Lear Corp Advances Electrification with Q1 Momentum and Solid Outlook

Lear’s Q1 2026 results highlight progress in electrical systems for electrified vehicles alongside reaffirmed full-year guidance.

Lear Corporation’s latest quarterly filing reveals strategic expansion in electrified powertrain components driving near-term operational momentum. The company is leveraging its Seating and Electrical Systems segments to capture growth amid industry shifts toward EVs, supported by longstanding OEM partnerships and technical scale. While cyclical automotive market factors and supply chain constraints remain risks, Lear maintains a stable financial position with covenant compliance as it advances product relevance and customer penetration. Upcoming milestones include monitoring EV program wins and next-quarter demand signals.

Q1 2026 Operating Highlights and Strategic Shifts

In its most recent quarterly report for the period ending April 4, 2026 [S2], Lear Corporation highlights key operational developments that reflect a strategic pivot towards components supporting electrified powertrains. The Electrical Systems segment has expanded its product scope beyond traditional internal combustion engine (ICE) reliance to integrate portfolio offerings such as wire harnesses, terminals, connectors, and notably key high-voltage battery connection systems. These high-voltage components—comprising intercell connect boards, bus bars, and main battery interface systems—address the critical need for managing higher voltage and power demands intrinsic to hybrid electric vehicles (HEVs), plug-in hybrids (PHEVs), and battery electric vehicles (BEVs) [S2].

The company’s reaffirmation of its full-year 2026 financial outlook in the May 1 press release [S3] suggests strong confidence in executing this transition amidst persistent automotive market challenges. Operating results indicate continued integration of electrification-focused technologies within customer vehicle platforms, underpinning stable revenue mix progress relative to prior periods [N1]. This quarterly update sets a foundation for understanding how Lear is positioning itself operationally at the intersection of automotive legacy systems and emergent electric mobility demands.

Business Model and Product Portfolio Insights

Lear operates principally through two reportable segments: Seating and Electrical Systems (E-Systems), each catering to global original equipment manufacturers (OEMs) with tailored solutions that reflect evolving vehicle design trends [S1]. The Seating division delivers advanced occupant seating assemblies recognized for ergonomic innovation and manufacturing scale optimized for passenger cars, SUVs, trucks, and commercial vehicles. These offerings generate steady contractual revenue tied to vehicle production volumes.

E-Systems encompasses a diverse array of electrical distribution products including complex wiring harnesses that act as critical nervous system pathways within automobiles, connectors that ensure reliable electrical signal transmission, as well as engineered components serving specialized electrification needs [S1]. Importantly, the inclusion of high-voltage battery connection systems reflects a strategic extension into electrification-relevant domains where technical complexity confers higher switching costs for OEMs.

The business model relies heavily on collaborative design engagement with automakers during vehicle development cycles, supporting long-term contractual relationships. Pricing typically accounts for volume-based scale advantages but faces ongoing pressure from tier-1 peers competing on global cost structures. Lear’s emphasis on quality engineering coupled with scalable operations builds defensibility especially where product reliability is paramount given increasingly sophisticated safety standards governing automotive electrical systems [S1].

Competitive Position within the Automotive Supplier Industry

Lear commands a competitive position within tier-1 automotive suppliers known for seating systems and electrical distribution. The highly concentrated OEM customer base increases buyer dependence dynamics but also rewards dependable supply performance across regions including North America, Europe, and Asia [S1]. Competitors vary across product lines—seating faces challengers like Adient while electrical systems contend with firms such as Delphi Technologies or Aptiv—each vying for share amid technological shifts.

Market competition centers on areas like pricing negotiation leverage, ability to rapidly adapt designs to changing platform architectures, regulatory certification compliance for safety-critical components, and geographic footprint efficiency. Lear’s sustained investment in R&D targeting EV-specific electrical architectures grants it partial differentiation by addressing higher voltage interconnectivity requirements increasingly mandated by automakers [S1]. However, supplier tiering norms mean OEMs often play suppliers against each other on cost which can cap margin expansion even as volumes grow.

Capacity constraints at assembly plants or raw material sourcing bottlenecks may limit ability to ramp production quickly during peak vehicle launches. Regulatory changes related to vehicle safety standards or materials compliance pose additional hurdles requiring agile certification processes. Lear’s global supply chain must also weather geopolitical uncertainties affecting component availability.

Growth Drivers: Electrification and Client Partnerships

Structural growth drivers center on accelerating automotive electrification trends creating heightened demand for robust electrical distribution innovations. With global automakers committed to expanding their EV portfolios over the next decade, wiring harnesses capable of safely managing higher voltage systems become mission-critical [S2]. Lear’s expansion into intercell connect boards and main battery connectors taps directly into this growth vector.

Beyond product innovation, deep-rooted client relationships facilitate inclusion in new EV platform programs providing scalable volume growth opportunities [N4]. OEMs tend to favor proven suppliers who combine technical expertise with flexible manufacturing footprints enabling multi-region rollout support. Such strategic partnerships help lock in order books ahead of production ramps.

Additionally, product diversification through integrated seating solutions complemented by evolving tech-enabled features such as smart seating controls or modular designs may sustain revenue stability independent of pure electrification cycles [S1]. Success in winning new contracts on emerging vehicle models or increasing content per vehicle can yield meaningful top-line contributions over subsequent quarters.

Risks and Constraints: Cyclicality, Supply Chain, and Competition

Lear faces inherent cyclical risk characteristic of automotive suppliers where global light vehicle production fluctuations strongly impact order volumes [S6]. Downturns compress margins via fixed cost absorption challenges while prolonged production delays or inventory imbalances strain working capital management.

Supply chain volatility remains a substantial constraint; raw material price inflation—copper for wiring harnesses or specialty plastics used in connectors—can erode margins absent swift pass-through pricing mechanisms [S2]. Furthermore, semiconductor shortages or transportation disruptions have episodically curtailed OEM production cadence leading to order deferrals.

Competition from both established multinational suppliers seeking share gains along with emerging regional players applying aggressive pricing strategies requires continuous investment in technology differentiation plus cost optimization initiatives. Failure to secure breakthrough electrification contracts or loss of preferred supplier status could impede growth momentum [S6].

Key Upcoming Milestones and Market Signals

Investors should monitor forthcoming quarterly earnings releases where management updates on program wins/losses will provide critical insight into product adoption trajectory within electrified powertrain categories [S3]. Particularly valuable will be commentary concerning backlog status across Seating and E-Systems segments alongside any adjustment in pricing environment due to raw material cost pressures or OEM renegotiations.

Broader industry EV rollout schedules function as indirect leading indicators; acceleration among key OEM clients correlates with demand spikes for Lear’s high-voltage connection products. Any announcements related to new platform launches incorporating advanced seat integration or upgraded wiring harness architectures could portend step-up volume growth.

Technological milestones such as successful launch of next-generation battery connection solutions or weight reduction initiatives enhancing overall system efficiency represent execution points underscoring competitive relevance going forward.

Latest Financial Snapshot: Liquidity, Leverage, and Capital Structure

Latest financial snapshot

| Metric | Value | Period |

|---|---|---|

| Cash & equivalents | $882mm | |

| 2026-04-04 | ||

| Current assets | $8.3bn | |

| 2026-04-04 | ||

| Current liabilities | $6.2bn | |

| 2026-04-04 | ||

| Current ratio | 1.33x | |

| 2026-04-04 |

Source: SEC companyfacts cache [F1].

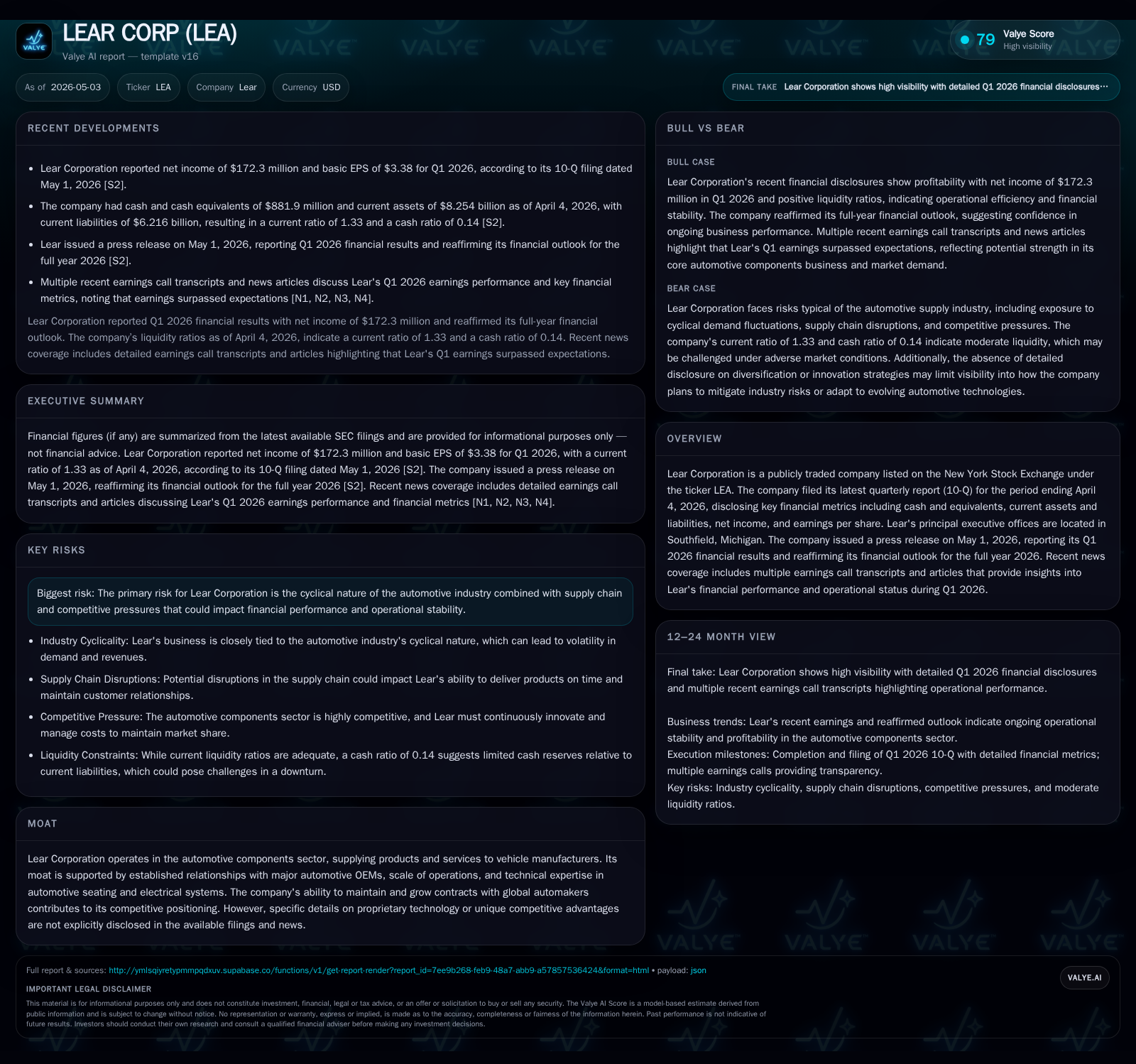

At quarter end April 4, 2026, Lear reported cash and cash equivalents totaling $881.9 million alongside current assets aggregating $8.254 billion versus current liabilities of $6.216 billion yielding a current ratio near 1.33 indicative of adequate short-term liquidity capacity [S2][F1].

The company maintains an unsecured delayed-draw term loan facility balance of $50 million maturing September 30, 2027 with full covenant compliance affirmed under its Credit Agreement reducing refinancing risk near term [S2].

| Metric | Amount (USD Millions) |

|---|---|

| Cash & Equivalents | 881.9 |

| Current Assets | 8,254.0 |

| Current Liabilities | 6,215.8 |

This analysis synthesizes audited SEC filings through May 2026 alongside contemporaneous earnings call insights without projecting future stock performance or providing investment recommendations. Readers should consult primary source documents for detailed disclosures.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments