Lionsgate Studios: Franchise Strength Meets Financial Headwinds in a Shifting Media Landscape

Despite iconic franchises like John Wick and Hunger Games underpinning its creative identity, Lionsgate faces acute financial pressures underscored by recent quarterly losses and liquidity constraints.

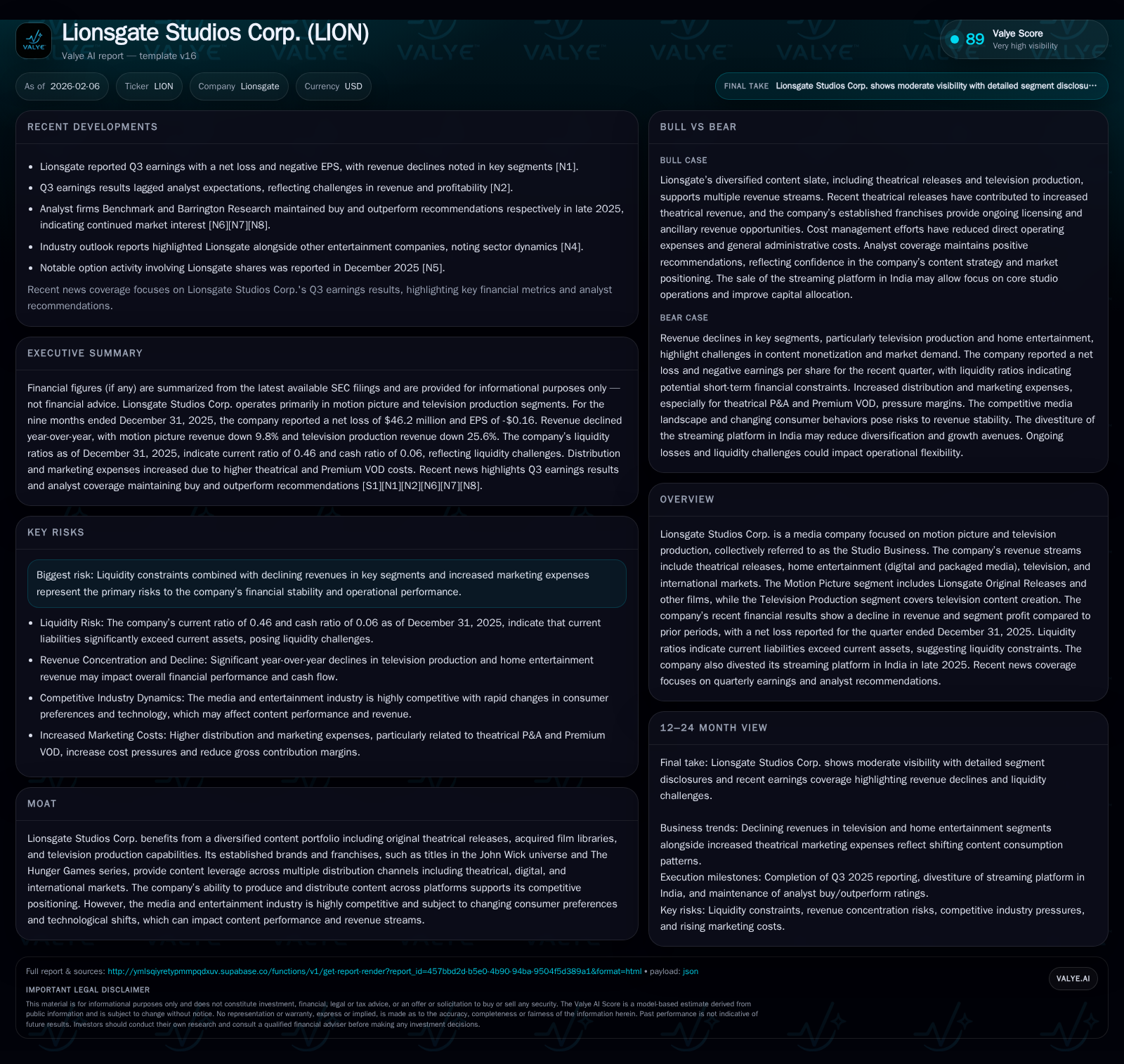

Lionsgate Studios Corp. carries the weight of beloved franchises that continue to define its market presence, yet its latest Q3 2025 results reveal notable declines in revenue and segment profit, alongside a net loss amid challenging cash flow dynamics. Rising marketing expenses and a strategic retreat from the Indian streaming market spotlight attempts to recalibrate resources in a fiercely competitive entertainment environment. The company’s future hinges on balancing franchise-driven content leverage with pressing operational and liquidity risks amid evolving consumer habits and industry disruption.

A Tale of Two Halves: Artistic Triumphs vs Financial Strains

Lionsgate Studios occupies an intriguing crossroads—a company synonymous with high-impact franchises such as John Wick and The Hunger Games that have left indelible marks on global pop culture. These titles represent more than mere box office success; they constitute a strategic moat, offering cross-platform leverage ranging from theatrical to international distribution channels [valye_report_excerpt.moat]. Yet, this artistic acclaim belies a more sobering financial narrative illuminated by the recent Q3 2025 earnings.

While these franchises have generated enduring brand equity, the company’s overall revenue has noticeably contracted. The studio's rich content pipeline seems unable to counterbalance broader fiscal headwinds—reflected in declining segment profits and culminating in a net loss of $46.2 million for the quarter ended December 31, 2025 [F1][S2]. This dichotomy underscores tension between creative success and operational sustainability.

Deep Dive into Q3 2025 Earnings: Revenue Declines and Segment Performance

Delving into the numbers reveals considerable weakening at the segment level. Combined Studio Business revenues waned approximately 17.7%, driven primarily by a nearly 10% dip in Motion Picture revenues to $964.9 million and a steeper blow to Television Production, which fell over 25% year-over-year to $790.3 million [S2]. The contraction suggests softness across content creation pipelines as well as distribution channels.

Segment profit diminished even more sharply; Motion Picture profits plunged by 46%, down to $91.7 million, while Television Production remained marginally down. The steep plunge in theatrical profits points to intensifying cost pressures possibly related to increased marketing spends and production economics. Importantly, intersegment eliminations—which can distort net results—lessened dramatically in Q3 versus prior periods, partially masking true operational declines [S2][N1][N2].

Crucially, marketing expense swelling within distribution—up nearly 20% overall and specifically U.S. theatrical P&A jumping some 28%—strained margins at a time when top-line performance could scarcely support such expenditures.

Navigating Liquidity Woes: Balancing Cash Flow and Current Obligations

Behind headline revenue figures lurks an acute liquidity challenge underscored by balance sheet metrics. At quarter-end, Lionsgate reported current assets totaling approximately $1.32 billion against $2.87 billion of current liabilities, yielding a current ratio near 0.46 —significantly below standard solvency benchmarks [F1][S2].

This discrepancy signals potential difficulties in meeting near-term obligations without resorting to asset sales or external financing. While cash reserves stood at $182 million—offering some buffer—the gulf between liquid assets and liabilities invites caution amid ongoing operational losses.

Management commentary did not indicate extraordinary distress yet acknowledged the imperative for diligent cash flow management amidst strategic shifts including restructuring efforts that trimmed corporate overheads modestly [S2].

Content is King, But at What Cost? Marketing and Operating Expenses Trends

The year-over-year rise in marketing budgets contravened efforts to moderate other operating costs where Lionsgate achieved a decline (operating expenses dropped by around 6.7%) [S2]. This divergence suggests prioritization of promotional spending designed to sustain box office traction or viewer engagement for flagship titles.

However, this elevated spend on prints & advertising (P&A), particularly within the U.S., expanded by more than $51 million (28%), cutting deeply into gross contribution levels which slid over 30% relative to the prior year period despite lower direct operating outlays [S2]. This dynamic poses questions regarding the sustainability of aggressive marketing at times when revenue bases contract and liquidity tightens.

Balancing necessary investment to protect franchise relevance against capital discipline emerges as a critical tension point for Lionsgate going forward.

Strategic Divestitures and Their Implications: Lessons from India Streaming Exit

In December 2025, Lionsgate divested its streaming platform in India—a move interpreted broadly as portfolio rationalization to sharpen focus on core competencies or bolster liquidity reserves [S2]. Exiting the Indian OTT space—one of the fastest-growing digital territories—suggests recalibration driven by intense competitive pressures and perhaps insufficient scale economies or profitability hurdles.

This divestiture curtails international digital expansion ambitions in the near term but may enable redeployment of capital towards stronger-performing segments or franchise development initiatives that command higher returns on invested capital. Nonetheless, exiting an emerging market also relinquishes possible long-term growth avenues amid accelerating global streaming consumption trends.

Moat Under Siege: Competitive Pressures in Motion Picture and Television

Lionsgate's historic moat—anchored by original content production capabilities plus ownership of high-profile film libraries—is increasingly tested by tectonic shifts reshaping the entertainment landscape [valye_report_excerpt.moat][N4][S2]. Streaming giants with deep pockets relentlessly invest in proprietary content while evolving consumer preferences favor direct-to-consumer delivery models over traditional theatrical windows.

Additionally, technology-driven shifts like AI-assisted editing, shorter series formats, or more personalized viewing experiences amplify competitive complexity for traditional studios reliant on longer production cycles.

This new paradigm compels studios like Lionsgate to innovate rapidly while safeguarding legacy revenue channels that currently still contribute substantial portions of operating cash flow—a precarious balancing act highlighted repeatedly in analyst commentary monitoring the sector's evolving contours [N4].

Investor Sentiment and Analyst Perspectives After Latest Earnings

Market reaction following Lionsgate’s Q3 earnings release reflected tempered expectations; shares experienced volatility amid investor reassessment of growth trajectories hampered by revenue declines and sliding profitability [N1][N2]. Analysts noted downside surprises primarily linked to operational execution challenges and rising cost burdens overshadowing marquee content strength.

Some voices advocated caution given ongoing liquidity concerns balanced against franchise IP advantage arguing for watchful monitoring rather than precipitous conclusions at this juncture [N4]. This cautious tone captures underlying uncertainty about timing for recovery amid broader macroeconomic volatility impacting discretionary consumer spending categories including entertainment.

Looking Ahead: Strategic Recommendations amid Industry Shifts

Lionsgate’s path forward demands concerted emphasis on maximizing existing franchise value through diversified platform exploitation—including licensing, international syndication, ancillary products—and incremental innovation in content formats attuned to contemporary consumption patterns.

Simultaneously, reigning in escalating marketing expense without eroding brand presence is paramount as is proactive stewardship of liquidity through further cost rationalizations or forging strategic partnerships that de-risk balance sheet exposures [valye_report_excerpt.risks].

Embracing data-driven audience insights could enhance greenlighting decisions reducing programming risk exposure, while selectively expanding digital direct-to-consumer initiatives calibrated prudently may unlock new growth vectors without disproportionate capital outlays.

In aggregate, alignment between creative visionaries empowered by compelling IP assets with financially disciplined management will be decisive as Lionsgate navigates this pivotal evolutionary phase within the media entertainment domain.

Disclaimer: This report is prepared solely for informational purposes based on publicly available data as of February 6, 2026. It does not constitute investment advice or recommendations.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments