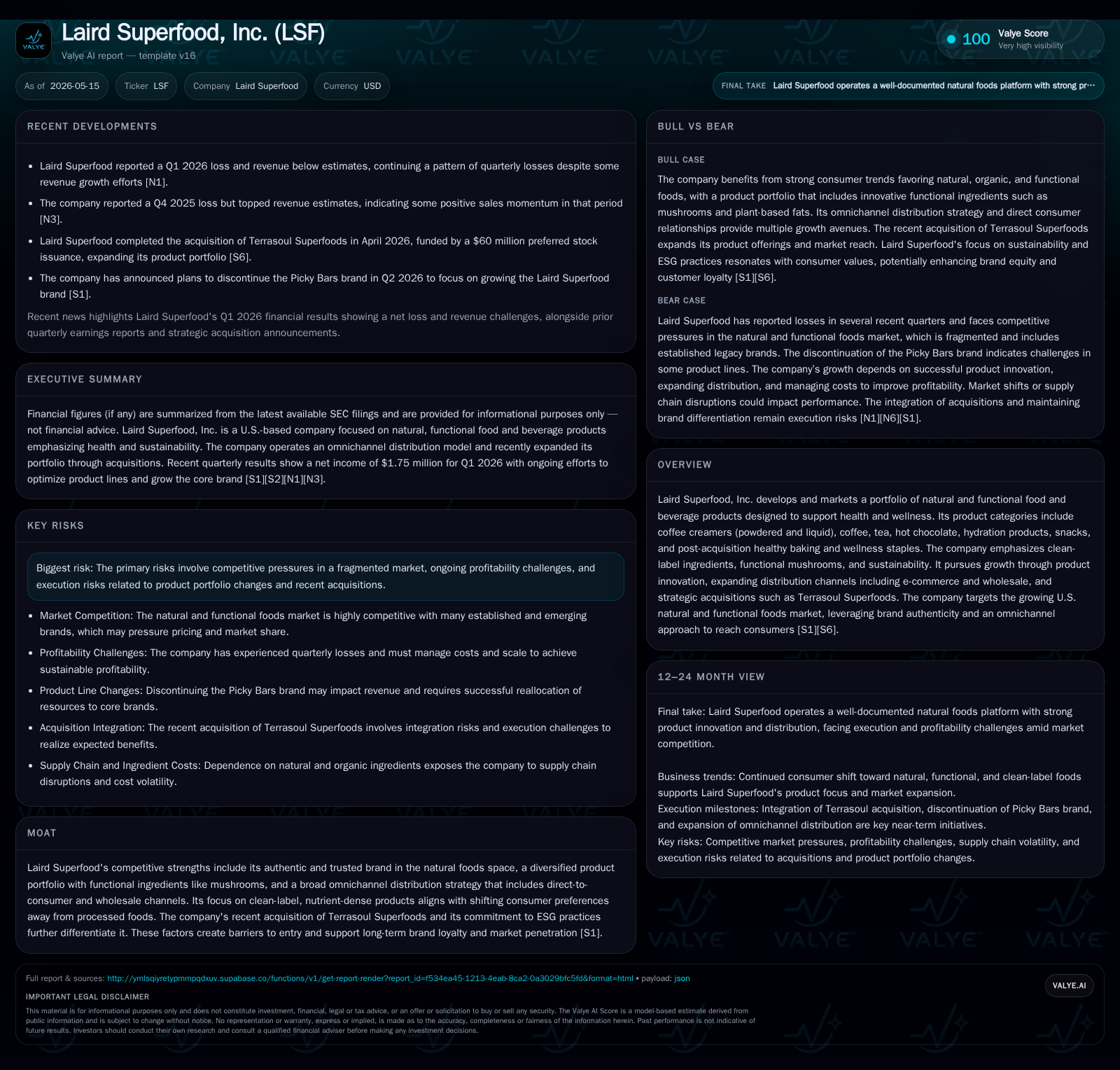

Laird Superfood Sharpening Growth Strategy Amid Q1 Revenue Shortfall

Q1 2026 results reveal financial pressures even as LSF pursues omnichannel expansion and integration of Terrasoul acquisition.

Laird Superfood reported a first-quarter revenue shortfall paired with ongoing losses, reflecting margin pressures and operational costs tied to recent expansion efforts. The company continues to leverage an omnichannel sales strategy, balancing e-commerce and wholesale growth, while integrating its transformative acquisition of Terrasoul Superfoods. Although the natural and functional foods market remains structurally attractive, execution risks around product mix and profitability persist. Key near-term focus areas include expanding retail distribution, stabilizing margins, and tracking acquisition synergies.

Q1 2026 Earnings Recap and Near-Term Operational Highlights

Laird Superfood’s latest quarterly filing for Q1 ended March 31, 2026 [S2][S3] disclosed a loss that missed market expectations alongside revenues falling short of forecasts [N1]. Despite ongoing top-line growth initiatives driven by increased distribution and innovation efforts, the company continues grappling with margin pressures exacerbated by elevated costs tied to integrating its April-acquired Terrasoul Superfoods business [S2][S3]. These factors underline persistent challenges balancing investment in growth while managing profitability.

The quarter’s results mark a critical checkpoint as LSF recalibrates its strategy amidst expanding product offerings and channel development. Pressure on gross margins partly reflects commodity price inflation within specialty ingredients like functional mushrooms—a core differentiator—while also absorbing incremental SG&A expenses linked to marketing and scaling operations. As such, sustained losses are symptomatic of the company's current early-growth phase wherein scale economies remain nascent.

Operational commentary reveals that wholesale channels now constitute approximately half of overall sales, consistent with the longer-term strategic plan to balance e-commerce dominance with physical retail presence [S1]. Channel diversification aims at capturing broader consumer touchpoints but requires heavy upfront investments in merchandising and logistics.

Business Model: Portfolio, Product Quality, and Consumer Appeal

Founded on authentic natural nutrition principles, Laird Superfood builds its business by developing high-quality consumables designed to support health and wellness through clean-label ingredients augmented by functional properties. Its flagship categories center on coffee creamers—both powdered and liquid—with proprietary blends incorporating adaptogens and particularly functional mushroom extracts shown to support cognitive focus and stress resilience [S1].

Beyond coffee creamers, the portfolio extends into coffee sachets, tea blends, hot chocolate mixes, hydration enhancers (e.g., electrolyte powders), nutrient-dense snacks including bars from its Picky Bars subsidiary, as well as more recently healthy baking products and wellness staples absorbed through the acquisition of Terrasoul Superfoods [S1][S9]. This diversified offering strategy appeals to a broad spectrum of health-conscious consumers seeking minimally processed alternatives free from artificial additives.

The emphasis on nutrient density and sustainability aligns closely with evolving consumer preferences away from ultra-processed foods. LSF’s formulation philosophy targets functionality paired with taste appeal—a notable differentiation factor in the crowded superfood segment. R&D efforts continue advancing novel formulations leveraging mushroom compounds such as lion’s mane or chaga alongside adaptogens like ashwagandha.

Market Positioning in the Competitive Natural and Functional Foods Industry

LSF operates within the highly fragmented yet rapidly growing U.S. natural foods sector estimated at $104.7 billion in 2023 with projected CAGR exceeding 13% through 2030 [S1]. Within this space, functional mushrooms represent an emerging subcategory valued at $5.5 million in North America but forecasted for robust double-digit expansion due to increasing wellness adoption trends.

Competitively, LSF contends with multiple established specialty brands offering standalone superfood or functional ingredient products; however it distinguishes itself via an integrated platform approach spanning multiple categories rather than isolated SKUs [S1]. This strategy enables cross-selling potential across adjacent formats (e.g., coffee creamer users might convert to hydration powders).

Pricing power hinges on demonstrating clear health benefits coupled with premium clean-label positioning. Supply chain sustainability is another vector of differentiation: sourcing organic or sustainably harvested mushroom ingredients entails higher input costs but underpins brand authenticity reinforcing customer loyalty.

Regulatory compliance around natural claims remains manageable without significant litigation at present though vigilance is required given sector scrutiny around health substantiation claims [S1]. Consumer adoption favors brands authentically connected to lifestyle narratives—a role LSF leverages through founder affinity (notably actor Laird Hamilton) propping brand credibility.

Growth Drivers: Distribution Expansion, Product Innovation, and M&A Integration

Growth catalysts emerge from three intertwined levers:

- Omnichannel distribution gains: The aim is further expanding physical retail penetration beyond current levels balanced against maintaining direct-to-consumer e-commerce momentum. Wholesale sales now approach parity with digital channels (~50% each) [S1], reflecting successful retailer onboarding but necessitating inventory scale-up and supply chain optimization.

- Product innovation pipeline: Incremental launches targeting gaps within existing categories (e.g., new flavor profiles or convenient formats) alongside line extensions tapping emerging wellness trends (e.g., gut health formulations). Innovation serves as both retentive force among customers and attractor for new segments.

- Integration of Terrasoul Acquisition: Closed April 21, 2026 [S9], this $48 million cash deal plus potential earnout expands capability into healthy baking goods—an adjacent high-growth category complementary to existing snack offerings—and broadens wellness staple assortments supporting repeat consumption occasions [S9][S11]. The acquisition adds revenue scale but also complexity given cultural alignment needs and cost synergy realization challenges.

Execution capacity across these fronts will dictate trajectory shifts from early-stage investment mode toward sustainable profitability in medium term. Particular focus remains enhancing supply reliability for key inputs such as organic mushrooms while streamlining channel-specific marketing strategies.

Risks and Constraints: Profitability Pressures, Market Fragmentation, and Execution Challenges

Despite promising growth vectors, LSF confronts several headwinds:

- Ongoing financial losses: The demonstrated Q1 net loss underscores pressure on EBIT margins stemming from elevated input costs, SG&A spending intensity related to channel expansion efforts, and integration expenses from recent acquisitions [N1][S2]. Transitioning from an early-stage enterprise to operational scale requires effective cost control without stifling innovation.

- Capital requirements: While current cash ($10.2M) positions LSF relatively well [F1], additional funding rounds or debt facilities may be necessary if organic cash flow fails to ramp sufficiently given intensified competition driving promotional activities [S1]. Equity issuance dilution or debt layering entail governance trade-offs.

- Market competition: The natural foods segment’s low barriers foster fragmentation with numerous niche entrants vying for consumer attention amidst aggressive product launches by incumbents delivering similar claims at lower prices disrupting pricing leverage [S1].

- M&A integration risk: Absorbing Terrasoul Superfoods’ operations introduces complexity around systems harmonization, cross-brand marketing coherence, margin stabilization post-acquisition—any misstep could impair expected synergies or dent investor confidence.

- Regulatory/compliance: Although presently the company meets consumer protection rules without material litigation exposure [S1], evolving regulations around health attributes promotion may impose new compliance cost burdens or constrain claim freedom impacting market positioning subtly over time.

Overall these constraints manifest typical scaling pains encountered by fast-growing companies seeking broader category leadership while preserving trusted niche brand status.

Upcoming Catalysts: Guidance Expectations and Milestones to Monitor

Key near-term items investors might track include:

- Next quarterly earnings communication expected mid-August 2026 should shed light on ability to improve topline growth trajectory versus Q1 shortfall alongside margin trends factoring operational leverage gains or further cost pressures [S2][S3].

- Progress reports related to retail footprint acceleration especially placement gains in national grocery chains providing visibility into broader consumer access points.

- Successful rollout timing of planned product launches supporting refreshed portfolio appeal potentially inflecting same-store-sales metrics within wholesale channels.

- Early signals confirming integration benefits realization from Terrasoul acquisition assessing revenue cross-pollination effects against incremental SG&A outlays.

- Monitoring working capital efficiency improvements feeding into cash flow sustainability critical for funding pathway clarity absent external capital raises.

Achievement on these metrics will materially influence confidence around transitioning toward break-even operations sustainably.

Financial Snapshot: Liquidity, Capital Structure, and Profitability Overview

Latest financial snapshot

| Metric | Value | Period |

|---|---|---|

| Cash & equivalents | $10mm | |

| 2026-03-31 | ||

| Current assets | $37mm | |

| 2026-03-31 | ||

| Current liabilities | $12mm | |

| 2026-03-31 | ||

| Current ratio | 3.19x | |

| 2026-03-31 |

Source: SEC companyfacts cache [F1].

| Metric | Value |

|---|---|

| Cash & Equivalents | $10.2M |

| Total Debt | $51K |

| Current Ratio | 3.19 |

| Net Income (Trailing) | -$3.25M |

The balance sheet remains sufficiently liquid with over $10 million in cash equivalents enabling operational flexibility despite net income losses trailing approximately $3.25 million as of end-2025 [F1]. The nominal debt level (~$51K) indicates minimal leverage risk providing capacity for strategic investments or buffering unforeseen cash flow fluctuations.

However sustaining this positive liquidity profile depends heavily on reversing operating losses through margin improvement or higher volumes; otherwise prolonged dependence on equity/debt markets arises posing dilution/cost-of-capital concerns amid volatile food sector dynamics [S2].

This analysis synthesizes latest SEC disclosures along with recent news reports focusing on Laird Superfood's operating environment without offering investment advice or recommendations.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments