Karbon Capital Partners' Q1 Shifts Spotlight On SPAC Value Creation Challenges

Karbon Capital Partners’ first quarterly update post-IPO underscores the operational status quo and execution-critical path toward its initial business combination.

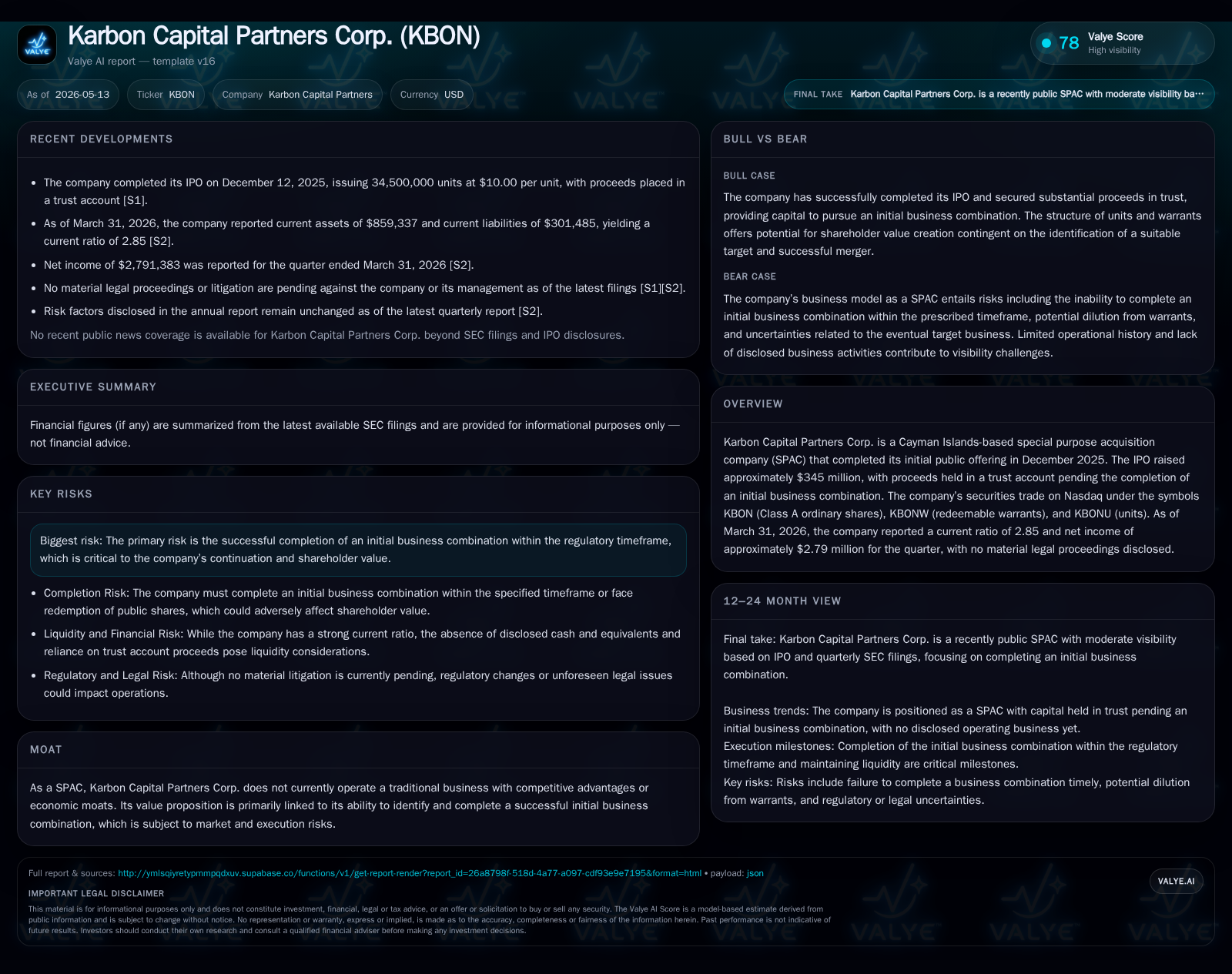

Karbon Capital Partners Corp. reported its inaugural quarterly filing since completing a $345 million IPO in December 2025, reflecting typical SPAC operational dynamics with no target acquisition yet announced. The 10-Q released on May 12, 2026 highlights a stable financial footing with a healthy current ratio and modest net income attributable to trust-related accounting, while risk factors and legal proceedings remain unchanged. As a SPAC, the company’s value hinges entirely on successful deal sourcing and completion within regulatory timelines, facing competitive pressures in the booming de-SPAC market.

Latest Quarterly Operating Update: Progress and Implications

Karbon Capital Partners Corp. provided its first substantive quarterly operating update with the Form 10-Q filed on May 12, 2026 [S2]. Having completed its initial public offering in December 2025 with gross proceeds of approximately $345 million held in a trust account, the company remains without an announced business combination target. The filing reiterates that no material legal proceedings or changes in risk factors have occurred since the annual Form 10-K submission on March 26, 2026 [S1][S10].

Despite lacking operating revenues—as expected for a Special Purpose Acquisition Company (SPAC)—the reported net income of around $2.79 million for the quarter presumably reflects accounting nuances related to interest earned on trust assets and non-operational items rather than underlying business profits [F1]. This net income figure is typical for pre-combination SPACs and is not indicative of recurring earnings.

Overall, this update confirms the classic SPAC status quo: capital securely parked awaiting deployment into an initial business combination while maintaining compliance with regulatory disclosure obligations.

Understanding Karbon’s SPAC Business Model: Structure, Mechanics, and Market Offering

Karbon’s business model centers entirely on raising capital through its December 2025 IPO [S4][S5]. The offering consisted of units priced at $10 apiece—each unit bundling one Class A ordinary share (KBON) and one-quarter of a redeemable warrant (KBONW), exercisable at $11.50 per share subject to adjustment [S6][S7]. Units (KBONU) have subsequently become separable starting January 27, 2026 allowing independent trading of shares and warrants [S11].

This structure aligns with typical SPAC design where proceeds are placed in a restricted trust account pending an initial business combination typically to be consummated within two years post-IPO. Sponsor private placement units totaling $8.9 million represent aligned management skin-in-the-game although these shares lack redemption rights available to public shareholders [S19][S22].

Value creation depends principally on identifying an attractive acquisition target swiftly and executing the de-SPAC transaction at or above trust-account per-share value—offset by transaction costs and shareholder redemptions. Investor considerations include warrant dilution potential post-exercise and timing risks under SEC-mandated deadlines.

Industry Context: Competitive Dynamics of the SPAC Ecosystem

Karbon participates in an increasingly crowded SPAC ecosystem featuring fierce competition for high-quality private companies to bring public via reverse mergers [S1][S12]. The challenge of sourcing deals is compounded by relatively standardized unit economics limiting pricing power; sponsors compete primarily through reputation and transactional capabilities.

SPACs confront strict regulatory timelines requiring deal completion within roughly two years from IPO closure or face forced liquidations with return of funds minus expenses to shareholders. This creates considerable execution pressure alongside redemption risk if shareholders opt out at vote time.

Deal origination costs including underwriter fees (Citigroup serves as lead underwriter here), advisors, legal counsel, and diligence expenses weigh heavily against realized returns. Furthermore, secondary market valuation discounts reflecting uncertain pipelines further strain sponsor incentives.

Growth Prospects: Strategic Drivers for Successful Business Combination Execution

Growth for Karbon is non-traditional; it is predicated entirely on successfully closing an initial business combination that transitions it from a shell vehicle into an operating public company [S1]. Announced merger agreements often expand investor interest base through enhanced liquidity and broader market access.

Absent organic revenue streams until combination consummation, management experience in identifying compelling private targets becomes paramount alongside efficient execution amidst shifting market conditions. Post-deal benefits materially hinge on acquirer sector focus—currently undisclosed but determinant for post-merger positioning.

If executed well, successful de-SPAC transactions can deliver shareholder value substantially exceeding the trust account floor through strategic synergies and growth acceleration driven by access to public capital markets.

Risks and Constraints: Timelines, Regulatory Hurdles, and Market Conditions

Primary risk vectors remain unaltered according to latest filings: failure to consummate an initial business combination within required windows could compel liquidation wrenching shareholder outcomes [S1][S2][S12]. This deadline-driven nature creates binary operational outcomes.

Potential dilution emerges from warrants exercisable at $11.50—a price point above IPO level but potentially below future merger prices—imposing caps on sponsor upside while pressuring eventual share issuance volumes. Volatile equity markets complicate valuation consensus further increasing risk premiums demanded by investors.

Competition intensifies sourcing quality targets amidst similarly structured peers striving to differentiate in sponsor expertise or sector specialization. Redemption rates pose additional uncertainty where large-scale opt-outs can reduce available merger funding thwarting planned transactions.

What Investors Should Monitor Next: Upcoming Milestones and Operational Signals

Key upcoming indicators include announcements or filings revealing letter(s) of intent or definitive agreements for identified acquisition targets [S2][S11]. Shareholder voting dates on proposed business combinations will serve as critical near-term event markers reflecting investor sentiment.

SEC comment letter resolutions may also provide transparency around any regulatory concerns impacting deal timelines or structures if such filings occur subsequently. Operational signals such as appointment of new directors representing prospective merger interests may emerge as well.

Market reception to announced deals generally dictates share price reaction trajectories defining post-combination liquidity profiles thus closely watched by investors awaiting clarity from current standby status.

Current Financial Health: Liquidity, Capital Deployment, and Financial Position

Latest financial snapshot

| Metric | Value | Period |

|---|---|---|

| Current assets | $859337 | |

| 2026-03-31 | ||

| Current liabilities | $301485 | |

| 2026-03-31 | ||

| Current ratio | 2.85x | |

| 2026-03-31 |

Source: SEC companyfacts cache [F1].

Karbon maintains a liquid balance sheet consistent with its SPAC mandate; as of March 31, 2026 current assets totaled $859,337 against current liabilities of $301,485 yielding a conservative current ratio of approximately 2.85 [F1]. These figures exclude the sizable approximately $345 million trust account proceeds held off balance sheet under trustee control ensuring preservation for eventual combination or redemption events.

The modest net income reported relates largely to accrued interest earned on the trust assets less operating expenses rather than core profitability [F1]. No debt or leverage is reported nor expected given reliance on equity capital until transaction completion stages.

Liquidity metrics affirm sufficient working capital support for ongoing administrative costs including audit fees, legal expenses associated with deal diligence preparation, listing fees for securities trading on Nasdaq under KBON/KBONW/KBONU symbols.[F1]

| Metric | Value |

|---|---|

| Current Assets | $859,337 |

| Current Liabilities | $301,485 |

| Current Ratio | 2.85 |

This analysis provides context around Karbon Capital Partners Corp.'s early lifecycle as a newly listed SPAC navigating typical challenges inherent in bringing private companies public through reverse mergers. Investors should view financial data primarily as indicative of administrative stewardship rather than conventional operational results given the pre-combination stage status.

Disclaimer: This document is an analytical overview intended for informational purposes only; it does not constitute investment advice or recommendations regarding securities of Karbon Capital Partners Corp.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments