Origin Materials’ Strategic Outlook After 2025 Year-End Results

Examining Origin Materials' 2025 results uncovers key operational challenges and potential growth vectors amid ongoing investment in sustainable chemical technologies.

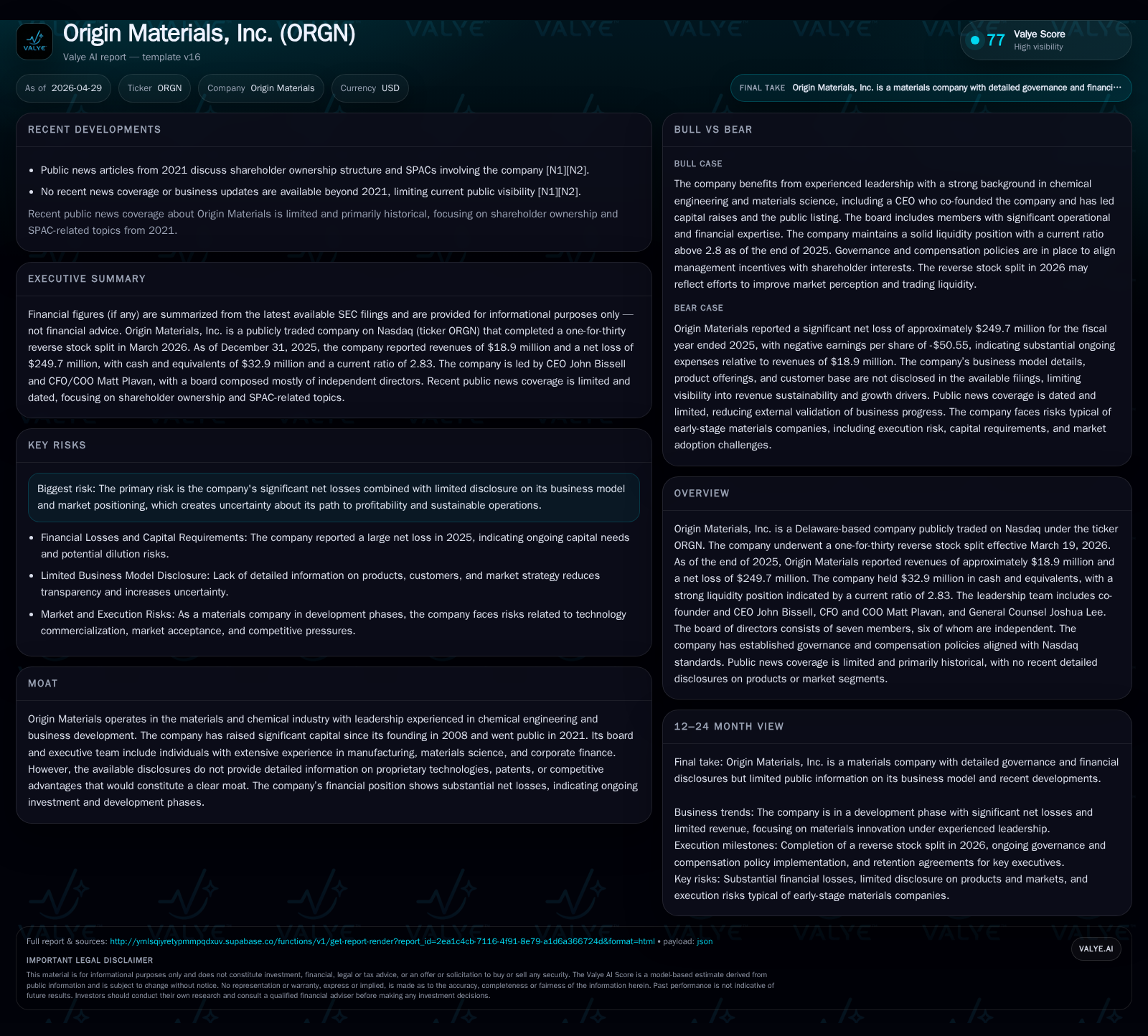

Origin Materials reported $18.9 million in revenue and a substantial net loss of $249.7 million for 2025, reflecting continued investment in technology and capacity expansion. The company’s liquidity remains sufficient with $32.9 million cash and a current ratio of 2.83, underscoring operational runway despite losses. Its business model centers on developing bio-based materials to serve customers demanding sustainable chemical inputs, yet commercial scale adoption remains nascent. Competitive dynamics encompass established chemical manufacturers and evolving regulatory pressures favoring green solutions, but the company faces execution risks tied to technological scale-up and sustained capital needs.

2025 Year-End Operating Update and Its Implications

Origin Materials disclosed its financial results for the fiscal year ending December 31, 2025 in an 8-K filing dated March 27, 2026 [S3]. Reported revenue stood at $18.9 million while net loss reached a significant -$249.7 million [F1]. This gap illustrates the company's position firmly in a heavy investment phase characteristic of emerging chemical technology enterprises scaling complex manufacturing capabilities.

Notably, liquidity metrics remain adequate relative to operating demands: cash and equivalents totaled $32.9 million at year-end with current assets surpassing liabilities by nearly threefold (current ratio of 2.83) [F1]. These figures suggest manageable short-term financial stability despite operating deficits. Further, the company effected a one-for-thirty reverse stock split in March 2026 to optimize share structure and enhance trading characteristics post-2025 [S14],[S17].

Taken together, the recent results mark a critical juncture where Origin balances foundational investments against early market revenues — setting up strategic decisions for progressing commercialization while monitoring capital efficiency.

Business Model Overview and Product Quality Considerations

Origin Materials generates revenue primarily through the production and sale of advanced materials derived from sustainable feedstocks directed at chemical manufacturing clients seeking carbon-negative or net-zero solutions [S1]. Its nascent product lines focus on precursor chemicals that can substitute fossil-based inputs in packaging plastics and related materials.

While specific unit economics details remain undisclosed, the prevailing low revenue relative to high operating expenses reflects developmental-stage commercialization efforts rather than mature sales volumes [S1]. Customer engagement appears concentrated among select large firms under offtake agreements intending to secure access to greener chemical supplies [S5].

The product quality imperative involves maintaining consistency and scalability in novel bio-based carbon intermediates — an inherently challenging process translating lab innovations into industrial throughput [S1]. The company leverages proprietary processes but has not explicitly detailed patent portfolios or technological moats, implying competitive differentiation hinges currently on execution pace rather than intellectual property exclusivity.

Industry Structure and Competitive Dynamics

Positioned within the chemicals sector pivoting towards sustainability, Origin competes against entrenched petrochemical incumbents alongside emerging renewable material startups [S1]. The industry's value chain spans upstream biomass sourcing through processing and downstream polymer or packaging integration.

Barriers include large capital requirements for manufacturing scale-up, stringent regulatory frameworks incentivizing lower-carbon materials (e.g., extended producer responsibility laws), and volatility in feedstock supply prices [S1]. Established players possess cost advantages due to scale but face strategic pressures transitioning their portfolios towards greener chemistries.

In this ecosystem, Origin strives to carve out niche leadership by offering innovative carbon-negative pathways; however, its relatively small size and ongoing development phase limit immediate competitive positioning.

Growth Drivers Anchored in Key Performance Indicators

Several quantifiable factors underpin Origin's growth thesis as illustrated by recent filings:

- Facility Commissioning: Progress on new plants capable of ramping material output represents a critical KPI directly affecting volume-driven revenues [S1],[S5].

- Offtake Agreements: Expansion or renewal of supply contracts with major CPG companies signal commercial acceptance and underpin volume visibility [S5].

- Technology Scale-Up: Achieving reliable full-scale manufacturing processes reduces costs per unit thereby improving margin potential — fundamental to long-term profitability [S1].

- Capital Deployment Efficiency: Management’s ability to convert invested capital into productive assets efficiently impacts burn rate control and operational leverage [S1].

Monitoring these KPIs provides actionable insight into crossing thresholds where development-phase costs give way to steady-state industrial chemistry economics.

Risks, Constraints, and Execution Challenges

Despite promising technology themes, Origin faces substantive headwinds:

- Persistent Net Losses: The steep net deficit (-$249.7 million) underscores extensive R&D and infrastructure spending without offsetting mature revenues yet realized [F1].

- Capital Needs Uncertainty: The necessity for ongoing funding rounds may dilute existing equity or increase leverage absent clear path to positive cash flow,[F1].

- Scale-Up Risks: Manufacturing processes for novel bio-materials carry inherent technical risks potentially leading to delays or cost overruns.

- Competitive Pressure: Larger incumbents accelerating green material initiatives could limit market share opportunities or compress margins [S1].

- Regulatory Flux: Dependence on regulatory incentives introduces some unpredictability regarding policy support durability.

These risks necessitate vigilant operational execution combined with prudent financial stewardship.

What to Watch: Upcoming Milestones and Operational Markers

Market participants should prioritize tracking several near-term developments:

- Updates on production facility commissioning timelines and output ramp rates as indicators of commercialization momentum [S3],[S1].

- Announcements concerning expansion or amendments of customer supply agreements reflecting demand trajectory [S5].

- Quarterly updates revealing revenue progression relative to cost containment efforts highlighting scaling efficiencies [S3].

- Management commentary during investor communications addressing burn rate normalization strategies.

Such milestones will clarify whether Origin transitions from capital-intensive development toward revenue-generating enterprise sustainably.

Latest Financial Snapshot Supporting Strategic Review

Latest financial snapshot

| Metric | Value | Period |

|---|---|---|

| Cash & equivalents | $33mm | |

| 2025-12-31 | ||

| Current assets | $81mm | |

| 2025-12-31 | ||

| Current liabilities | $29mm | |

| 2025-12-31 | ||

| Current ratio | 2.83x | |

| 2025-12-31 |

Source: SEC companyfacts cache [F1].

| Metric | Value (USD) |

|---|---|

| Revenue | $18.9 million |

| Net Loss | -$249.7 million |

| Cash & Equivalents | $32.9 million |

| Current Ratio | 2.83 |

Origin Materials maintains a strong liquidity buffer relative to current liabilities ($28.5 million) with cash reserves ample for near-term operational needs despite considerable losses reported for the period ending December 2025 [F1]. Total debt levels appear manageable though last recorded figure is dated end-2023 at approximately $5.1 million with net debt negative due to cash holdings [F1], confirming low financial leverage currently.

This analysis synthesizes late-stage calendar year 2025 filings anchored principally on the March 2026 event disclosure alongside annual amended filings incorporating governance updates as of April 29, 2026. While Origin Materials demonstrates foundational strengths such as emerging product relevance aligned with sustainability mandates and sufficient liquidity for continued development, critical uncertainties persist regarding scaling execution and path toward profitability.

Readers should interpret financials as consistent with an investment-intensive materials startup moving through a protracted commercialization lifecycle lacking broad market penetration thus far. Monitoring milestone delivery around facilities readiness and sales expansion offers the clearest signals for evolution toward financially self-sustaining operations.

Disclaimer: This analysis is intended for informational purposes only. It does not constitute investment advice or recommendations regarding Origin Materials’ securities.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments