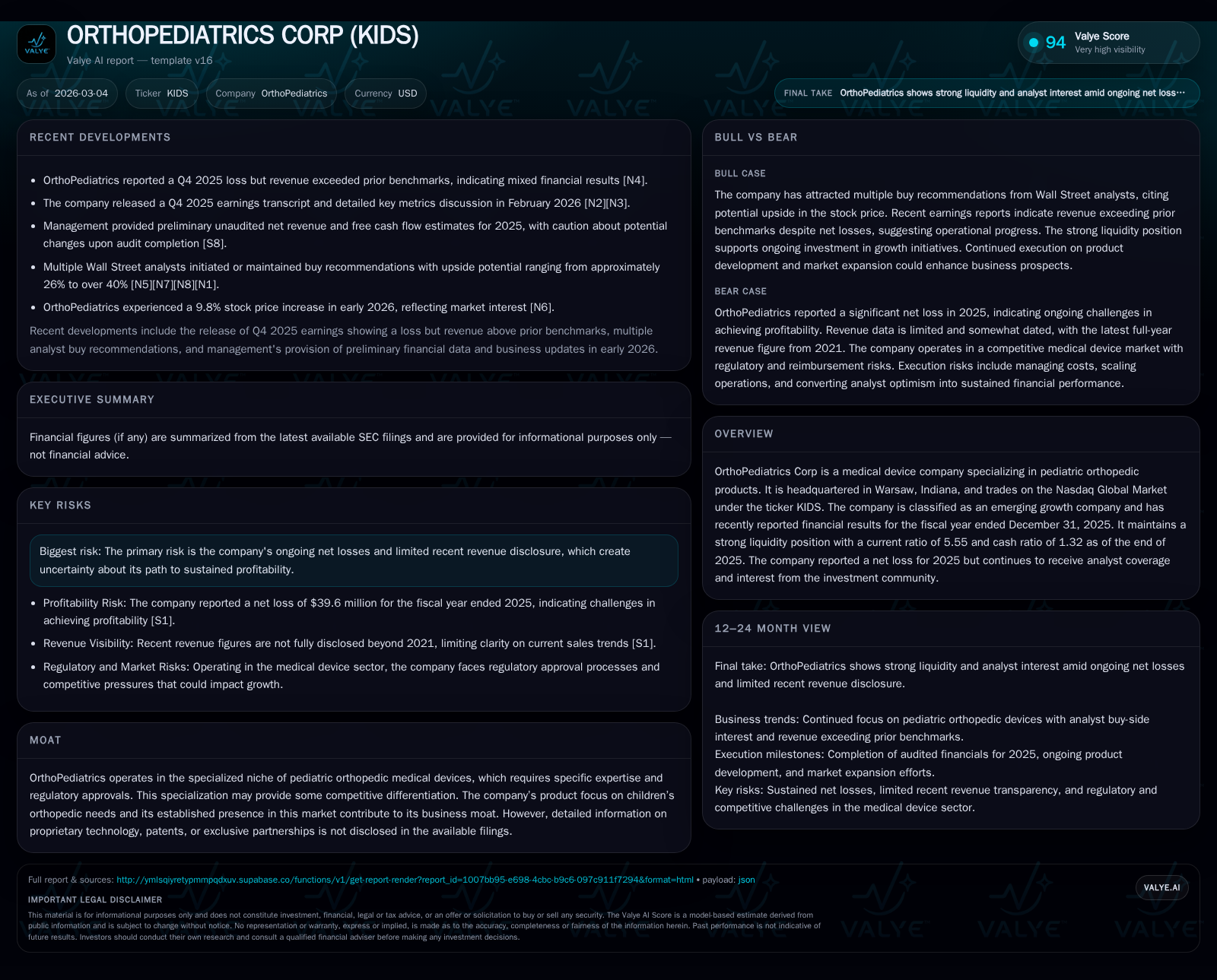

OrthoPediatrics Corp Extends Pediatric Orthopedic Market Focus Despite Ongoing Losses

Specialization in pediatric orthopedic devices supports growth, but profitability challenges persist amid growing operating expenses.

OrthoPediatrics Corp operates as a niche specialist in pediatric orthopedic medical devices, expanding geographically and through acquisitions since its founding. From 2018 through 2021, the company saw strong revenue growth driven by product portfolio expansion and market penetration. However, despite increasing sales activity, OrthoPediatrics has continued to report operating losses through 2025, with escalating R&D and capacity investments weighing on profitability. The company maintains a solid liquidity position, supporting ongoing growth efforts and R&D initiatives. Future revenue growth depends on leveraging recent international expansions and integrating acquired technologies, while margin improvement and path to profitability remain key watch points.

Company Background and Market Niche

OrthoPediatrics Corp (Nasdaq: KIDS), headquartered in Warsaw, Indiana, is focused exclusively on designing pediatric-specific orthopedic implants, surgical instruments, and specialized bracing systems tailored for children. Since commencing U.S. sales in 2008, the firm broadened its footprint internationally beginning in 2011, establishing subsidiaries or agencies across key regions such as the UK, Australia/New Zealand, Canada, major European markets (Netherlands, Germany), and recently Brazil [S1].

The company's specialized approach addresses a distinct market need; pediatric orthopedics requires different anatomical sizing and biomechanical considerations compared to adult orthopedics. This specialization offers a moat rooted in expertise and regulatory compliance specific to children’s devices but lacks disclosed proprietary technological advantages or exclusive licensing partnerships.

Historical Financial Performance

From a financial perspective, OrthoPediatrics demonstrated robust revenue growth over the last several years through increased unit sales and expanded geographic presence. Revenue rose from $57.6 million in 2018 to nearly $98 million by the end of 2021 — a compound annual increase supporting steady market penetration [F1].

However, operating profitability has remained elusive as the company prioritizes spending on R&D for new products and infrastructure investments to support international operations. Operating income declined further into negative territory from -$25.4 million in 2022 to -$39.2 million by fiscal 2025 [F1], illustrating widening losses coincident with growth-related expenditures.

Net income patterns align closely with operating results; notable was a modest positive net income of $1.25 million in 2022 likely due to non-operating factors but followed by sharp net losses totaling -$39.6 million in 2025 [F1]. Operating cash flows have also remained negative consistently from at least 2022 through 2025 (-$4.9 million CFO in latest year), constrained further by substantial capital expenditures (~$11.1 million capex in 2025) directed towards scaling manufacturing capabilities and facilities [F1].

Historical performance (annual)

| FY | Net ($mm) | CFO ($mm) | OpInc ($mm) | Capex ($mm) | Net YoY |

|---|---|---|---|---|---|

| 2025 | -40 | -5 | -39 | 11 | -4.8% |

| 2024 | -38 | -27 | -35 | 14 | -80.3% |

| 2023 | -21 | -27 | -27 | 17 | -1767.2% |

| 2022 | 1 | -22 | -25 | 10 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | FCF ($mm) | ROE% |

|---|---|---|

| 2025 | -16 | -11.4 |

| 2024 | -41 | -10.7 |

| 2023 | -44 | -5.6 |

| 2022 | -32 | 0.3 |

Source: SEC companyfacts cache [F1].

*Full-year data available only for operating metrics post-2021 [F1]

Growth Drivers and Future Prospects

OrthoPediatrics' future top-line expansion hinges primarily on:

Geographic Expansion: The company has deepened its presence internationally by setting up distribution entities and warehouses across Europe (Netherlands, Germany), Australia/New Zealand, and launched direct sales in Brazil by late 2025 [S1][S3]. Improved local infrastructure should facilitate faster delivery times and enhanced customer service.

Portfolio Enhancement via Acquisitions: Strategic acquisitions such as ApiFix Ltd., which offers minimally invasive scoliosis correction systems for adolescents, alongside MD Ortho (clubfoot orthopedics), augment both breadth and depth of device offerings targeting pediatric deformity correction — a high-impact sub-niche within pediatric orthopedics [S1]. These provide cross-selling opportunities.

Organic Product Innovation: Continued R&D investment focuses on refining existing products like PediLoc®, PediNail™, Boston Brace®, alongside newer innovations addressing complex pediatric conditions requiring tailored solutions [S11][S12]. The contract manufacturing model supports scalability.

Potential constraints include ongoing pandemic-related headwinds disrupting elective surgeries—critical use cases for OrthoPediatrics devices—as well as broader economic uncertainties affecting healthcare spending patterns [S1]. These exposures introduce variability to procedural volumes impacting near-term revenue consistency.

Outlook and Management Guidance

Management expresses cautious optimism regarding accelerating revenue growth through enhanced international operations combined with acquisition synergies; however, explicit profitability milestones remain unspecified publicly [N1][S12]. The company projects achieving break-even cash flow at some point during expansion though integration costs may delay this event.

Analyst upgrades indicate investor interest based on anticipated topline acceleration driven by recent strategic moves despite persistent loss risks noted among sector peers specializing in smaller-device niches [N4][N5][N6].

Capital Allocation & Returns Analysis

OrthoPediatrics retains earnings for reinvestment into growth; no dividends have been declared recently following discontinuation after small payouts in prior years [F1]. Stock repurchases are negligible reflecting disciplined capital management amid loss absorption needs.

Return metrics show negative returns on equity approximating -11% for the latest fiscal year given persistent net deficits amid an equity base near $347 million at end-2025 supported by prior equity raises [F1]. Free cash flow remains negative reflecting ongoing scale build-out.

The balance sheet exhibits strength with a current ratio of approximately 5.55 alongside cash reserves around $19.6 million providing operational flexibility despite negative earnings phases [F1][S5][S7]. This positions OrthoPediatrics favorably versus peers dependent on leverage-constrained financing.

Risks & Challenges

Key risks include:

- Dependence on elective pediatric surgeries vulnerable to disruption from pandemic surges or hospital capacity strains (notably COVID-19/RSV impact continues to create uncertainty) [S1].

- Extended timeline toward profitable scale requiring sustained capital infusions or operational improvements.

- Competitive pressures where innovation pace is critical but entry barriers moderate due to contract manufacturing enabling substitutes.

- Macro headwinds such as inflationary cost increases potentially elevating operating expenses temporarily [S1].

Conclusion

OrthoPediatrics maintains focus on a unique pediatric orthopedic niche supported by steady historical revenue gains but weighed down by continuing operating losses reflective of its investment-intensive growth phase. Expansion into key international markets alongside technology acquisitions diversifies product scope offering potential upside.

Monitoring should center on quarterly revenue trends relative to management projections alongside progress toward break-even cash flow while assessing competitive differentiation sustainability amid evolving healthcare delivery models.

Disclaimer: This analysis is based exclusively on publicly available SEC filings and recent news reports up to March 2026 concerning OrthoPediatrics Corp (KIDS). All financial figures adhere strictly to sourced data without speculative extrapolation or investment recommendations.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments