Merck's Q1 2026 Transition Highlights Acquisition Impact and Pipeline Expansion

Merck reports a notable Q1 loss driven by acquisition expenses while advancing oncology and antiviral pipelines through strategic deals.

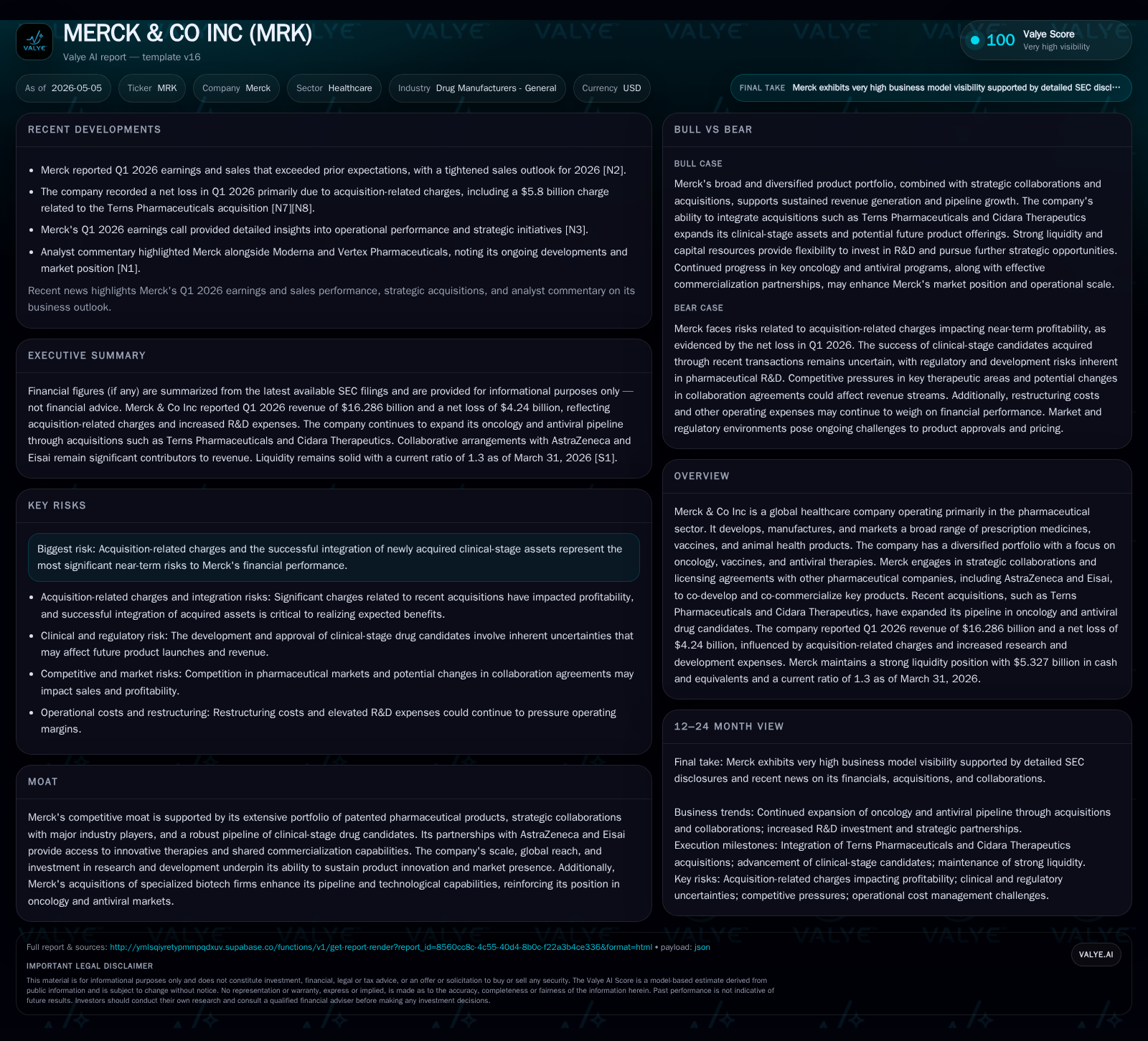

Merck’s first quarter of 2026 shows revenue growth to $16.3 billion but a net loss of $4.24 billion largely due to significant acquisition-related charges. The company’s recent acquisitions of Terns Pharmaceuticals and Cidara Therapeutics enhance its clinical pipeline, particularly in oncology and antiviral sectors. Strategic collaborations with AstraZeneca and Eisai continue to underpin revenue streams. Going forward, Merck’s growth will hinge on successful integration of new assets, regulatory approvals, and sustained innovation in core therapeutic areas.

Recent Operating Update: Q1 2026 Highlights

Merck & Co., Inc.'s latest quarterly report underscores a complex operating environment shaped by transformative corporate actions. For Q1 ended March 31, 2026, Merck posted revenues of $16.286 billion, topping analyst expectations and reflecting robust sales across its pharmaceutical portfolio [S3][S2]. However, this positive topline was overshadowed by a net loss of approximately $4.24 billion, primarily attributable to substantial acquisition-related research and development charges worth over $17 billion collectively from the purchases of Terns Pharmaceuticals in March 2026 (expected $5.8 billion charge) and Cidara Therapeutics in January 2026 (recorded $9 billion charge) [S2][S5][S7].

Alongside these acquisitions, Merck entered into a funding deal with Blackstone Life Sciences whereby Blackstone will pay Merck a non-refundable $700 million in Q4 2026 to subsidize development costs for sacituzumab tirumotecan (sac-TMT), an investigational oncology asset currently in clinical development [S2]. This upfront investment helps offset R&D expenses while enabling advanced trials for sac-TMT.

Business Model: Revenue Mechanics and Strategic Positioning

Merck operates as a diversified healthcare company focused primarily on pharmaceuticals, vaccines, and animal health products. The business generates revenues through product sales worldwide, licensing agreements, milestone payments from collaborations, and royalties. Major products such as Keytruda (oncology immunotherapy), Lynparza (oncology co-developed with AstraZeneca), Koselugo (a pediatric oncology therapy), Gardasil (HPV vaccine), and antiviral agents including Lagevrio form the backbone of the commercial portfolio.

Revenues flow as hospitals, healthcare providers, governments, distributors, and pharmacies purchase prescription medicines or vaccines based on demand influenced by disease prevalence, treatment guidelines, regulatory approvals, pricing strategies, reimbursement environments, and competitive dynamics. Collaborations bring milestone recognition linked to regulatory achievements or sales thresholds; for example, Merck shares profits or pays royalties under co-development deals with players like AstraZeneca.

Acquisition strategy is pivotal for future-proofing growth – illustrated by the large spending on Terns’ allosteric BCR::ABL1 tyrosine kinase inhibitor candidate targeting resistant chronic myeloid leukemia and Cidara’s long-acting antiviral MK-1406 catering to influenza high-risk populations [S5][S7]. These add clinical-stage pipelines complementary to internal R&D.

Financially significant intangible assets linked to products like Lynparza ($762 million) are amortized over expected useful lives supported by forecasted cash flows through roughly 2028-29 periods [S2]. This accounting reflects underlying confidence in legacy product franchises providing medium-term revenue streams.

Industry Structure and Competitive Position

Merck is positioned among top global pharmaceutical firms competing intensely in specialty therapeutics—especially oncology—and antiviral markets that feature rapid innovation cycles and heavy R&D investment requirements. The sector demands continuous breakthroughs due to patent expirations, evolving treatment protocols, price pressures from generic entrants or biosimilars, pricing negotiations in numerous jurisdictions, and increasing emphasis on real-world evidence supporting therapy value.

Collaborative networks serve as essential enablers; Merck's alliances amplify resource sharing for co-development/commercialization risks while extending market access globally. The firm’s scale affords broad manufacturing capabilities and distribution reach but sustains high fixed costs making operational efficiency critical.

Cancer therapeutics form the core growth battleground alongside vaccines amid high unmet medical needs. Competition includes other industry giants like Pfizer/BioNTech in vaccines or Bristol Myers Squibb in immuno-oncology plus emerging biotech innovators that challenge incumbents via novel modalities or differentiated mechanisms.

Growth Drivers

Pipeline Expansion & Acquisitions

The acquisitions of Terns Pharmaceuticals ($6.7 billion tender offer underway targeting May closure) and Cidara Therapeutics ($9.2 billion completed early 2026) reinforce Merck’s commitment to bolstering promising late-stage candidates focused on high-growth oncology subsegments and respiratory infections respectively [S5][S7]. The pipeline diversification into oral allosteric BCR::ABL1 inhibitors addresses resistance issues unmet by existing treatments potentially securing market niches if clinical data prove favorable.

Commercial Portfolio Momentum

Keytruda remains a pillar with expanding indications across multiple tumor types driving continued uptake despite growing competition [S23]. Vaccines like Gardasil sustain demand trends benefiting from childhood immunization programs globally.

Collaborations & Milestones

Funding partnerships such as with Blackstone reduce capital outlay risk while facilitating advanced clinical trials (e.g., sac-TMT). Revenue-sharing deals help manage upfront development cost burdens offering financial flexibility.

Geographic & Segment Diversification

Merck's global footprint shields somewhat against region-specific regulatory or pricing headwinds; varied product segments including animal health provide cyclical buffers amid pharmaceutical patent cliffs.

Risks / Watchpoints / Growth Constraints

Integration Costs & R&D Expense Volatility

High acquisition-related charges depress near-term profitability; integration success hinges on operational synergies realization without disrupting ongoing projects or commercial efforts [S2]. Research expense acceleration may pressure margins until assets reach commercial phases.

Regulatory & Reimbursement Uncertainty

Clinical trial outcomes are binary inflection points that could delay or halt product launches impacting expected revenue streams especially for novel compounds like TERN-701 or MK-1406. Price controls or reimbursement cutbacks globally pose persistent challenges affecting volume growth potential.

Competitive Pressures & Patent Expirations

Rival therapies’ launch timing can erode market share while generic competition may compress legacy product lifecycles requiring continuous innovation.

Balance Sheet Leverage From Acquisitions

Although liquidity remains healthy with over $5 billion cash on hand [F1][S2], total debt elevated from acquisition financing generates net debt exceeding $12 billion implicating leverage considerations if further borrowing is needed before asset monetization ramps up.

What To Watch Next

- Terns Acquisition Completion: Monitor tender offer results anticipated May 2026; closing will concretize pipeline addition impact [S5].

- Clinical Development Milestones: Progress updates on Phase 1/2 trial for TERN-701 in resistant chronic myeloid leukemia patients; Phase 3 readout timelines for MK-1406 influenza antiviral program [S7].

- Regulatory Approvals: Key indications for sac-TMT backed by Blackstone funding could trigger royalty payments post-FDA clearance.

- Quarterly Financial Updates: Observe margin trajectories post-acquisition charges; cash flow generation validating sustainability amid elevated R&D expenses.

- Partnership Revenue: Continued performance from alliances such as with AstraZeneca measured through sales-based revenue recognition patterns aligned with drug lifecycle stages.

Financial Profile Summary (Q1 2026)

Latest financial snapshot

| Metric | Value | Period |

|---|---|---|

| Cash & equivalents | $5.3bn | |

| 2026-03-31 | ||

| Current assets | $35.0bn | |

| 2026-03-31 | ||

| Current liabilities | $26.9bn | |

| 2026-03-31 | ||

| Current ratio | 1.3x | |

| 2026-03-31 |

Source: SEC companyfacts cache [F1].

| Metric | Value (USD billions) | Period Ending |

|---|---|---|

| Revenue | Approx. $16.29 | Q1 2026 |

| Net Loss | $(4.24) | Q1 2026 |

| Cash & Cash Equivalents | $5.33 | March 31, 2026 |

| Total Current Assets | $35.0 | March 31, 2026 |

| Total Current Liabilities | $26.95 | March 31, 2026 |

| Current Ratio | ~1.3 | March 31, 2026 |

| Estimated Net Debt | ~$12.77 | Calculated Q1 2026 |

Merck generated strong operating cash flow of approximately $3.9 billion despite non-cash acquisition charges totaling nearly $17 billion impacting net income negatively [S23]. Capital expenditures remain consistent around the $1 billion range supporting manufacturing capacity enhancements.[S23] Financing activities reflected dividend payouts (~$2.1B) alongside modest treasury stock repurchases [$874M].[S23]

The company preserves strong liquidity but needs to carefully manage leverage given ongoing integration complexities associated with its recent multi-billion-dollar acquisitions.[F1][S20]

Disclaimer: This analysis is an independent industry overview based strictly on publicly available information from SEC filings and reputable news sources without providing investment advice or recommendations.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments