Kinder Morgan Strengthens Pipeline Leadership with Robust Q1 2026 Results

Strong Q1 revenues and income underpin Kinder Morgan's operational continuity amidst leadership changes in its midstream infrastructure business.

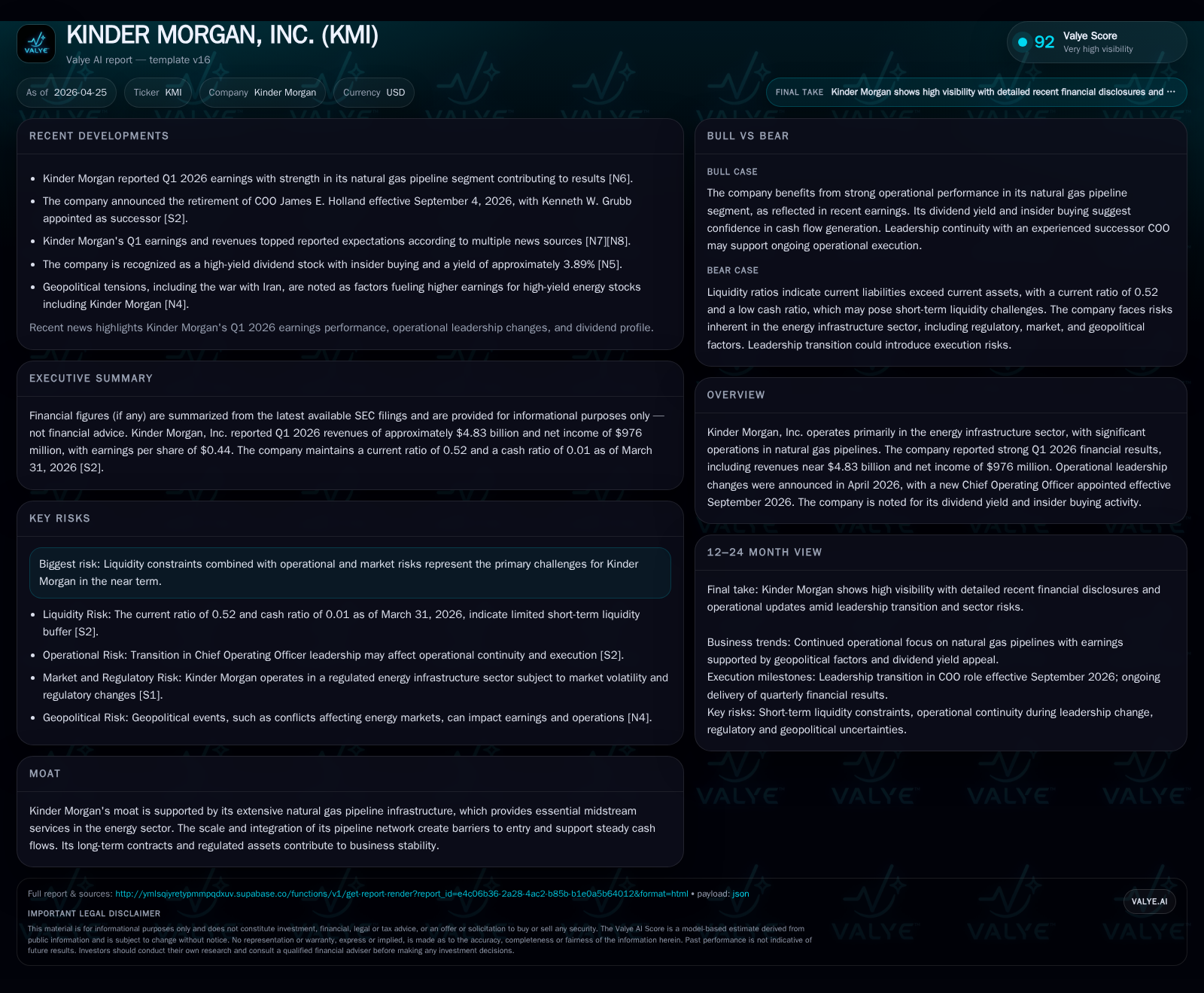

Kinder Morgan reported solid first quarter 2026 financial results, with revenues approximating $4.83 billion and net income of $976 million, signaling stable cash flow generation in its core natural gas pipelines segment. The announcement of a COO transition to Kenneth W. Grubb reflects an internally cultivated leadership path that supports operational depth and continuity. The company's extensive pipeline network and fee-based contracts underpin its competitive moat, while growth prospects rest on sustained contracted volumes and dividend appeal, tempered by liquidity constraints and leverage considerations.

First Quarter 2026 Operating Update: Performance Highlights and Leadership Transition

Kinder Morgan’s latest quarterly filing dated April 24, 2026 [S2] reveals a solid operating landscape anchored by Q1 revenues near $4.83 billion and net income reaching approximately $976 million—a reflection of durable demand in its midstream energy infrastructure segment. This performance aligns with analysts’ expectations noted around the earnings release timing [N5][N6][N9]. Importantly, the company reported no material shifts in risk factors or unexpected operational disruptions [S4].

Strategic leadership continuity forms an integral part of this update. The April 22, 2026 Form 8-K discloses that COO James E. Holland will retire effective September 4, 2026 [S3]. His successor, Kenneth W. Grubb, brings over 35 years of deep tenure within Kinder Morgan’s natural gas pipeline operations, having held a variety of senior roles including earlier COO experience within the segment. This internal succession plan minimizes transitional risks and reinforces operational depth within critical midstream management.

Business Model Deep Dive: Midstream Infrastructure Driving Stable Cash Flows

Kinder Morgan primarily generates revenue through fee-based contracts underpinning its vast natural gas pipeline network [S1]. These long-term agreements afford the company high visibility into cash flows irrespective of commodity price swings, which is a defining characteristic for midstream pipeline operators. Fee payments often involve committed minimum volumes with contractual take-or-pay provisions that ensure baseline revenue stability.

The company’s portfolio includes both regulated assets—subject to cost-of-service tariffs—and unregulated contracts negotiated at market rates, blending revenue sources to balance risk and return profiles [S1]. High integration between pipelines creates intrinsic switching costs for customers who rely on service continuity and connectivity offered exclusively by Kinder Morgan’s network topology.

This model supports a consistent dividend yield widely attractive to certain income-focused investors. Insider buying activity reported recently further signals confidence in the sustainability of these cash flows.

Competitive Positioning: Moat Built on Extensive Natural Gas Pipeline Network

Kinder Morgan maintains one of the largest natural gas pipeline systems in North America, which establishes significant barriers to entry [S1]. The scale delivers operating leverage advantages while limiting effective competition due to both geographic coverage and capital intensity hurdles for new entrants.

Pricing power is nuanced; regulated assets impose tariff ceilings set by federal or state authorities ensuring reasonable returns but constraining profit margins. Conversely, unregulated segments allow dynamic pricing responsive to supply-demand fundamentals enhancing margin potential when market conditions are favorable.

Regulatory compliance acts as both a constraint and moat component—operational licenses hinge upon strict adherence to safety and environmental standards, where Kinder Morgan’s established track record affords persistent approval rights, thereby maintaining its indispensability within the energy midstream value chain.

Growth Enablers: Contracts, Dividend Strategy, and Market Opportunities

Future growth drivers largely stem from sustained or growing contracted volumes across natural gas pipelines fueled by secular trends like increased utilization for power generation and industrial use [S1]. While the U.S. energy transition may pose structural threats over decades, midterm demand for reliable gas transport remains robust.

The company’s disciplined capital allocation includes organic expansions and capacity investments aligned with contracted customer commitments—capex has risen steadily over recent years exceeding $3 billion annually [F1]. This supports incremental fee revenue without speculative volume risk.

Dividend policy is integral to Kinder Morgan’s shareholder value proposition [N14]. Predictable cash flows combined with steady distributions foster investor retention even amid volatile commodity markets—a factor reinforcing stock attractiveness relative to peers.

Near-Term Risks and Operational Constraints Amid Sector Volatility

Liquidity analysis reveals a current ratio of approximately 0.52—signaling constrained short-term asset coverage against liabilities as per the March 31, 2026 balance sheet snapshot [F1]. Additionally, total debt hovers around $29.7 billion with net debt close behind at $29.65 billion given modest cash reserves [F1], anchoring leverage at levels typical for capital-intensive midstream firms but requiring careful covenant diligence.

Market risks tied to energy demand fluctuations persist as indirect operational constraints; while fee-based contracts mitigate volume exposure, certain unregulated segments remain sensitive to commodity price cycles adversely impacting margins [S7]. Regulatory risks also continue but showed no material shifts in the latest risk disclosures [S4].

Key Upcoming Catalysts: Monitoring Execution and Operational Milestones

Investors should focus on execution updates regarding capex projects initiated over previous years which represent pivotal growth milestones—completion timelines and achieved return metrics will offer insights into organic expansion efficacy [S2][N12][N13].

Quarterly guidance announcements will be scrutinized for any margin movement that may reflect underlying cost pressures or volume changes amid broader inflationary or market headwinds.

The newly appointed COO Kenneth W. Grubb's integration effects on operational efficiency will also be observed given his deep expertise but fresh executive leadership responsibilities starting September 2026 [S3].

Financial Overview: Balancing Leverage With Cash Generation

Historical performance (annual)

|

| FY | Rev ($bn) | Net ($bn) | CFO ($bn) | OpInc ($bn) | Rev YoY | Net YoY |

|---|---|---|---|---|---|---|

| 2025 | 16.9 | 3.1 | 5.9 | 4.7 | +12.2% | +17.0% |

| 2024 | 15.1 | 2.6 | 5.6 | 4.4 | -1.5% | +9.3% |

| 2023 | 15.3 | 2.4 | 6.5 | 4.3 | -20.1% | -6.2% |

| 2022 | 19.2 | 2.5 | 5.0 | 4.1 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

|

| FY | Buybacks ($mm) | FCF ($bn) | ROE% |

|---|---|---|---|

| 2025 | 0 | 2.9 | 9.8 |

| 2024 | 7 | 3.0 | 8.6 |

| 2023 | 522 | 4.2 | 7.9 |

| 2022 | 368 | 3.3 | 8.3 |

Source: SEC companyfacts cache [F1].

Kinder Morgan’s financial profile at end-Q1 2026 demonstrates balanced tension between leveraging scale and preserving robust cash generation capabilities:

- Cash & equivalents stand at roughly $72 million against current liabilities totaling about $5.18 billion resulting in a subdued current ratio (~0.52) highlighting tight short-term liquidity cushions [F1].

- Total debt aggregates near $29.7 billion with net debt roughly equivalent due to low cash holdings reflecting reliance on long-term financing structures common for infrastructure players [F1].

- Operating cash flow for FY2025 was about $5.92 billion annualized indicating healthy operating profitability supporting dividend commitments despite capital expenditure outlays exceeding $3 billion yearly [F1].

- Return on equity approximated at 9.8% offers moderate investor returns consistent with midstream utility-style asset profiles balancing steady income with moderate growth prospects [F1].

- Free cash flow remains positive albeit modest relative to size reflecting reinvestment priorities alongside shareholder distributions.

This financial construct implies ongoing prudence in capital management is essential; limited liquidity headroom underscores importance of maintaining covenant compliance while leveraging operational predictability derived from fee-based contracts.

Disclaimer: This analysis is based solely on publicly available SEC filings dated April 24, 2026 ([S2]), April 22, 2026 ([S3]), February 13, 2026 ([S1]) alongside verified companyfacts data ([F1]) and relevant external news sources referenced herein. It does not constitute investment advice or recommendations.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments