YXT.COM GROUP HOLDING Ltd Faces Margin Improvement Amid Revenue Contraction and Liquidity Constraints

Latest quarterly filings spotlight YXT’s operational resilience in a challenging environment marked by declining revenues and regulatory pressures.

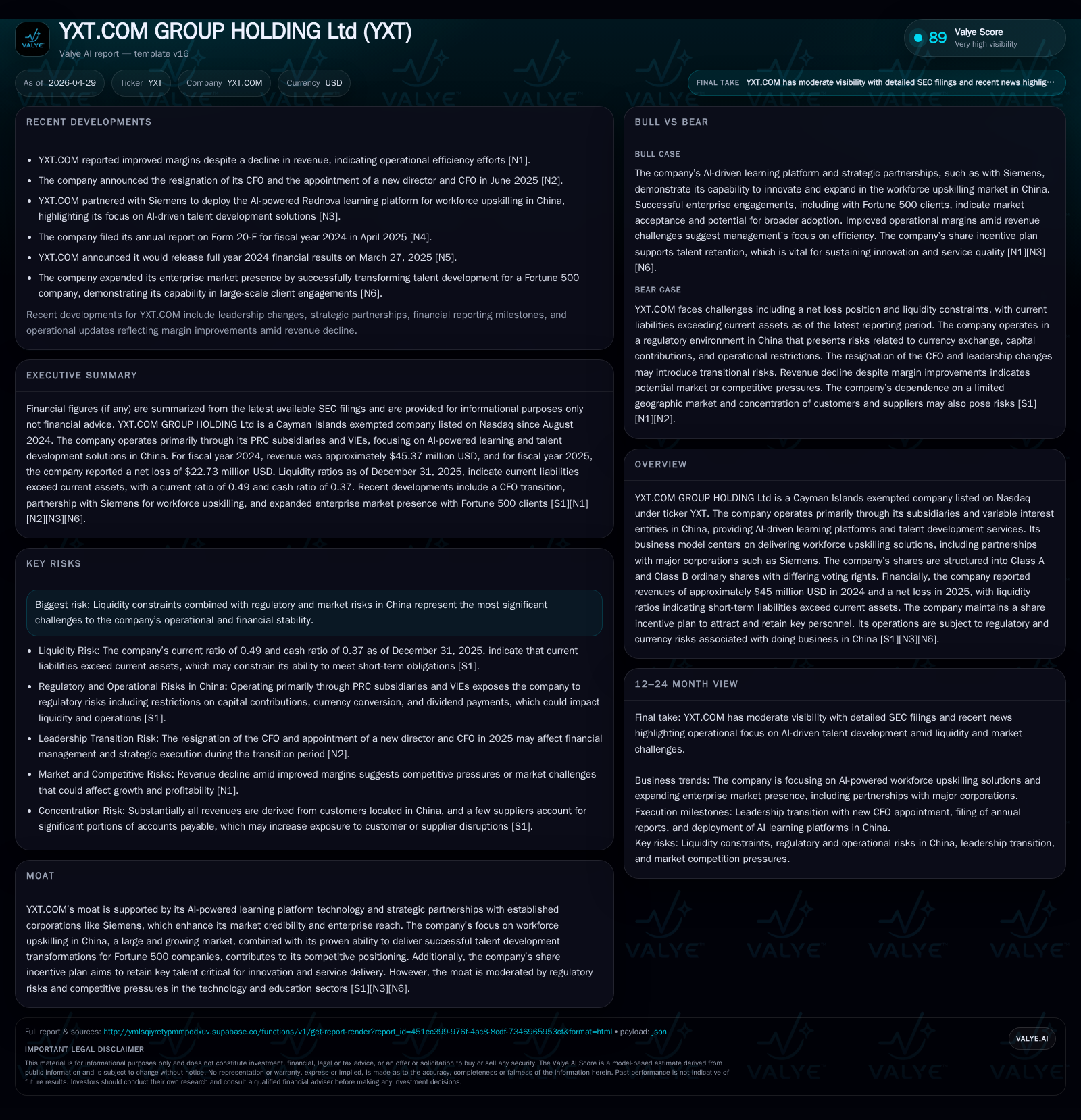

YXT.COM GROUP HOLDING Ltd reported a continued net loss in 2025 despite notable margin improvements. The company’s AI-driven workforce upskilling platform retains strategic partnerships with major corporations such as Siemens, supporting enterprise adoption amid a competitive Chinese edtech landscape. However, liquidity challenges persist, with current liabilities substantially exceeding current assets, raising near-term financial risks. Regulatory risks remain salient given the company's operational structure within China’s evolving technology regulations. Growth prospects hinge on expanding enterprise contracts and R&D innovation, while containment of operating costs will be crucial.

Recent Operating Update

YXT.COM GROUP HOLDING Ltd's latest filing as of March 31, 2026, validated its adherence to annual reporting under Form 20-F without indicating new operational disruptions or business pivots [S2]. This establishes continuity in disclosure but offers limited incremental insights into near-term performance changes.

The annual report dated April 29, 2026, remains essential to contextualize recent operating dynamics. Notably, YXT experienced deconsolidation of its previously controlled entity CEIBS PG as of January 2024 following an adverse arbitration award that was upheld by the High Court of Hong Kong in early 2025. The loss of control over CEIBS PG necessarily impacted the scale of consolidated revenues and earnings comparisons historically [S1].

Most recently reported revenue for fiscal year ending December 31, 2024, stood at approximately $45.4 million USD [F1], while the company recorded a net loss nearing $22.7 million USD for calendar year 2025 according to their financial snapshots [F1]. Despite top-line contraction vis-à-vis earlier years—partly attributable to structural changes post-CEIBS PG deconsolidation—operating margins have improved moderately as per commentary from Nasdaq disclosures [N1]. This margin improvement likely reflects cost rationalization efforts and a shift towards higher-value service contracts.

Business Model

YXT operates predominantly through its subsidiaries and variable interest entities (VIEs) in China, delivering AI-driven learning solutions designed to drive workforce upskilling and talent development. Its revenue model hinges on SaaS-like platform subscriptions, customized learning modules powered by proprietary AI capabilities, and client-specific corporate training services.

The company’s primary customers are large enterprises requiring digital transformation in human capital management. Partnerships with recognized multinational firms such as Siemens not only validate its product offerings but also facilitate deeper penetration into China's enterprise technology ecosystem [S1].

Revenue generation depends significantly on contract renewals and expansion within existing accounts alongside acquisition of new corporate clients. Pricing mechanics involve recurring fees linked to platform access and service customization levels; thus volume (number of users) and usage intensity directly influence monthly recurring revenue streams.

A critical component includes YXT's commitment to research and development focusing on enhancing AI algorithms, cloud infrastructure upgrades, and developing new digital learning products tailored for market demand shifts [S4]. This aligns with securing differentiated technological advantages necessary amidst fierce competition from both local Chinese tech firms specializing in education technology as well as international players.

Retention is fostered through integrated solutions that embed into corporate HR workflows creating switching costs; however, pricing power may face pressure given alternative offerings available in the rapidly evolving Chinese edtech market.

Industry Structure and Competitive Position

China’s education technology sector has witnessed sharp regulatory recalibrations centered around online tutoring restrictions and foreign investment barriers over recent years. Against this backdrop, YXT's positioning within enterprise upskilling differentiates it from consumer-focused edtech players which have been more heavily impacted.

The B2B segment for digital talent development remains large but competitive with key participants including domestic listed companies offering blended e-learning platforms and multinational HR tech firms bringing global expertise. YXT’s AI-centric platform combined with institutional relationships like Siemens provides a defensible niche supported by tailored solutions addressing complex corporate training needs.

However, the company confronts risks related to regulatory oversight governing data privacy, foreign ownership structures via VIEs, and currency controls restricting capital repatriation or funding inflows [S6][S7]. These structural nuances impose operational constraints uncommon in Western markets.

Growth Drivers

YXT’s growth thesis rests significantly on three pillars:

- Technology Innovation: Sustained investment in AI-powered product enhancements targeting scalability of cloud platforms and intelligent learning analytics enables richer user experiences aligned with emerging corporate demands [S4].

- Enterprise Expansion: Leveraging trusted relationships with Fortune 500 clients facilitates cross-selling additional modules and expanding user bases within current clientele; this drives volume growth critical for scaling subscription revenues.

- Market Penetration: Growing employer recognition around reskilling necessities amid labor market transformations positions YXT favorably within an expanding total addressable market in China’s digital economy.

These drivers are measurable via KPIs including backlog bookings for contracted services, renewal rates on software subscriptions, active user counts on platforms, and pipeline conversion ratios reported internally though not publicly detailed.

Risks / Watchpoints / Growth Constraints

Despite strategic strengths, YXT grapples with several headwinds:

- Liquidity Deficits: As of year-end 2025, current assets were roughly $25.6 million USD against current liabilities exceeding $51.7 million USD resulting in a low current ratio (~0.49), highlighting short-term liquidity risk that demands careful cash flow management or financing actions [F1].

- Regulatory Uncertainty: The VIE structure exposes the company to potential adjustments from Chinese regulators regarding foreign investment treatment or restrictions on funds moving offshore impacting capital availability or dividend distributions [S5][S14].

- Operational Legal Risks: The prior arbitration outcome evidenced by CEIBS PG deconsolidation underscores exposure to litigation outcomes which could further impair consolidated results or reputation if unfavorable judgments arise [S6].

- Competitive Intensity: Rapid innovation cycles and aggressive pricing behaviors by competitors introduce margin pressures requiring ongoing differentiation investments.

- Internal Control Weaknesses: The company disclosed material weaknesses within financial reporting controls necessitating remedial staffing hires and protocol improvements to restore reliability in SEC disclosures [S22].

These factors form critical considerations that may constrain growth trajectories or investor confidence unless mitigated effectively.

What to Watch Next

Key milestones that will illuminate YXT’s trajectory include:

- Quarterly revenue trends particularly evidence of stabilization or growth following prior declines.

- Renewal rate disclosures from key enterprise clients reflecting client satisfaction and retention strength.

- Cash flow statements indicating easing or exacerbation of liquidity pressures.

- Announcements regarding regulatory developments especially those affecting VIE arrangements or dividend payment abilities.

- Progress updates on R&D initiatives signaling capability enhancements that could spur competitive advantage expansions.

- Execution effectiveness concerning share repurchase program deployment potentially influencing shareholder value perception [S19][N1].

Investor attention should focus sharply on these operational metrics as indicators of execution robustness amid underlying structural challenges.

Financial Profile (Latest Snapshot)

Latest financial snapshot

The financials depict a business contending with losses but showing operational margin improvement efforts alongside constrained liquidity positions necessitating financing prudence [F1][N1][S15]. The balance sheet reflects significant short-term obligations relative to readily available assets highlighting working capital management as a near-term priority.

This analysis is based solely on disclosed filings from YXT.COM GROUP HOLDING Ltd as detailed above through April 29, 2026. It does not constitute investment advice but aims to present an impartial valuation narrative grounded in verifiable data.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments