally [S29][N1].

- Sustained investment in automation and digitization within process industries aligns well with increasing customer emphasis on sustainability metrics; Kadant’s solutions reduce fiber waste and optimize water/energy use—a strong tailwind given tightening environmental regulations globally [S1].[N1]

Increasing customer demand for sustainable processing solutions underpins organic growth prospects even as macroeconomic cycles challenge volume expansions.

Industry Headwinds and Operating Constraints: What Limits Future Expansion?

While optimism abounds on sustainability adoption benefits, several constraints temper outlook:

- Economic cyclicality dampens capital spending intensity especially in cyclical end-markets like mining or packaging converting sectors impacting order visibility [S7][N1].

- Persistent inflation pressures on raw materials raise COGS challenging margin preservation.

- Complexity integrating multiple acquisitions adds organizational complexity risking execution delays or cultural clashes marginally impacting operational efficiencies.

- Supply chain bottlenecks have moderated but remain a watch area given global geopolitical tensions.

These intrinsic industry risks necessitate vigilant operational adaptations to sustain EBITDA margins amid growth aspirations.

Financial Forecasts and Key Indicators to Monitor Ahead

Recent Q4 earnings commentary highlighted Kadant’s shift toward adjusted EPS calculation methodology moving forward improving comparability but absent formal long-term guidance from management remains reliant on key leading indicators such as backlog levels, contract liabilities trends (~$60 million at FY end up from ~$46 million year prior), and margin targets discussed during analyst calls [N1][N2][S4].

Backlog conversion rates particularly on large capital projects may presage future revenue acceleration or contraction pending macro conditions.

Capital Allocation Strategy: Balancing Dividends, Buybacks, and Investment

Kadant exercises disciplined capital deployment balancing shareholder returns with reinvestment needs:

- Operating cash flow increased ~10% YoY reaching $171 million for FY2025 while capex reduced by nearly one-fifth reflecting efficiency gains or matured asset base needs [F1][S16].

- Dividends paid rose modestly to ~$15.8 million demonstrating commitment to steady shareholder distributions alongside manageable levels of share repurchases historically minor or paused recently due to strategic priorities [F1][S27].

- Debt profile well managed with revolver capacity expanded significantly to $750 million amid debt maturity extension enhances financial flexibility supporting growth investments including acquisitions like Clyde Industries [$175M cash outlay covered by revolver usage] without pressuring leverage ratios beyond covenant limits (~3.75x leverage max allowed) [S5][S6][F1].

- ROE estimated around solid double digits at ~10.4%, indicative of effective equity utilization relative to reported net income despite margin headwinds [F1].

Overall capital strategy seeks balance between sustaining innovation funding while returning cash efficiently.

Risks and Regulatory Considerations in Kadant’s Operating Environment

Key risks detailed include economic sensitivity of order intake cycles common within capital goods industries; inflationary cost exposures; reliance on stable supply chains; legal contingencies related to contractual disputes typical for engineered systems providers; all embedded within detailed risk disclosures [S7][N1].

Regulatory frameworks increasingly emphasize sustainable manufacturing outputs which simultaneously represent opportunity yet intensify compliance requirements contributing potential cost burdens or product adaptation demands.

Technological Edge and Sustainability as Moats in Competitive Landscape

Kadant leverages proprietary technology platforms such as rotary sealing devices crucial for fluid flow control along with advanced fiber recovery mechanical systems as barriers preventing facile competitive entry given high technical specialization required [S8].

Coupling this technological positioning with investment into automation/digitization modules tailored for industrial processing enhances customer stickiness via integrated solution offerings aligned tightly with evolving ESG norms worldwide.

Such combined assets reinforce durable moats centered on sustainable industrial processing leadership fostering long-term competitive advantage while addressing pressing global resource efficiency imperatives.

Disclaimer: This analysis is intended solely for informational purposes based on data current as of March 2026 from verified filings and news reports; it does not constitute investment advice or recommendations.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments