LivaNova's Turnaround: From Environmental Liability to Innovation-led Growth

A detailed examination of LivaNova’s financial recovery, strategic restructuring, and innovation pipeline beyond significant environmental and legal challenges.

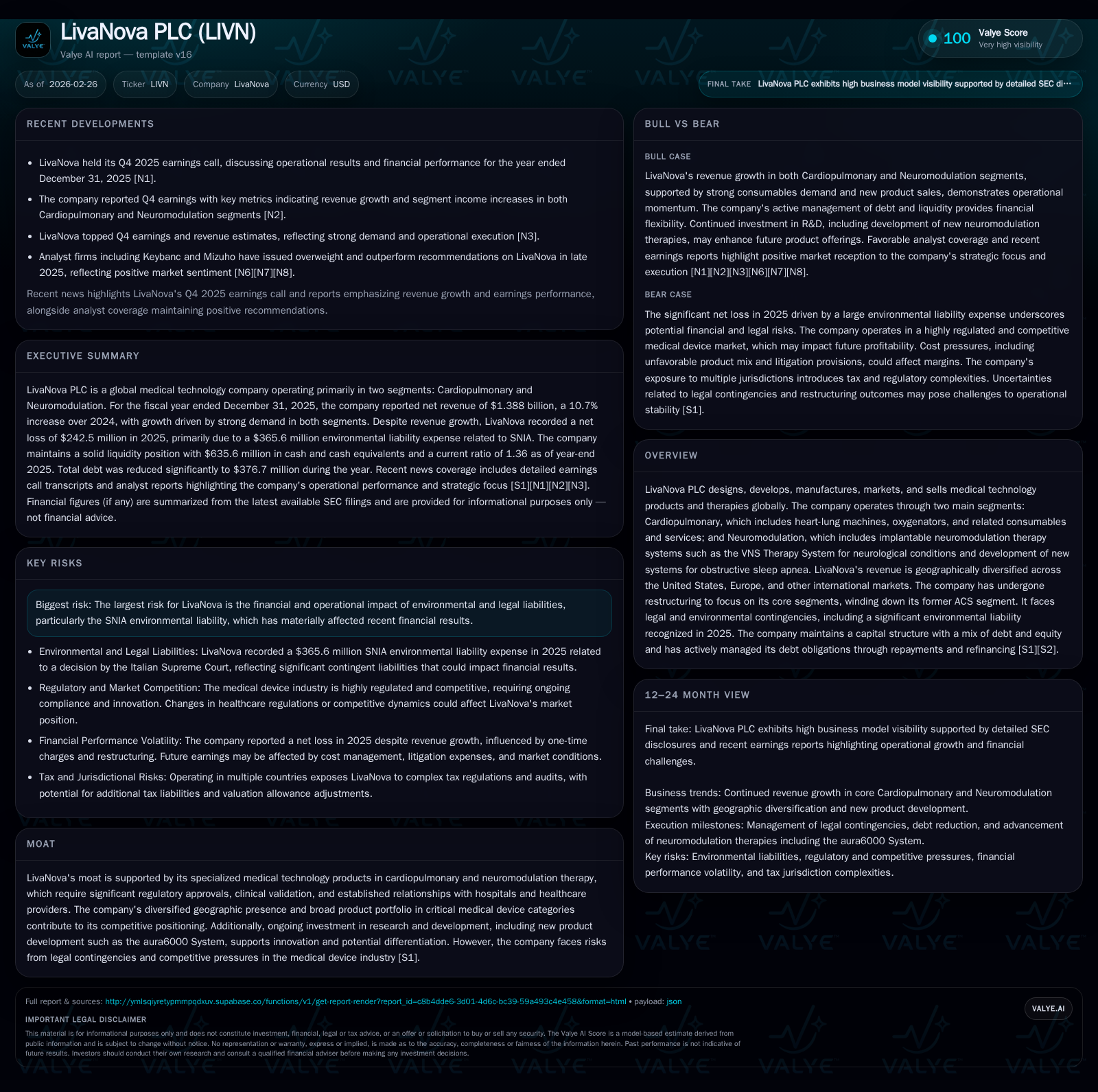

LivaNova PLC faced substantial headwinds in 2025 owing to a large environmental liability tied to legacy SNIA obligations, which heavily impacted net income despite robust operational results. The company demonstrated strong growth in its core Cardiopulmonary and Neuromodulation segments, supported by geographic diversification and durable consumables revenue streams. Aggressive debt reduction efforts markedly improved the capital structure, enabling enhanced liquidity and financial flexibility. Meanwhile, innovation efforts focused on the development of the aura6000 System signal a strategic pivot towards future growth opportunities in implantable neuromodulation therapies.

Strong Revenue Expansion Driven by Cardiopulmonary and Neuromodulation Segments

LivaNova’s 2025 financials exhibit sustained top-line growth anchored in its two core segments: Cardiopulmonary and Neuromodulation [F1][S1][S17]. Overall net revenue increased by a solid 10.7% year-over-year to approximately $1.39 billion. Within this total, the Cardiopulmonary segment was the standout performer with revenues up nearly 15% to about $785 million.

This segment’s growth was geographically skewed towards Europe, which posted an almost 20% increase compared to prior year, supported by enhanced hospital partnerships across key EU markets including Germany, France, Italy, and the UK [S17]. Such expansion reflects increased unit sales of heart-lung machines and oxygenators along with growing consumables—a critical recurring revenue driver common across medical device consumable portfolios that help stabilize revenue during volume fluctuations.

Neuromodulation revenues reached nearly $593 million in 2025, up 7%, paced chiefly by U.S. sales growth at just over 5%. This segment focuses on implantable neuromodulation therapy systems such as the VNS Therapy System used for neurological disorders; it also encompasses development of next-generation products like the aura6000 System targeting obstructive sleep apnea (OSA), indicating fresh pipeline momentum [S1][N1]. The more modest neuromodulation growth rate compared with Cardiopulmonary aligns with typical medtech adoption cycles requiring rigorous clinical validation before mass penetration.

Historical performance (annual)

| FY | Net ($mm) | CFO ($mm) | OpInc ($mm) | Capex ($mm) | Net YoY |

|---|---|---|---|---|---|

| 2025 | -242 | 254 | 199 | 81 | -483.5% |

| 2024 | 63 | 183 | 129 | 47 | +260.4% |

| 2023 | 18 | 75 | -68 | 35 | +120.3% |

| 2022 | -86 | 70 | -77 | 27 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | FCF ($mm) | ROE% |

|---|---|---|

| 2025 | 173 | -20.2 |

| 2024 | 136 | 4.8 |

| 2023 | 40 | 1.4 |

| 2022 | 43 | -7.1 |

Source: SEC companyfacts cache [F1].

Note: ‘NMF’ indicates not meaningful due to operating income turnaround from loss to profit.

Navigating Environmental Liability Impact Amid Operational Improvement

While LivaNova's operational results show marked strength, they were overshadowed in net income terms by a significant non-recurring charge—a SNIA environmental liability expense totaling approximately $365.6 million recognized in fiscal year 2025 [F1][S1][S5]. This historic liability stems from environmental remediation claims linked to SNIA’s chemical sites prior to its spin-off events dating back over a decade.

The scale of this provision is substantial relative to typical litigation expenses for medtech firms but must be understood within the unique context of European demerger legal precedents combined with Italian Supreme Court rulings assessing joint and several liability [S9][S12]. Despite this sizable charge, LivaNova's underlying operating income improved robustly by more than half from the prior year as core business fundamentals remained solid [F1].

Management’s transparent disclosures with precise provisions reflective of probable outcomes demonstrate effective risk governance amid unpredictable legacy contingencies. Market participants should view this large one-off environmental expense separately from underlying operating performance given its episodic nature.

Capital Structure Repair: Aggressive Debt Paydown and Liquidity Management

LivaNova made significant strides improving its leverage profile during the year ended December 31, 2025 [F1][S1][S4][S6]. Total debt dropped sharply from roughly $628 million at end-2024 down to approximately $377 million at end-2025 — a near $251 million reduction principally driven by early repayments on term loan facilities amounting to $200 million in May 2025 plus maturity repayment of $57.5 million on notes [S4].

This deleveraging effort reduced total debt as a percentage of equity from almost half (47.5%) at end-2024 to just over thirty percent (31.4%) heading into early 2026 [F1][S7]. The credit agreement covenants under the Amended First Lien Credit Facility require maintenance of leverage below specified levels (net leverage ratio ≤3.50 times EBITDA) and an interest coverage floor of at least two times EBITDA-to-interest expense — both comfortably met as per latest filings [S4].

Liquidity available through cash reserves plus undrawn revolver facilities stands near $860 million as of December 31, 2025 providing ample headroom [S1][S7]. The effective borrowing rate on term debt was about 7%, incorporating adjusted SOFR-based margins reflective of current market conditions [S4].

By proactively managing debt amortization schedules aligned with cash flows generated from operations alongside prudent cash management measures — including divestments supporting manufacturing expansions — LivaNova has fortified its balance sheet foundation for sustainable operation.

Innovation Pipeline Spotlight: The Aura6000 System and Neuromodulation Prospects

Research & development spending remains prioritized towards advancing proprietary technologies within neuromodulation therapy systems [S1][N1]. This includes further development phases for their investigational aura6000 System targeting obstructive sleep apnea treatment — a space characterized by substantial unmet clinical need and potential market expansion.

Neuromodulation involves implantable pulse generators interfacing directly with neurological pathways such as the vagus nerve; regulatory submissions require multi-phase clinical trials validating safety and efficacy before commercial launch [S17]. Thus iteration through incremental design improvements paired with rigorous post-market studies mark R&D cycles here.

Forward-looking commentary from management highlights these ongoing programs as critical differentiators potentially enabling niche dominance if successful clinical endpoints are achieved [N1]. Given competitive dynamics within medical implantables—where proprietary stimulation algorithms drive product loyalty—this innovation pipeline will serve as an important monitor for medium-term growth projection.

Cash Flow Strengthening Enables Strategic Investments and Financial Flexibility

Operating cash flow registered an increase of almost 40% year-on-year reaching $254 million in fiscal year 2025 versus prior periods [F1][S1]. This ramp reflects stronger core profitability paired with working capital optimization partially offsetting previously elevated litigation-related outflows.

Capital expenditures surged over seventy percent to approximately $81 million evidencing intensified investment activities mostly attributable to software development related to new device functionalities as well as manufacturing footprint enhancements supporting scaling production volumes for key lines [F1]. This capex pattern aligns with typical maturational expenditure profiles seen across mid-sized medtech players balancing innovation spend against operational capacity buildout.

Resultantly, free cash flow generation remains robust near $173 million offering steady runway for funding internal projects without dependence on external financing or dilutive equity issuance.

What to Watch: Regulatory Milestones, Competitive Dynamics, and Contingency Resolutions

Looking ahead, investors should monitor several key areas:

- Upcoming clinical trial results and regulatory clearances relating specifically to the aura6000 System will act as crucial catalysts determining neuromodulation segment trajectory [N1].

- Continued revenue trends within Cardiopulmonary consumables amid global healthcare budget pressures could affect recurring volume stability.

- Resolution timelines around outstanding environmental liabilities remain uncertain; scheduled June 24, 2026 court sessions may provide clarity albeit settlement outcomes retain inherent unpredictability [S10][N3].

- Competitive pressures are expected given the dynamic landscape encompassing implantable devices where rapid technological evolution demands sustained innovation investment.

- Corporate cash flow health and capital allocation policy shifts—including potential dividend or buyback revisits—should be watched relative to balance sheet improvements [F1].

Ultimately, LivaNova presents a compelling case study reconciling legacy legal burdens while realigning toward innovation-fueled growth driven by structural segment leadership within critical medical technology fields.

Disclaimer: This analysis is based on publicly filed documents and news sources available as of February 26, 2026; it does not constitute investment advice or recommendations.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments