Kun Peng International Ltd. Faces Liquidity Pressure as Online Health Sales Slow

Kun Peng International’s May 2026 quarterly filing reveals severe liquidity constraints and ongoing losses, raising near-term operational risks amid a competitive Chinese e-commerce market.

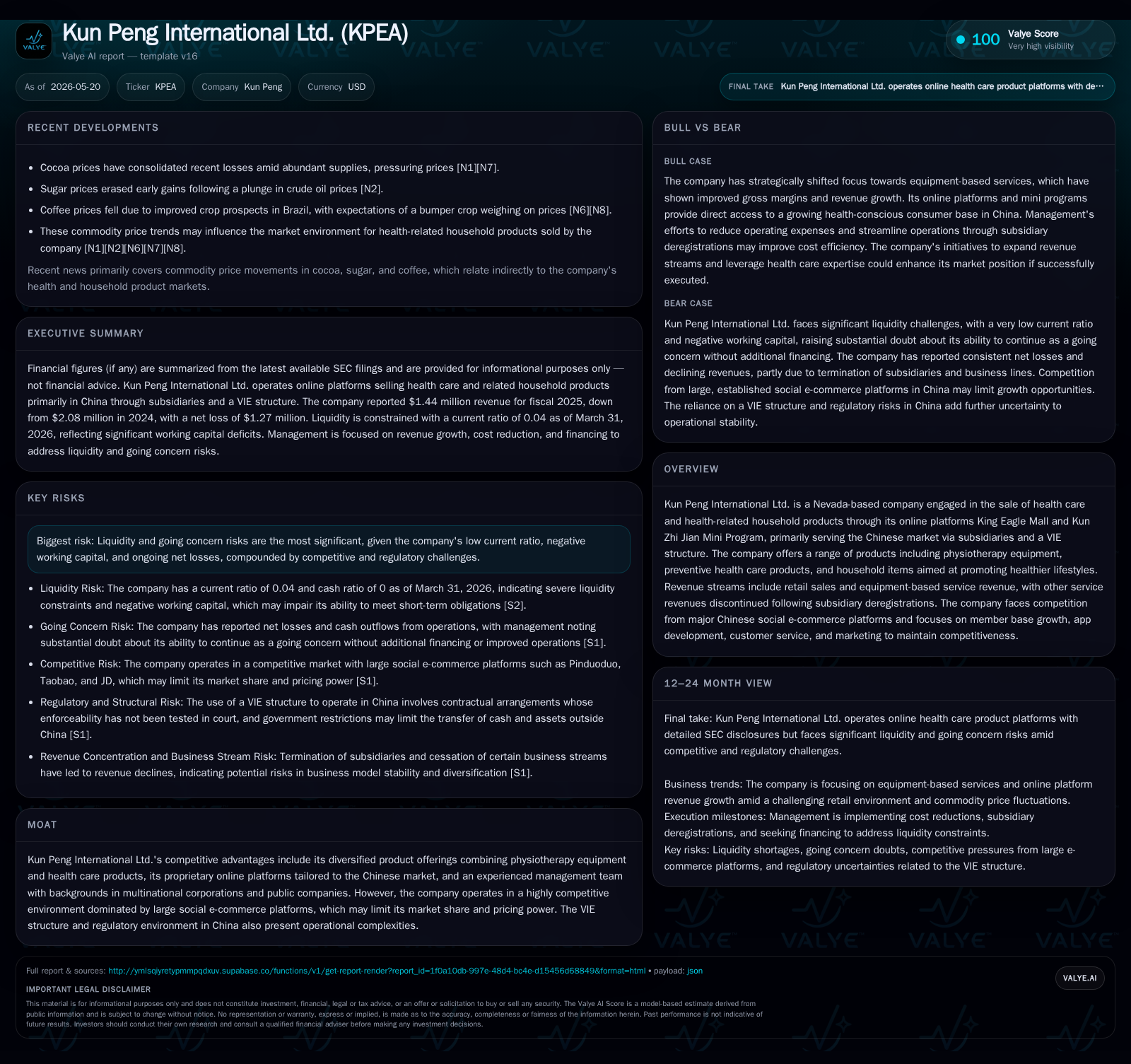

Kun Peng International Ltd., a U.S.-listed company selling health care and wellness products primarily through its Chinese-focused online platforms, reported critical liquidity stress as of Q1 2026, with a cash balance of under $20,000 against current liabilities exceeding $9.6 million. The company continues to operate at a loss driven by declining online retail sales and high operating expenses. Its business model hinges on proprietary e-commerce platforms serving the Chinese market via a Variable Interest Entity (VIE) structure, but faces intense competition from giants like Pinduoduo and Taobao, along with regulatory uncertainties. Growth efforts focus on platform improvements and membership expansion, although financing and regulatory risks remain significant headwinds.

As of March 31, 2026, the company held approximately $19,768 in cash equivalents against current liabilities nearing $9.68 million—a current ratio around 0.04 [S2][F1]. This negative working capital position underscores an imminent funding gap that threatens ongoing operations unless remedied swiftly.

Compounding these constraints is the continuation of net operating losses; recent annual figures show operating losses above $1.7 million with net loss exceeding $1.26 million for fiscal year ended September 30, 2025 [F1]. Such entrenched losses reflect both shrinking revenues in online health product sales and high operating costs associated with platform management, marketing campaigns, and customer service [S1]. This acute cash burn dynamic raises significant going concern issues for the company absent timely capital injections or sustainable margin improvement.

Business Model and Product Portfolio: Online-Driven Health Care and Wellness Goods

Kun Peng generates revenue principally through e-commerce sales of healthcare-related products aimed at promoting healthy lifestyles among Chinese consumers. The company operates two proprietary digital platforms: King Eagle Mall and the Kun Zhi Jian Mini Program [S1][S4]. These channels offer a diversified range including physiotherapy equipment, preventive healthcare goods like nutritional supplements and diet aids, as well as household items connected to wellness.

Revenue streams bifurcate between pure retail sales via these online platforms and equipment-based service revenue—covering prepaid card activation fees plus technical support fees linked to physiotherapy devices [S6]. Notably, Kun Peng has discontinued several service lines following deregistration of certain subsidiaries to streamline operations [S5]. End customers predominantly reside in China, accessed through subsidiaries structured via a Variable Interest Entity (VIE) framework which facilitates compliance with foreign investment restrictions while enabling consolidated reporting [S1][S23].

Pricing power is limited by fragile consumer demand amid China's broader economic uncertainty impacting consumption patterns [S6]. Moreover, product mix shifts influence gross margins; higher-margin physiotherapy equipment services somewhat offset depressed retail margins but overall margin contraction is evident compared to prior periods [S6]. Platform engagement quality drives customer retention and purchasing frequency — key metrics underpinning revenue volume.

Industry Context: Competitive Pressures from Dominant Chinese Social E-Commerce Platforms

Kun Peng operates within a fiercely competitive Chinese social commerce landscape dominated by large-scale players such as Pinduoduo (known for group buying models), Taobao (Alibaba’s flagship marketplace), JD.com, and emerging specialty platforms [S7]. These incumbents benefit from superior scale economics, brand recognition, extensive product assortments, advanced app functionalities, and robust user bases.

Compared to such giants, Kun Peng's competitive position is challenged by its relatively modest member base size and brand presence. Customer loyalty hinges heavily on app usability enhancements, service reliability, and marketing efficacy—all areas where competitors continuously innovate [S7]. Member acquisition cost pressures persist amid saturation effects in China's e-commerce sector.

While Kun Peng leverages proprietary platforms focused exclusively on health-related offerings that add some differentiation versus broad generalist marketplaces, cross-platform switching costs remain low for price-sensitive consumers in this segment. Sustained marketing investment is essential just to maintain visibility amid advertising noise pressure.

Sector-Specific Operational Realities: VIE Structure and Regulatory Complexities

Operating through a VIE structure introduces distinct operational risks tied to regulatory ambiguities between U.S. listing requirements and PRC statutes. This framework enables control over PRC operating entities despite foreign ownership restrictions by using contractual arrangements rather than equity ownership [S1][S23].

However, such arrangements face legal enforceability uncertainties under evolving PRC laws. External risk factors have intensified given increased scrutiny of China-based VIE companies by U.S. regulators under statutes like the Holding Foreign Companies Accountable Act (HFCAA). Although Kun Peng’s independent auditor is PCAOB-registered in Malaysia rather than China mainland—currently mitigating direct audit-related delisting risks—potential future regulatory shifts pose material threats including forced delisting or operational constraints [S1].

Furthermore, cross-border fund transfer mechanisms embedded within the VIE schema can be impaired by PRC government interventions restricting capital flow between subsidiaries and ultimate parent entity. This situation may undermine efficient liquidity management for Kun Peng's global corporate structure [S1][S16]

Growth Drivers: Platform Enhancements, Member Expansion, and Product Diversification

Despite headwinds, Kun Peng pursues measured growth strategies centered on upgrading its digital platform features to improve user experience and engagement metrics via King Eagle Mall and Kun Zhi Jian Mini Program [S7][S20]. Enhancements aim at smoother navigation workflows and expanded health care product offerings designed to boost purchase frequency.

The company emphasizes expanding its paying subscriber base through targeted marketing campaigns highlighting preventive health benefits linked to its physiotherapy apparatus [S7]. Customer service quality improvements are also vital parts of the retention strategy given relatively low switching barriers.

On the product side, diversification into dietetic advice services alongside existing physiotherapy equipment attempts to deepen wallet share per customer while appealing to growing health-conscious demographics in China [S7][S20]. However growth remains tactical rather than transformative due to structural competition limits imposed by dominant social commerce platforms.

Risks and Constraints: Liquidity, Regulatory Environment, and Competition

Coupled with ongoing net losses reflecting underwhelming top-line traction and high fixed overheads in platform maintenance plus marketing expenditure [F1], this introduces credible going concern doubts explicitly highlighted in prior annual disclosures [S1][S14]. The company depends on shareholder loans or external financing sources that may not materialize under adverse capital market conditions or investor sentiment deteriorations.

Regulatory uncertainty stemming from China-U.S. geopolitical tensions present additional constraint risks — notably potential audit-related delisting threats under HFCAA or sudden enforcement changes affecting VIE contract validity [S1]. Such scenarios might necessitate restructuring costly enough to destabilize ongoing business operations.

Market competition sharply compresses pricing power outside niche product verticals [S7]. Larger peer platforms enjoy economies of scale in logistics fulfillment costs not replicable easily by Kun Peng’s smaller distribution footprint limiting margin elasticity

Upcoming Catalysts and Execution Metrics to Monitor

Key performance indicators that will serve as barometers of operational progress include:

- Sequential quarterly revenue trajectories post Q1 2026 filing highlighting recovery or further deterioration trends;

- Monthly active user counts alongside paying member growth rates reflecting platform adoption strength;

- Regulatory developments clarifying the status or enforcement of VIE contractual frameworks impacting cross-border activity;

- Any announced refinancing or capital injection events addressing urgent liquidity shortfall;

- Public disclosures concerning incremental app functionality rollouts or product category expansions signaling execution momentum. Monitoring these milestones will provide critical insight into whether Kun Peng can stabilize its financial position while capturing incremental structural growth in China’s competitive online health care segment.

Brief Financial Profile Summary

As of March 31, 2026, Kun Peng held cash & equivalents of approximately $19,768 against current liabilities north of $9.68 million resulting in a dangerously low current ratio around 0.04 indicating extreme short-term liquidity stress [F1][S2]. Latest available annual data as of September 30, 2025 showed operating losses surpassing $1.77 million with net losses over $1.26 million reinforcing persistent unprofitability challenges [F1][S1]. This scenario underscores an urgent imperative for capital raising or transformational cost reduction initiatives to preserve going concern viability.

This analysis reflects a synthesis of audited filings up to May 2026 without speculation beyond documented disclosures. It aims solely at evaluating operational dynamics within industry context—not advising investment actions.

Financial position in context

As of 2026-03-31, companyfacts shows $19,768 in cash and equivalents [F1]. Current assets of $341,092 and current liabilities of approximately $9.68 million imply a current ratio near 0.04x for 2026-03-31 [F1].

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments