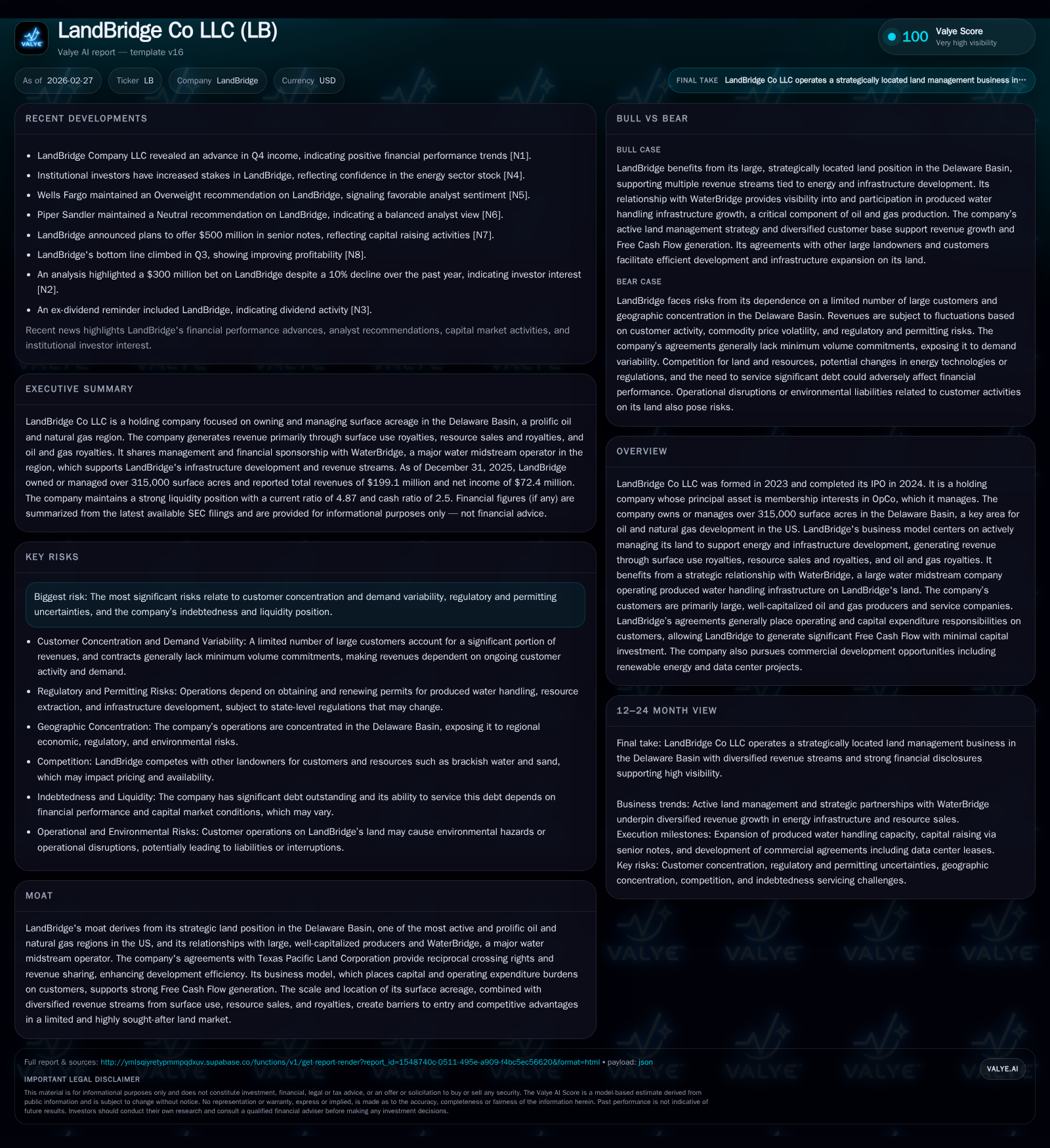

LandBridge Co LLC Expands Free Cash Flow Through Strategic Delaware Basin Land Management

LandBridge leverages its prime surface acreage and partnerships to generate diversified revenues with minimal capital outlay amid industry volatility.

Founded in 2023 and public since mid-2024, LandBridge Co LLC owns and manages over 315,000 surface acres centrally located in the prolific Delaware Basin. The company’s revenue model is grounded in surface use royalties, resource sales, and oil and gas royalties, with a distinct emphasis on placing capital and operational burdens on its customers. This approach has fueled substantial growth in operating income and cash flow in 2025. Critical to its ecosystem is a synergistic relationship with WaterBridge, a leading water midstream operator. However, LandBridge’s financial profile reflects concentration risks and leverage constraints tied to industry cyclicality and geographic focus within the Permian Basin.

Company Background and Business Model

LandBridge Co LLC was established in late 2023 as a holding entity focused exclusively on capturing value from surface land assets critical for energy development. It completed its IPO in mid-2024, positioning itself publicly as a land management firm with a unique operational focus.

The company currently controls over 315,000 surface acres concentrated predominantly along the Texas-New Mexico border within the heart of the Delaware Basin—a prolific sub-region of the larger Permian Basin known for extensive oil and natural gas production [S1]. Unlike exploration & production (E&P) companies, LandBridge does not engage directly in hydrocarbon extraction but rather provides essential surface rights under agreements that shift operating costs to lessees.

Revenue streams derive primarily from three categories: surface use royalties and revenues (approximately 68% of total), resource sales including brackish water and caliche (about 24%), and oil & gas royalties (~6%) from mineral interests underlying roughly 4,400 gross mineral acres [S20][S12]. This diversified base helps mitigate reliance on any single income source while capitalizing on growing activity in the basin.

Historical Performance and Financial Growth Drivers

From a nascent entity during formation and IPO phases through 2023-2024, LandBridge's financial trajectory has been notably upward:

Historical performance (annual)

| FY | Net ($mm) | CFO ($mm) | OpInc ($mm) | Capex ($mm) | Net YoY |

|---|---|---|---|---|---|

| 2025 | 30 | 126 | 119 | 4 | +489.6% |

| 2024 | 5 | 68 | -17 | 1 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | FCF ($mm) | ROE% |

|---|---|---|

| 2025 | 122 | 8.9 |

| 2024 | 67 | 1.2 |

Source: SEC companyfacts cache [F1].

The dramatic earnings turnaround from an operating loss in 2024 to strong positive income indicates effective scaling of contract execution and asset monetization post-IPO [F1]. Net income similarly turned positive with $30.1 million recorded at end-2025.

Cash flows from operations nearly doubled year-over-year reaching $126 million by 2025 driven by expanding surface rental agreements (SURAs), resource extraction contracts, and synergies from WaterBridge operations [F1][S14]. Capital expenditures remain modest relative to cash flow generation due to the company’s strategy of transferring investment burden onto customers.

A pivotal growth catalyst has been the acquisition of strategic acreage including the notable "1918 Ranch," expanding scale though requiring higher upfront capital investments which management approved with debt financing support [S14][S15].

Future Growth Prospects

The company envisions sustaining long-term growth via four main levers:

- Continued expansion of acreage under active management combined with selective acquisitions enhancing footprint quality.

- Increasing penetration of non-traditional energy sectors such as solar power generation, energy storage facilities, digital infrastructure, and emerging uses like cryptocurrency mining leveraged by versatile land assets.

- Strengthening relationships with large-cap E&P producers who are key beneficiaries of WaterBridge's water infrastructure coupled with LandBridge’s surface management expertise drives recurring volume.

- Proactive contract negotiations embedding inflation-adjusted fee structures while broadening fee-based services beyond traditional energy-centric operators [N1][S12][S15].

However, growth is tempered by several constraints including:

- Customer concentration risk where top five clients represent nearly 60% of revenues, raising sensitivity to shifts in their capital spending patterns or credit conditions [S10].

- Market demand dependence tied closely to commodity price cycles impacting drilling activity which drives land use.

- Environmental regulatory developments could impede operations or impose liability risks given joint responsibility on leased properties [S19][S21].[F1]

- Supply chain disruptions affecting customers’ ability to deploy equipment or complete projects could further dampen revenue visibility [S24].

Forecasts, Guidance & Milestones to Monitor

While explicit forward-looking guidance is limited publicly, key milestones include:

- Monitoring WaterBridge capacity utilizations which directly correlate with royalty volume growth potential on produced water handling systems mounted on LandBridge acreage.

- Anticipating renewal rates and inflation escalators effectiveness within SURAs impacting recurring revenue stability.

- Tracking incremental contributions from commercial ventures branching beyond core hydrocarbon services into renewables or data center infrastructure development with partners such as Powered Land Partners (PowLan).

- Debt covenant adherence amid ongoing debt amortization schedules offers insight into possible adjustments in capital allocation or refinancing initiatives [S9][S27].

Analysts should watch quarterly filings for developments on acreage expansion deals or restructuring that may influence leverage ratios or liquidity metrics.

Returns & Capital Allocation

LandBridge demonstrates strong operational cash generation ability relative to its net income profile:

- Operating cash flow hit $126 million in fiscal 2025 versus net income of around $30 million indicating robust non-cash adjustments typical of asset-heavy entities or share-based compensation factors detailed in reports [F1][S14].

- Free Cash Flow after minimal capital expenditure was approximately $122 million for 2025 accentuating low-investment intensity business model benefits.

- Equity as of end-2025 stood near $340 million resulting in an estimated return on equity around 8.9%, supported by efficient asset utilization though impacted by share-based compensation expenses [F1].

The company's debt load—about $570 million—is manageable under current covenant structures but represents a significant factor affecting financial flexibility given interest expense levels near $20 million annually leading into 2026 [S13][S18]. Management’s conservative approach enforces leverage limits tied to EBITDA calculations while permitting restricted payments such as dividends or buybacks contingent upon meeting coverage ratios [S7][S28]. However:

- The company currently does not disclose regular dividends nor aggressive buyback plans but retains authorized share repurchase programs that may be opportunistically executed depending on market conditions [S9].

Industry Positioning & Competitive Moat

LandBridge’s principal competitive advantage roots deeply in its premier geographic position within the Delaware Basin—arguably the most prolific oil & gas basin driving US production growth—and ownership scale surpassing most private landholders relevant for industrial development.

Moreover, symbiotic intra-group connections with WaterBridge midstream business afford distinct insight into production trends and infrastructural pipeline expansions enhancing revenue predictability through joint land-use contracts.

Reciprocal crossing rights arrangements with adjacent landowners like Texas Pacific Land Corporation further advance operational efficiencies facilitating developers’ site access while diversifying revenue sharing relationships.

Nonetheless:

- The company contends with competition from other regional landowners vying for a share of limited resource extraction rosters particularly sand and brackish water supplies essential for well completions.

- Emerging demand sectors such as renewables impose novel regulatory compliance dynamics alongside established fossil fuel activities illustrating evolving operational landscapes faced by LandBridge's management teams [S11][S25].

Key Risks Summary

Risks detailed primarily hinge on external factors largely outside direct control:

- Volatility inherent in commodity markets fundamentally shapes demand-side activity where downturns could abruptly curtail drilling rig counts lowering revenue from surface use fees or resource royalties.

- Geographic concentration concentrated solely within Texas-New Mexico bounds increases exposure to regional disruptions such as weather events or state regulatory policy changes impacting operators’ activity timelines.

- Substantial debt holding introduces refinancing risk particularly if interest rate environments worsen or credit market conditions tighten unexpectedly influencing cost of capital access.[F1][S19]

- Customer diversification remains an ongoing challenge; tight client bases raise dependencies potentially limiting bargaining leverage or cash flow consistency when contract renewals come due.

Conclusion

In under three years since inception, LandBridge Co LLC has accelerated from startup phases toward scaled profitability through shrewd acreage management centered on one of North America’s foremost petroleum basins. The firm’s unique partnership symbiosis combined with minimal capital outlays by leveraging customer investment obligations yields near-term free cash flow strength bolstered by rising operating income margins.

Looking forward, sustainable growth will require deft navigation of commodity price cycles coupled with broadening revenue sources within emergent infrastructure markets while prudently managing financial leverage constraints under evolving industry headwinds.

Disclaimer: This analysis is based exclusively on publicly available information from SEC filings and news reports as of February 27, 2026. It does not constitute investment advice or recommendations regarding acquisition or disposition of securities related to LandBridge Co LLC.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments