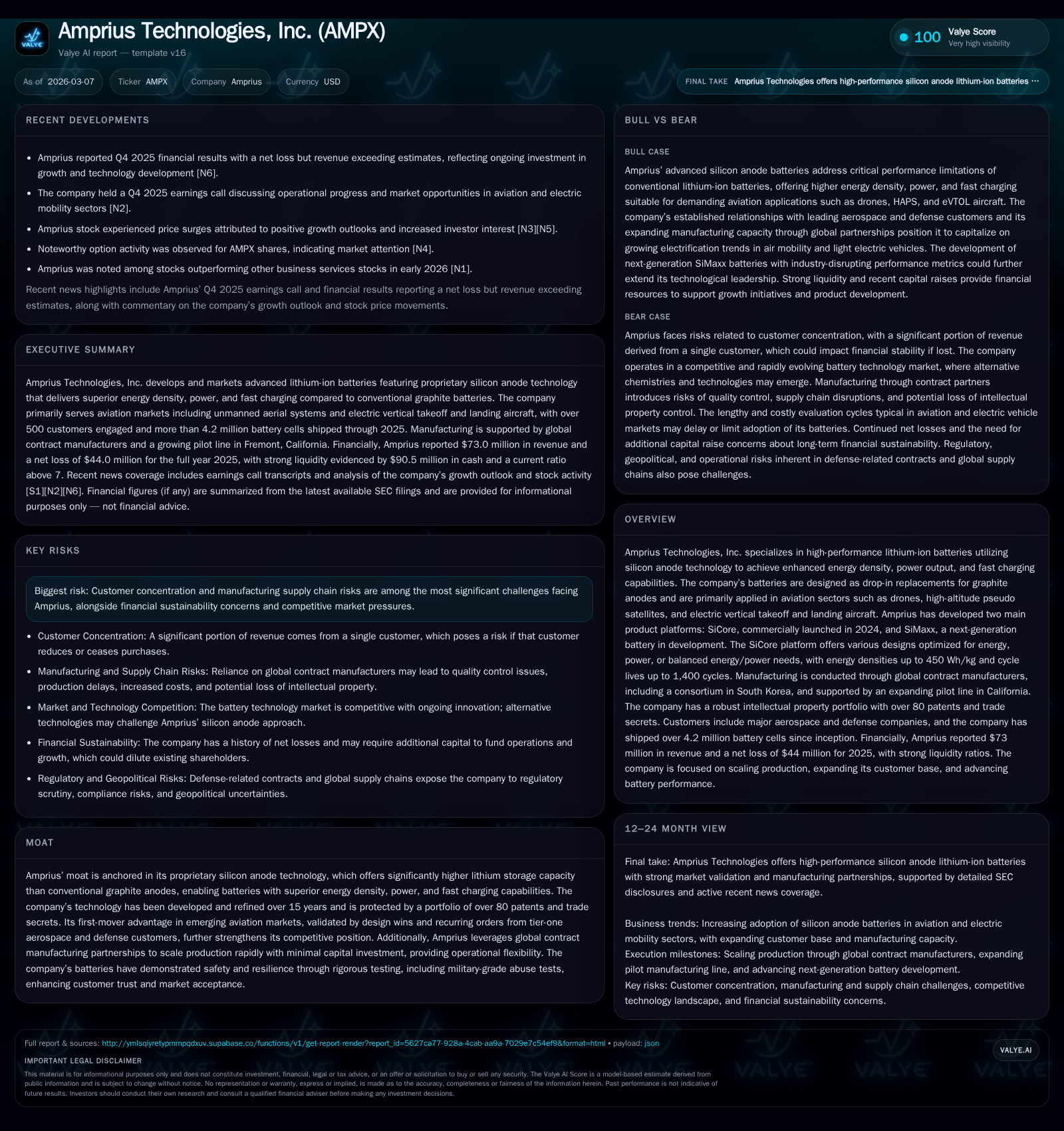

Amprius Technologies Battles Profitability Challenges While Scaling Next-Gen Lithium Batteries

The company’s rapid revenue growth driven by proprietary silicon anode technology contrasts with persistent operating losses amid manufacturing scale-up.

Amprius Technologies, a pioneer in silicon anode lithium-ion batteries for aviation and mobility, demonstrated exceptional revenue growth of over 200% in fiscal 2025 following the commercial launch of its SiCore platform. Despite top-line gains, profitability remains elusive with operating losses near $46 million due to rising costs and scale-up investments. The firm's competitive edge stems from extensive patent protection and validated applications in drone and eVTOL sectors, supported by global contract manufacturing partnerships. Expansion initiatives focus on ramping a Fremont pilot line with government contracts backing progress, but supply chain dependencies and market concentration pose notable risks. Monitoring operational milestones and cash burn will be crucial as Amprius pursues further innovation with its SiMaxx platform.

Surging Revenues Fuelled by Silicon Anode Breakthroughs

Amprius Technologies recorded an impressive revenue jump to $73.0 million in fiscal year 2025, representing a remarkable 202% increase from $24.2 million in 2024 [F1]. This acceleration followed the commercial launch of its flagship SiCore battery platform in early 2024 [S1]. SiCore batteries utilize proprietary silicon anode technology that replaces conventional graphite anodes directly — enabling significantly higher energy densities reaching up to 450 Wh/kg, superior power output, and rapid charge capabilities that distinguish these cells in demanding aviation applications [S1].

This leap in sales reflects growing validations from over 500 customers since inception and shipments exceeding 4.2 million battery cells used primarily in unmanned aerial systems (UAS), high-altitude pseudo satellites (HAPS), and electric vertical takeoff and landing (eVTOL) aircraft sectors [S1]. The diverse product designs under SiCore cater specifically to energy-intensive or high-power needs, supporting mission-critical use cases across aerospace OEMs like Airbus subsidiaries, AeroVironment, BAE Systems, Teledyne FLIR, and defense customers including the U.S. Army [S20].

Technology Moat Rooted in Innovation and Patent Defense

Amprius’ competitive moat hinges on its fifteen years of dedicated research culminating in over 80 granted or pending patents globally protecting its advanced silicon anode architectures and manufacturing know-how [S19]. Key differentiators extend beyond raw energy density: their silicon structures—characterized by nanowire templates and multilayered dopants—enable operational voltages about 100 mV higher than graphite counterparts, which not only facilitate fast charge cycles but also improve safety margins at lower operating temperatures [S19][S20].

The technology's drop-in compatibility allows seamless integration into existing lithium-ion battery manufacturing processes without drastic supply chain overhaul — an advantage against alternative silicon composite or lithium metal solutions that are less mature or commercially proven [S9][S17]. Rigorous third-party military-grade abuse testing validated resilience under nail penetration tests per MIL-PRF-32383 standards without ignition, underscoring readiness in harsh environments [S20].

Manufacturing Footprint and Scale-Up Progress

Production scaling relies heavily on strategic global contract manufacturing partnerships rather than capital-intensive facility build-outs [S11]. These include a South Korean consortium known as the “Amprius Korea Battery Alliance” providing capabilities across pouch, cylindrical, and prismatic cell formats with annual production capacity exceeding 2 GWh as of December 2025 [S1][S21]. This outsourced model offers flexibility to ramp volumes while controlling fixed capital commitments.

Domestically, Amprius operates a Fremont pilot line where it manufactures next-generation SiMaxx batteries [S1]. The company is actively expanding this pilot facility’s capacity from kWh to a targeted 10 MWh scale intended for accelerated prototype production of SiCore customers requiring rapid iteration [S21]. This expansion is partly funded by a $14.8 million contract through the U.S. Defense Innovation Unit awarded mid-2025 [S21]. However, the prior lease agreement for a large-scale Colorado facility was terminated due to evolving supply dynamics favoring contract manufacturers abroad [S21].

Financial Performance: Rising Sales Amid Loss-Making Operations

Despite robust revenue gains, Amprius reported operating income losses at $46.6 million for FY2025 barely changed from $(46.3) million in FY2024 — reflecting stable but substantial operating deficits amid scaling efforts [F1][N2]. Net loss stood around $44 million with slight improvement relative to prior years' widening deficits [F1]. Gross margin pressures stem from ongoing ramp costs, complex manufacturing quality control protocols necessary for novel silicon structures, and early stage volume inefficiencies.

Operating cash flow remained negative at approximately $(31.1) million but showed modest improvement versus $(33.3) million last year indicating controlled outflows during expansion [F1]. Capital expenditures increased moderately to $4.4 million consistent with pilot line enhancements but remain restrained compared to earlier years emphasizing reliance on contract manufacturing rather than greenfield builds [F1].

Historical performance (annual)

| FY | Rev ($mm) | Net ($mm) | CFO ($mm) | OpInc ($mm) | Rev YoY | Net YoY |

|---|---|---|---|---|---|---|

| 2025 | 73 | -44 | -31 | -47 | +202.1% | +1.4% |

| 2024 | 24 | -45 | -33 | -46 | +167.0% | -21.5% |

| 2023 | 9 | -37 | -26 | -39 | +105.3% | -112.2% |

| 2022 | 4 | -17 | -14 | -18 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | FCF ($mm) | ROE% |

|---|---|---|

| 2025 | -36 | -42.4 |

| 2024 | -37 | -64.3 |

| 2023 | -43 | -61.5 |

| 2022 | -15 | -23.7 |

Source: SEC companyfacts cache [F1].

Note: All figures approximate from reported data.

Capital Investment, Cash Flows, and Capital Structure Insights

At year-end 2025 Amprius held cash and equivalents totaling roughly $90 million with current assets exceeding liabilities sevenfold—a current ratio above 7 indicating solid short-term liquidity [F1]. Nonetheless, substantial negative free cash flow around $(35.5) million after accounting for capex persists as operational expansion continues absorbing capital [F1].

Equity grew notably to approximately $104 million fueled by financing rounds since going public via SPAC merger in late 2022 facilitating scale-up spending [F1][S21]. Capital discipline manifests through measured capex focused on modular pilot line upgrades complemented by outsourcing bulk production capacity through partners reduces balance sheet leverage risks.

Given losses and cash burn rates trending below peak levels last year but still significant relative to operating scope, sustaining sufficient runway beyond current liquidity will depend on maintaining revenue momentum or accessing additional financing if needed—particularly as production scales accelerate [F1][S23].

Growth Drivers and Future Market Opportunities

Looking forward analysis suggests Amprius’ addressable market is poised for expansion aligned with growing electrification trends within aerospace domains such as drones (UAS), high-altitude pseudo satellite substitutes (HAPS), and increasingly commercial eVTOL aircraft — segments demanding light-weight yet highly energy-dense batteries not achievable with conventional materials [N1][N6][S1].

Development of the next-generation SiMaxx battery promises enhanced performance specifications building upon SiCore’s footprint potentially unlocking broader applications beyond current niche aviation deployments into land-based electric vehicles where size-to-performance ratios are critical but remains early-stage with production awaiting scale validation [N6][S1]. Regulatory frameworks emphasizing sustainability and emission controls may indirectly assist market demand for premium high-performance lithium batteries.

However, these opportunities are tempered by competitive pressures from composite silicon alternatives as well as more established lithium-ion producers investing heavily in incremental improvements; continual innovation imperative alongside successful transition from prototype demonstrations to volume production capability will be decisive [S9][N6].

Operational Risks and Supply Chain Challenges Facing Expansion

Supply chain dependencies stand out as material risks given Amprius’ reliance on third-party manufacturers overseas particularly within South Korea consortiums plus critical sourcing of proprietary silicon materials governed under exclusive agreements primarily restricted geographically to North America via partner Berzelius [S6][S11][S24]. Recent Chinese export controls targeting battery precursor materials threaten availability or cost profiles affecting timing or fulfillment reliability hence contingency plans including NDAA-compliant sourcing are actively managed though pose inherent uncertainties that could disrupt operations or inflate costs unpredictably.

Intellectual property protection while robust remains vulnerable due to global enforcement variability posing risk of design circumvention or infringement costly litigations which could divert resources or dilute competitive positioning; trade secrets augment legal protections yet monitoring enforcement efficacy remains labor-intensive [S16][S19]. Customer concentration also introduces execution risk with elongated sales cycles particular within government contracts that require extensive certification regimes delaying ramp timing uncertainty impacting near-term revenue predictability [S7][S18].

Investor Expectations and Key Upcoming Milestones

Investor sentiment has been buoyed recently following notable revenue beats despite persistent net losses highlighted during Q4/ FY2025 earnings calls which catalyzed positive coverage initiations including Craig-Hallum recommending buy based on growth potential balanced against risk profile (sources: N8,N11). Stock price volatility reflects market appetite for hyper-growth narratives weighed against scale-up capital demands.

Critical upcoming milestones include completion of Fremont pilot line expansion targeting 10 MWh capacity enabling rapid prototype iteration essential for securing additional design wins across aviation OEMs; monitoring recurring order inflows particularly from defense contractors scouting resilient battery solutions underpins validation efforts key to sustaining commercial momentum [N1][N8].

Watching metrics related to unit economics improvements as throughput rises alongside operational yield gains within outsourced manufacturing ecosystems will be essential signals for transition toward profitability thresholds while managing supply continuity remains paramount.

This report distills information solely from cited SEC filings ([F1],[S#]) and publicly available news transcripts ([N#]) without extrapolation beyond documented facts or speculative forecasts about future performance or valuations.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments