Repay Holdings Refines Payment Platform Amid Q1 2026 Operational Shifts

Q1 results show modest revenue decline and net loss while Repay advances acquisitions and technology investments.

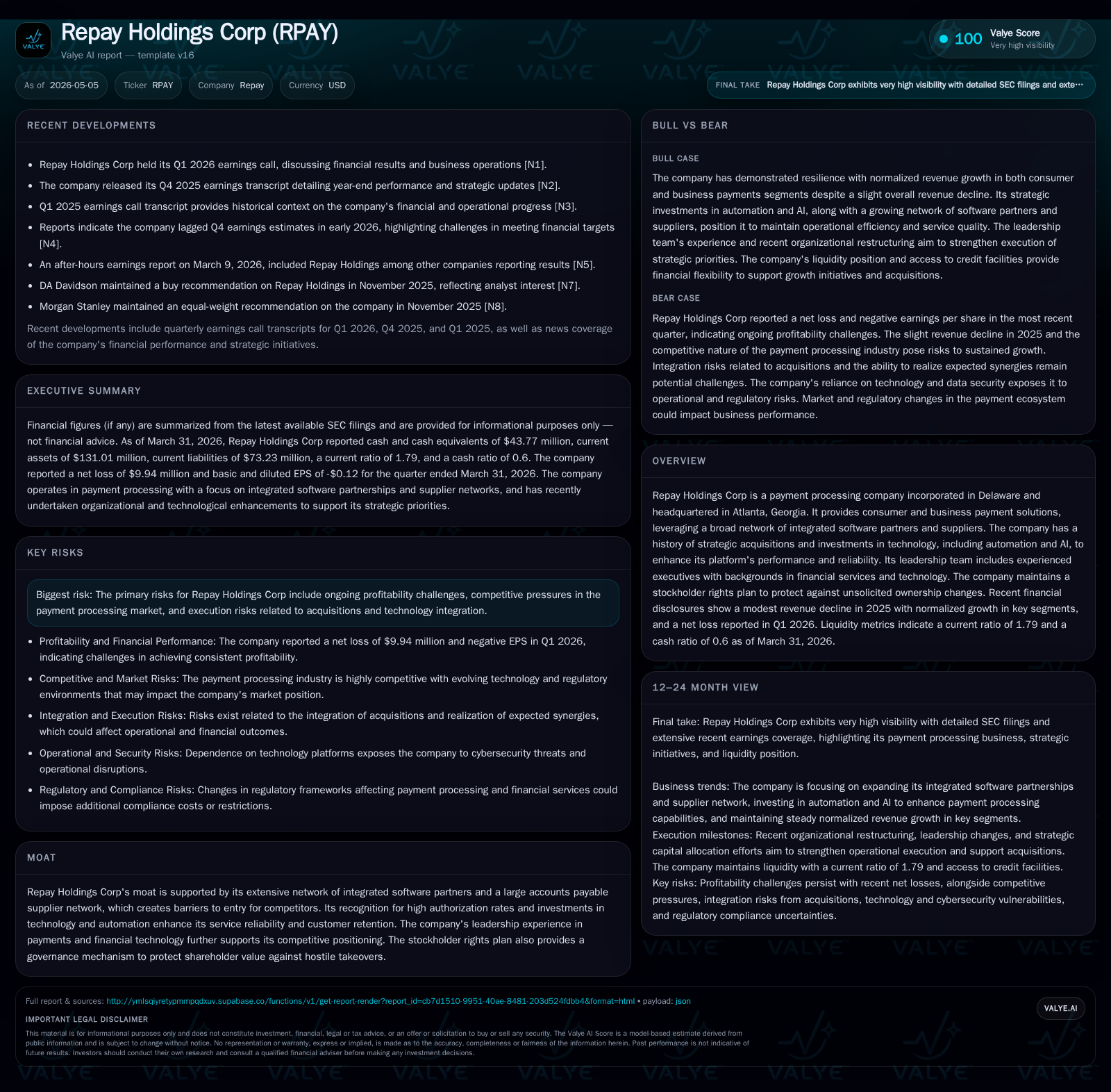

Repay Holdings Corp reported a net loss in Q1 2026 alongside a slight revenue dip, reflecting ongoing challenges in profitability. The company is actively integrating its sizable KUBRA acquisition and advancing automation and AI initiatives to enhance its payment processing platform. Its competitive moat relies on a broad ecosystem of software partnerships and supplier networks that bolster authorization rates and customer retention. Near-term growth hinges on scaling payment volume, achieving synergy from acquisitions, and platform modernization amidst competitive market pressures and profitability headwinds.

Q1 2026 Operational Update and Implications

In the quarter ended March 31, 2026, Repay Holdings Corp reported a continuation of its net loss trajectory alongside a modest decline in revenue trends [S2][S3]. While explicit revenue figures for Q1 have not been disclosed in the provided excerpts, the company reiterated ongoing investment in strategic initiatives that are absorbing near-term profitability. Notably, liquidity remains sufficient with a current ratio of 1.79 and cash plus equivalents around $43.8 million as of quarter-end [F1], providing runway for continued operational shifts.

A material event in this period is Repay's pending acquisition of KUBRA Holdings Inc., valued at approximately $372 million with an expected close in Q2 2026 [S6][S25]. This deal is financed through a combination of existing cash reserves and committed debt facilities totaling up to $600 million, including term loans and revolving credit lines arranged with Truist Bank [S25]. Successful closing and seamless integration of KUBRA are critical near-term milestones to expand Repay’s product suite and client base.

The company also completed governance enhancements with the adoption of a stockholder rights plan designed as an anti-takeover measure [S27][S28], indicating management’s intent to maintain strategic control during this transformative phase.

Repay’s Business Model and Payment Ecosystem Integration

REPAY operates primarily as a payment processing company serving both consumer-facing clients and business customers through an extensive network of integrated software partners covering diverse verticals [S1]. Its platform aggregates payment acceptance capabilities facilitated by partnerships across software providers who embed REPAY’s payment solutions within their own offerings. This model generates transaction fees linked directly to payment volume processed.

The backbone of Repay’s competitive advantage is its high authorization rates—an indicator of transaction success—and a large supplier network managing accounts payable transactions that create implicit switching costs for clients [S1]. Recent filings highlight continued rollout of new product capabilities leveraging automation and AI technologies intended to bolster performance reliability and scalability [S1]. These enhancements aim to reduce manual processes while improving client retention through a more seamless experience.

Revenue growth mechanics revolve around increases in transaction volume driven by partner onboarding and expansion into new verticals or geographies, combined with stable or improving pricing metrics tied to service tiers or transaction types. Subscription or recurring fees may also supplement this mix but remain secondary to transactional drivers.

Competitive Position in the Payment Processing Industry

The payments industry is notably fragmented yet intensely competitive, dominated by players ranging from large-scale incumbents to nimble fintech challengers [S1][N5]. In this environment, Repay positions itself via deep integration within software ecosystems rather than stand-alone end-customer sales—that integration serves both as a distribution moat and switching-cost mechanism.

The company’s emphasis on high authorization success rates supports client loyalty amid tight margins. The company must regularly update compliance postures aligned with evolving regulation as well as maintain technological relevance through continuous investments.

Scale achieved through acquisitions like KUBRA contributes critically to supporting necessary infrastructure investments while widening geographic reach. However, margin pressure persists until such acquisitions yield full synergy realization.

Drivers Supporting Future Growth Prospects

Growth levers for Repay include the anticipated closing and integration of the KUBRA acquisition which should expand its customer base and payment product portfolio [S6][S25].

Additionally, internal initiatives focusing on automation deployment aim at reducing operational costs per transaction enhancing potential profitability without compromising service quality [S1]. The company also targets expanding payment volume by growing its network effect: onboarding new software partners who can channel more transactions through REPAY’s platform.

Incremental product enhancements unveiled recently are designed for future-scale readiness, signaling efforts to capture more wallet share within existing clients while attracting new ones seeking modern payment technologies [S3]. Monitoring KPIs such as booking rates from partners, renewal rates, average transaction size, and platform uptime will be crucial indicators.

Risks and Constraints Impacting Execute and Profitability

Financially, REPAY continues grappling with sustained net losses reflecting high investment levels coupled with competitive pricing pressure [S2][F1]. Execution risk is non-trivial given complexities inherent in large-scale integrations like KUBRA coupled with platform modernization efforts involving automation/AI initiatives which carry potential technical pitfalls or delayed ROI realization.

Market competition intensifies margin compression risk alongside regulatory changes that might alter allowable fee structures or introduce compliance cost escalations. Dependency on third-party software partners also exposes REPAY to concentration risks whereby loss of key partners could significantly impact volume flow.

Liquidity appears adequate currently; however, debt levels totaling nearly $398 million generate financial leverage considerations warranting vigilance especially if operating losses persist [F1]. The stockholder rights plan adopted signals management’s awareness of shareholder value preservation amid speculative takeover interest.[S27]

Key Upcoming Milestones and Investor Watchpoints

Investors should track the expected closing timeline for the KUBRA acquisition in Q2 2026 along with subsequent integration progress reports detailed in upcoming quarterly disclosures or investor presentations [S25][S3]. Progress metrics around synergy realization—including cost saves or cross-selling effectiveness—will be critical for margin improvement narratives.

Platform performance improvements from automation/AI rollouts merit attention for their impact on service reliability KPIs such as authorization rates or system uptime reported periodically [N1]. Similarly, announcements concerning new partner additions or expanded vertical penetration would provide tangible demand signals.

Management commentary during earnings calls will illuminate strategic priorities adjustment given evolving macroeconomic factors or industry dynamics potentially influencing guidance updates beyond Q2.

Latest Financial Snapshot: Liquidity and Leverage Profile

Latest financial snapshot

| Metric | Value | Period |

|---|---|---|

| Cash & equivalents | $44mm | |

| 2026-03-31 | ||

| Total debt | $398mm | |

| 2026-03-31 | ||

| Net debt | $354mm | |

| 2026-03-31 | ||

| Current assets | $131mm | |

| 2026-03-31 | ||

| Current liabilities | $73mm | |

| 2026-03-31 | ||

| Current ratio | 1.79x | |

| 2026-03-31 |

Source: SEC companyfacts cache [F1].

| Metric | Value (USD million) |

|---|---|

| Cash & Equivalents | 43.77 |

| Total Debt | 397.50 |

| Net Debt | 353.73 |

| Current Assets | 131.01 |

| Current Liabilities | 73.23 |

| Current Ratio | 1.79 |

As of March 31, 2026, Repay held $43.8 million in cash against $398 million in total debt resulting in net leverage approximating $354 million [F1]. Current assets adequately cover short-term liabilities with a current ratio near 1.8 indicating reasonable liquidity buffers despite operating losses [F1][S2]. Sustained profitability improvements will be necessary to support deleveraging efforts over time.

Disclaimer

This analysis is based solely on publicly available information as of May 5, 2026. It does not constitute investment advice or recommendations. Readers should conduct their own due diligence before making any decisions related to securities mentioned herein.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments