LightPath Technologies: Balancing Strong Liquidity and Analyst Enthusiasm Against Persistent Losses

LightPath Technologies presents a compelling juxtaposition of healthy cash reserves and bullish analyst sentiment amid ongoing quarterly losses and opaque sector classification.

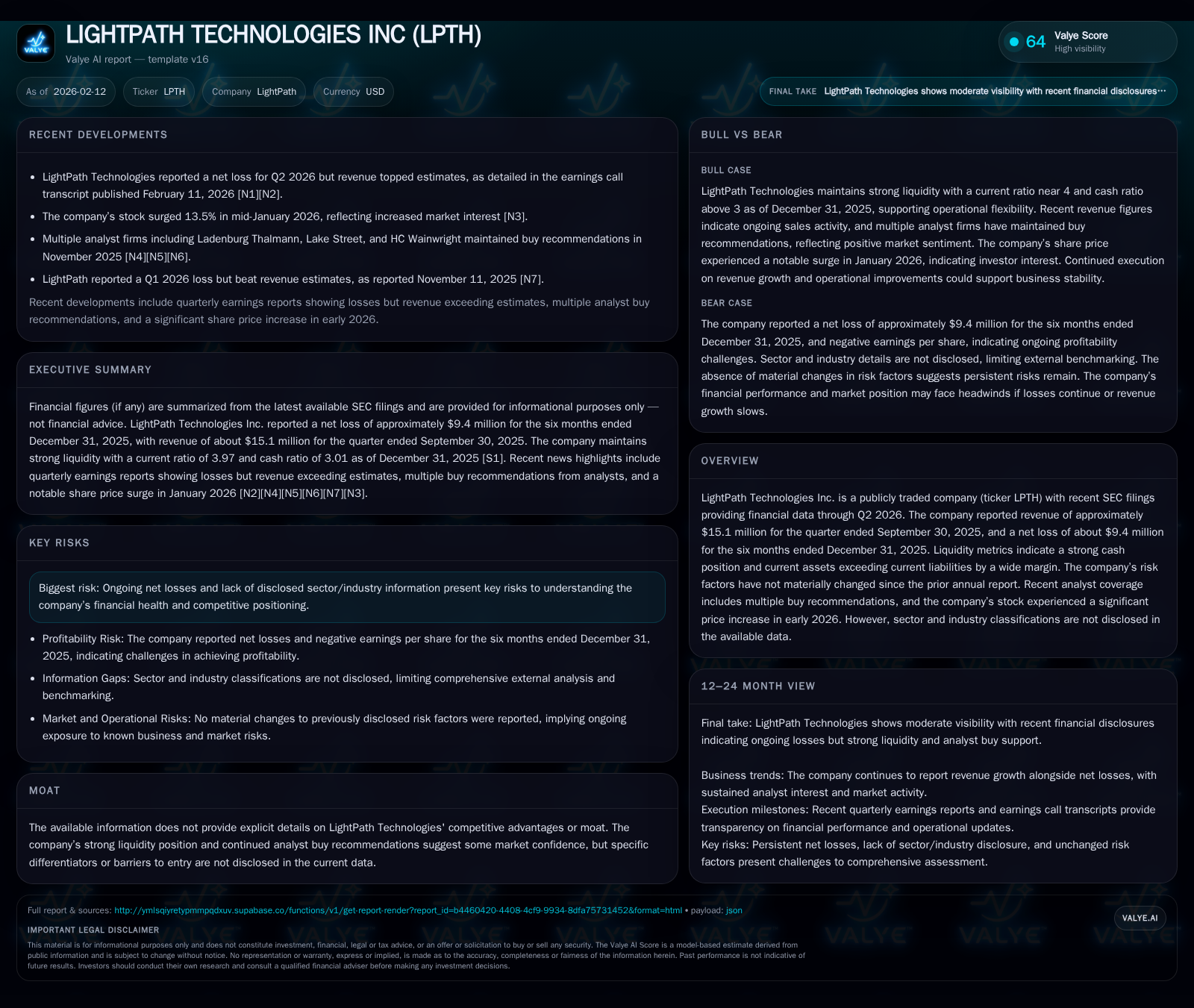

In Q2 2026, LightPath Technologies beat revenue expectations with $15.1 million sales but continued to report a net loss totaling approximately $9.4 million for the half-year period ended December 2025. Despite persistent losses, the firm’s substantial liquidity — nearly four times current liabilities in current assets and over $73 million in cash — underpins confidence among several analysts who issued buy ratings following a significant early-2026 stock rally. However, the absence of disclosed industry categorization and recognizable competitive moats complicates efforts to gauge sustainable growth prospects and risk exposure. The company navigates a precarious balance between operational challenges and financial flexibility, warranting careful observation as investors contemplate its longer-term trajectory.

Navigating Q2 2026: Revenue Beats Amid Losses

LightPath Technologies demonstrated notable top-line resilience in the quarter ending September 30, 2025, reporting revenues of approximately $15.1 million [F1], surpassing consensus expectations communicated around that period [N2]. This revenue beat is particularly striking against the backdrop of sustained unprofitability; for the six months ending December 31, 2025, LightPath posted a net loss close to $9.4 million [F1]. The juxtaposition of growing sales alongside continuous negative earnings underscores complexities in the company’s operational dynamics—an indicator that while demand or order flow may be strengthening, margin pressures, elevated costs, or investments continue to weigh heavily on the bottom line.

The earnings call transcript from February 11, 2026 [N1] hints at management's optimism towards incremental progress but also reflects caution regarding expense management and scaling efficiencies necessary to bridge toward profitability. Without detailed segment disclosure or margin breakdowns publicly available, external observers must infer that operational leverage remains elusive despite encouraging topline momentum.

Cash Reserves as a Strategic Buffer

A cornerstone of LightPath's financial profile is its robust liquidity position. As of December 31, 2025, the company held approximately $73.5 million in cash and cash equivalents [F1], bolstered by current assets tallying just over $97 million against current liabilities near $24.4 million—the resulting current ratio stands at an impressive 3.97 [F1]. This cushion not only shields LightPath against near-term solvency risks but also equips it with optionality—to pursue R&D initiatives, sustain operations through volatile periods, or potentially finance strategic ventures without immediate capital raises.

This level of liquidity is noteworthy given the recurring losses; it signals prudent treasury management and possibly past capital injections that have fortified the balance sheet. However, liquidity alone cannot substitute for generating operating profits indefinitely; it forms an enabler rather than a solution.

Analyst Optimism vs. Market Reality

Market reaction during early 2026 mirrored newfound enthusiasm: LightPath's shares surged roughly 13.5% in January [N3], fueled by positive analyst coverage including multiple buy recommendations noted recently [valye_report_excerpt]. These upgrades often emphasize LightPath’s enticing valuation relative to tangible cash reserves and improving revenue trends.

Yet this optimism contrasts with persistent underlying deficits—posing questions about whether the stock's momentum stems from fundamental shifts or speculative positioning. Key investors appear focused on potential inflection points where operational cost control might align with stable revenue growth to crystallize profits.

The mixed signals highlight a delicate dance between hope for turnaround catalysts and vigilance toward protracted losses—a duality not uncommon in emerging technology-related companies constructing market footholds.

Assessing the Elusive Moat

One striking omission in available disclosures is any explicit statement regarding LightPath’s competitive moat or differentiated advantage [valye_report_excerpt]. No clear barriers to entry, proprietary technologies narrows, or lock-in mechanisms are detailed publicly.

From an investor perspective, this opacity complicates assessing sustainable defensibility against peer entrants or substitutes. While solid liquidity may provide temporary cover, longer-term value creation often demands some form of measurable competitive advantage—be it IP depth, customer relationships, manufacturing excellence, or market exclusivity.

Without transparency on such attributes, assumptions must remain circumspect; past market confidence could rest more on financial runway than intrinsic strategic positioning.

Industry Mystery: The Challenge of Classification

Perhaps uniquely challenging is LightPath’s lack of sector or industry tagging in both official filings and market data platforms [valye_report_excerpt]. This absence hinders routine benchmarking exercises critical for valuation contextualization and risk evaluation.

When investors cannot readily place a company within existing industrial frameworks—be it optics manufacturing, photonics components, or advanced materials—it complicates comparisons to peers’ growth trajectories, margin profiles, and cyclicality patterns.

This fuzziness can introduce additional volatility as market participants speculate about relevant end-markets or technological niches where LightPath operates, amplifying interpretive uncertainty.

Risk Factors in a Steady State

Reviewing recent SEC filings confirms that risk elements remain largely unchanged since the annual report for fiscal year ended June 30, 2025 [S2]. There were no newly disclosed material risks through December 31, 2025—indicating a steady-state risk profile despite operational challenges.

Key ongoing risks presumably include continuing net losses raising sustainability questions; potential need for future capital if cash burn persists; lack of explicit moat exposing vulnerability to competitive pressures; and uncertainties associated with incomplete sector disclosure impacting investor clarity.

The stable risk factor environment may suggest no acute existential threats emerged during this period but does little to alleviate structural concerns inherent in prolonged unprofitability.

Amplified Share Price: Bubble or Breakout?

The sharp share price ascent observed starting January 2026 [N3] invites scrutiny regarding its drivers. Was this movement primarily triggered by earnings surprises such as revenue beats reported shortly afterward [N2]? Or was it more speculative exuberance fueled by positive analyst sentiment detached from fundamentals?

While enhanced revenue figures provide some fundamental underpinning, they fall short of reversing loss trends immediately. Hence, part of this rally could be attributed to hopeful speculation about an imminent turnaround rather than confirmed operational transformation.

Investors should weigh this cautious interpretation alongside broader market dynamics affecting small/mid-cap technology-related equities where volatility driven by sentiment swings is common.

Future Outlook: Growth Catalysts and Lingering Questions

Looking ahead, LightPath finds itself at an inflection characterized by strong financial headroom but unclear strategic visibility. Translation of positive analyst views into durable shareholder value depends critically on several factors: achieving consistent profitability by leveraging revenue momentum; articulating clearer competitive advantages to assure market positioning; clarifying industry classification to enable more informed investor evaluation; and managing risks inherent in current loss patterns.

No single element currently guarantees success—but abundant liquidity cushions that journey. Investors will likely monitor quarterly results closely for signs of margin improvement alongside increased transparency about product lines and markets served.

The pathway forward is thus marked by both opportunity afforded through financial strength and uncertainty stemming from missing competitive clarity—a dual narrative inviting attentive stewardship rather than cavalier optimism.

Disclaimer: This analysis is informational only and does not constitute investment advice or recommendations.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments