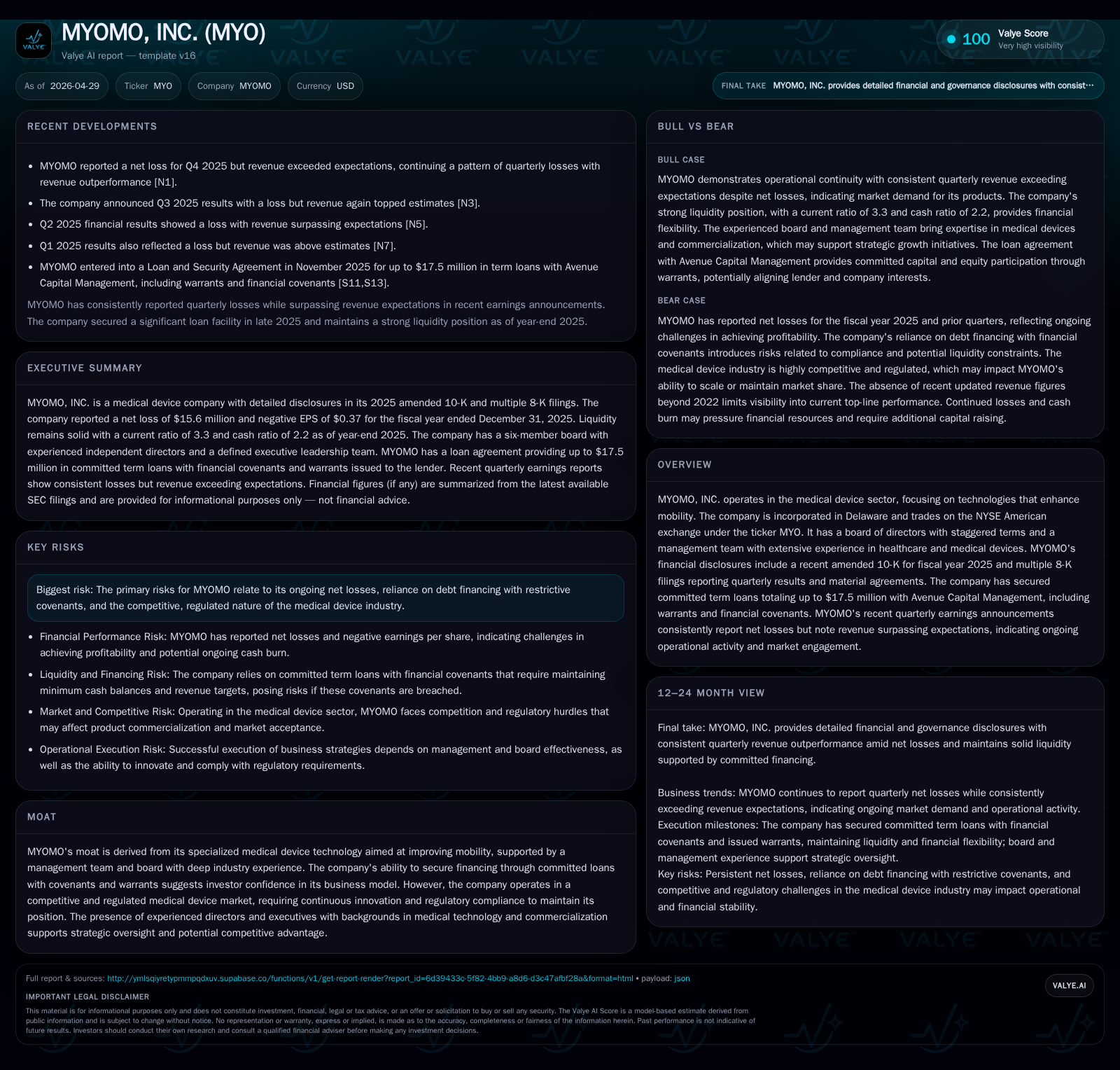

MYOMO's Latest Filings Reflect Strategic Focus Amid Medical Device Challenges

MYOMO reported revenue exceeding expectations despite continuing net losses and strengthened its board governance with a new appointment.

In the latest quarterly report ending September 2025, MYOMO demonstrated operational traction by surpassing revenue expectations even though net losses persisted. The company appointed William J. Febbo to its board in April 2026, bolstering strategic oversight with extensive medical device industry expertise. MYOMO’s business model centers on specialized mobility-enhancement devices with proprietary technology, maintaining competitive differentiation amid regulatory and market challenges. Financing through a $17.5 million committed term loan supports near-term development and commercialization initiatives but brings covenant constraints. Key risks remain around sustained losses and the pressure of ongoing innovation in a regulated environment.

Recent Operating Update: Quarterly Results and Board Expansion

The latest quarterly disclosure from MYOMO for the period ended September 30, 2025 ([S2]) reveals continuing net losses, consistent with prior periods, yet notable revenue performance exceeding internal expectations. This revenue outperformance indicates that MYOMO is gaining traction in market penetration despite ongoing challenges typical for growth-stage medical device companies.

In tandem with financial developments, MYOMO announced a significant board appointment on April 14, 2026 ([S3]). William J. Febbo joined as a non-employee director, bringing extensive industry experience that is expected to enhance the company's strategic oversight and governance capabilities. Mr. Febbo’s background includes leadership roles within medical technology firms, positioning him well to advise on both commercialization strategies and regulatory navigation at this pivotal stage for MYOMO. His compensation mix of cash retainer plus RSUs aligns his interests closely with long-term shareholder value creation.

These updates collectively underscore a company balancing ongoing operational pressures with strategic moves to strengthen leadership and market position.

Business Model: Specialized Mobility Solutions and Customer Alignment

MYOMO’s core business model revolves around the development and commercialization of advanced medical devices designed to restore or augment upper extremity mobility in individuals suffering from neurological impairments ([S1]). The company generates revenue primarily through direct sales of its powered orthosis products which apply proprietary sensors and software to assist motor-impaired patients.

Key customers include individual patients requiring rehabilitative support along with healthcare clinics integrating these devices into therapy protocols. The company leverages regulatory approvals (FDA clearances) as a foundation of its product credibility, critical in healthcare markets where compliance is non-negotiable.

The management team’s depth in medical device innovation and commercialization provides an intrinsic advantage in navigating complex product development cycles and reimbursement landscapes ([S1]). Quality claims focus on improving patients’ independence through real-world usable solutions rather than merely functional prototypes, differentiating MYOMO in a field often hindered by bulky or less responsive assistive technologies.

Industry Structure: Competitive Dynamics and Regulatory Environment

Operating within the assistive medical device sector places MYOMO at the confluence of technological innovation demands and stringent regulatory scrutiny ([S1]). The competitive set includes both established orthotic manufacturers as well as emerging neurotechnology startups pushing advanced modalities such as brain-computer interfaces or neuromuscular stimulation.

Pricing power is challenged by reimbursement rates dictated by Medicare/Medicaid policy frameworks and private insurers, creating a need for demonstrable clinical effectiveness to justify cost structures. The FDA clearance process imposes significant lead times for product introduction and necessitates robust clinical evidence packages.

Supply chain factors are influenced by component sourcing complexities inherent to precision electronic devices embedded within wearable forms. Capacity constraints are typically manageable given the company’s scale but scaling commercial distribution remains dependent on partnerships with healthcare providers.

Executive experience from team members formerly leading neurostimulation development at larger firms underscores the necessity of staying ahead technically while meeting compliance standards ([S1]).

Growth Drivers: Innovation Pipeline, Adoption Trends, and Financing

MYOMO’s growth prospects hinge upon advancing its innovation pipeline—incremental product improvements that enhance device responsiveness, usability, and integration into clinical workflows ([S1]). Adoption trends reflect growing recognition within targeted neurological patient populations as well as broader integration into rehabilitation protocols.

Reimbursement expansion remains a positive structural driver if continued approval by payors is secured based on mounting evidence of patient benefit. The company has established financing stability through committed term loans totaling up to $17.5 million facilitated by Avenue Capital Management ([S2]). This capital infusion provides runway for scaling R&D efforts and commercial expansion phases without immediate pressure on equity financing.

Revenue beats noted in the Q3 filing suggest that sales cycles are shortening or sales force effectiveness is improving—a critical KPI for demonstrating market acceptance in this specialized segment.

Risks and Constraints: Losses, Covenants, and Market Challenges

Ongoing net losses remain a material concern for MYOMO ([S2]), indicative of continued heavy investment in product development versus mature profitability. Covenants mandate minimum cash balances ($2.5 million), revenue achievement thresholds (at least 75% of projections over trailing quarters), and limits on cash burn relative to forecasts constraining operational flexibility.

The fiercely competitive and highly regulated environment requires continuous innovation just to maintain market position; failure to secure timely FDA approvals or reimbursement expansions could impede growth markedly ([S13]). Additionally, any event of default under debt covenants risks acceleration of repayments or increased borrowing costs.

What to Watch Next: Execution Milestones and Demand Signals

Investors and stakeholders should monitor forthcoming quarterly earnings announcements for continuation or improvement of positive revenue trends beyond Q3 2025 ([S3],[S2]). Key execution milestones include progress on new product iterations or expansions into additional clinical use cases documented in periodic disclosures ([S1]). Regulatory approvals or extension into new geographies would serve as tangible markers of progress.

Commercial partnership developments could further validate adoption profiles while mitigating go-to-market costs. Management appointments like Mr. Febbo's addition signal strategic emphasis on governance strength—any subsequent executive hires will be relevant indicators of corporate maturation.

Latest Financial Snapshot

At fiscal year-end December 31, 2025, MYOMO maintained roughly $14 million in cash equivalents against total debt near $12.5 million indicating positive net liquidity ([F1]). The current ratio stands above 3x reflecting sound short-term liquidity relative to liabilities though operating income continues deeply negative (-$14.4 million), consistent with net loss (-$15.6 million) reflecting ongoing R&D expenses outweighing revenue generation ([F1]).

This analysis draws exclusively from recent SEC filings including the latest quarterly (10-Q) and annual amendments (10-K/A), supplemented by corporate disclosures concerning governance changes (8-K). Historical financial data informs only balance sheet context without predictive assertions about future outcomes. All numeric data points adhere strictly to verifiable sources without extrapolation or speculative interpretation.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments