Lyft’s Complex Transition: Navigating Profitability, Competition, and Regulatory Headwinds in Multimodal Mobility

A detailed exploration of Lyft’s shift from rideshare pioneer to diversified mobility platform amid fierce rivalry and evolving legal challenges.

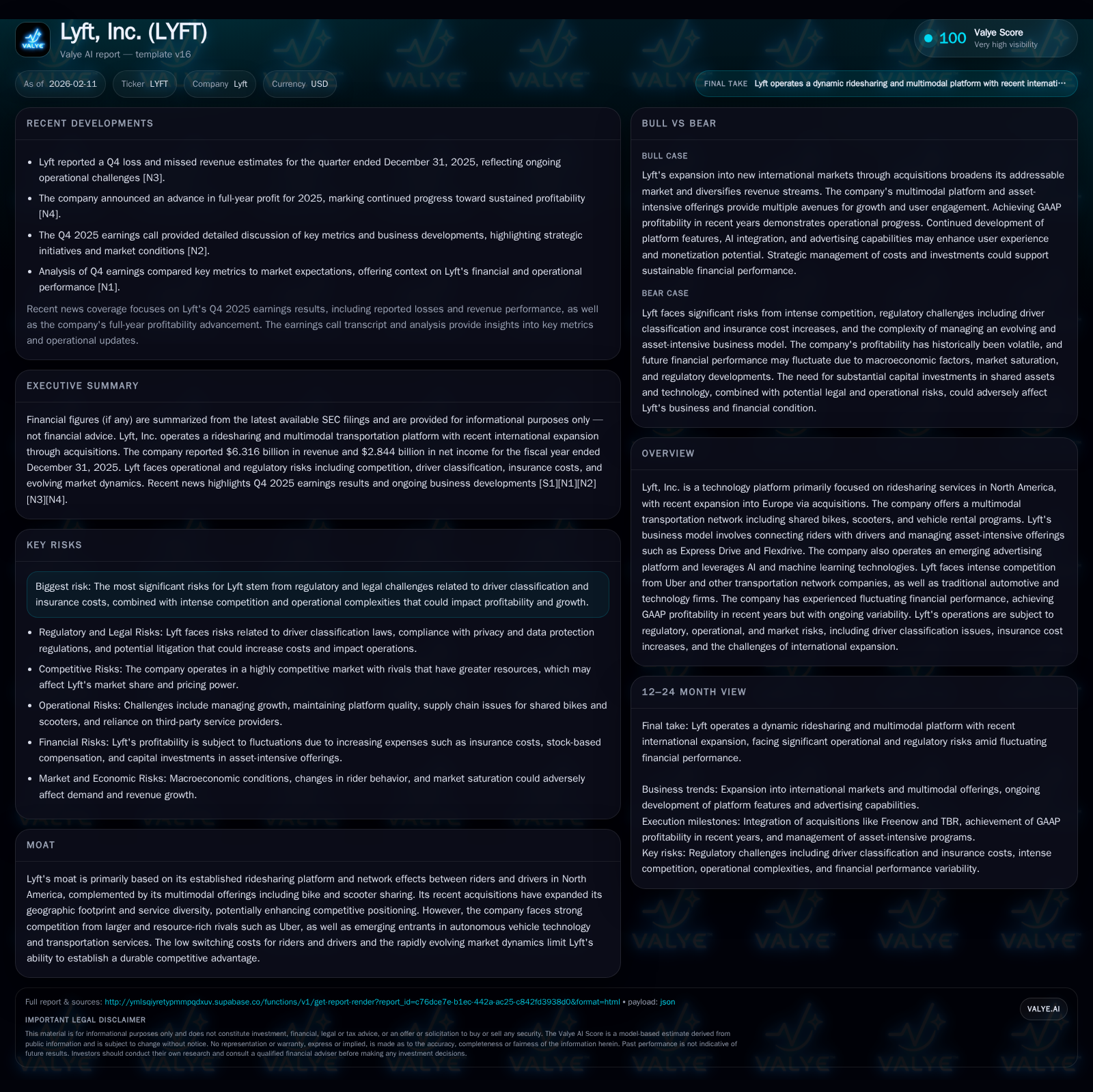

Lyft, Inc. has evolved beyond its initial North American ridesharing roots into a multimodal transportation platform that includes bike and scooter sharing as well as vehicle rental programs. Despite reporting a substantial full-year net income gain of $2.84 billion in 2025, the company demonstrated signs of revenue pressure and missed estimates in Q4, underlining the volatile path toward sustained profitability. Facing formidable competition from Uber and emerging mobility tech firms alongside complex regulatory environments—especially around driver classification and insurance—Lyft’s strategic investments in AI, advertising, and international expansion reflect both opportunities and heightened operational risks. Managing cash flow constraints amid liquidity concerns remains critical as Lyft balances growth ambitions with market realities.

From Ride-Hailing Roots to Multimodal Ambitions: Mapping Lyft's Business Evolution

Since launching its ridesharing marketplace in 2012, Lyft has increasingly molded itself into a comprehensive transportation platform that transcends traditional ride-hailing. Originally positioned exclusively as a connector between drivers and riders across North America, it now offers shared electric bikes and scooters alongside vehicle rental programs such as Express Drive and Flexdrive [S1]. This broader multimodal approach reflects Lyft’s strategic response to shifting consumer preferences toward flexible urban mobility solutions.

Crucially, these expansions complicate operational oversight — integrating asset-heavy initiatives requires balancing capital intensity with the scalability advantages typical of tech platforms. Additionally, Lyft's nascent advertising platform (Lyft Ads) represents another vector for monetization distinct from ride fares [S1]. Collectively, these efforts demonstrate Lyft’s pursuit of diversified growth avenues amid mature ride-hailing markets.

The Profitability Puzzle: Decoding Lyft’s Financial Upswing Amid Market Headwinds

Lyft reported a notable GAAP net income of approximately $2.84 billion for full-year 2025, signaling an important financial milestone [F1]. Yet, the fourth quarter presented nuanced challenges: revenue missed Wall Street expectations despite positive overall earnings results [N1][N3]. This dichotomy underscores the volatility intrinsic to Lyft's evolving business model.

The revenue miss can be partly attributed to intensifying competition driving price compression, seasonal demand variation, or operational expenses linked to expansion investments [N3]. Understanding whether profitability stems from transient cost controls or sustainable operational improvements is critical. The interplay between fluctuating revenue streams from ride services versus newer offerings like Express Drive or advertising complicates straightforward extrapolations.

Competitive Skirmishes: Lyft versus Uber and the Emerging Mobility Titans

Within North America’s rideshare arena, Uber commands dominant scale advantages — greater geographic breadth, deeper liquidity on both rider and driver sides, plus brand recognition that leverages network effects robustly [N7][N10][S1]. Lyft occupies a niche but must continuously innovate to capture incremental market share.

Emerging competitors focusing on autonomous vehicle development or niche alternative mobility solutions add layers of complexity. Unlike pure-play ride-hailing experts of the past decade, these entrants threaten the traditional demand-supply balance with technology potentially disintermediating human drivers or reshaping user expectations [S1]. Lyft’s ability to integrate autonomous technologies through partnerships may prove strategically pivotal but also uncertain at this stage.

Switching costs remain low for both riders and drivers — diminishing moat durability — amplifying the importance of differentiated services beyond price alone [S1]. This milieu necessitates constantly evolving value propositions encompassing convenience, safety assurances, pricing innovation, and ancillary services.

Navigating Regulatory Turbulence: Impact of Driver Classification and Legal Complexities

Perhaps no factor weighs heavier on Lyft's operational outlook than the legal status of its drivers. Classifying drivers as employees rather than independent contractors would substantially increase labor costs through wages, benefits, insurance obligations—and would disrupt the flexible labor model foundational to ridesharing economics [S1][S2].

Ongoing litigation risks and regulatory uncertainties require Lyft to maintain adaptive compliance strategies; moreover insurance coverage adequacy remains a focal point given liability exposure inherent in passenger transport [S1]. The company must also brace for potential increases in claims costs alongside evolving privacy regulations influencing data handling practices within its digital ecosystem [S1].

These overlapping legal pressures elevate operational risk profiles materially, imposing cost volatility that complicates financial forecasting or long-term planning.

Empowering the Fleet: Managing Drivers, Vehicle Rentals, and Asset-Intensive Programs

Securing an engaged pool of drivers is essential for service reliability but also costly given competitive incentives amidst rising living costs. In parallel, vehicle rental programs such as Express Drive mitigate driver ownership barriers by supplying vehicles but introduce asset-heavy commitments requiring sophisticated fleet management and expense controls [S1][S2].

Balancing driver retention incentives against margin pressures demands calibrated approaches that preserve user experience without eroding profitability excessively. Moreover, micromobility assets (bikes/scooters), while light asset classes comparatively speaking, present supply chain challenges influenced by global component shortages or manufacturing constraints impacting deployment velocity [S1].

Operational complexity multiplies as Lyft refines algorithms matching rider demand with hybrid fleets across modalities.

Tech Advancements as Differentiators: AI, Machine Learning, and Advertising Platform Developments

Investment into artificial intelligence (AI) and machine learning (ML) underpins Lyft’s strategy to optimize routing efficiency, dynamic pricing models, fraud detection frameworks, and personalized customer experiences [S1][S2]. Such technological refinements aim not only to reduce operational costs but also enhance retention through superior service quality.

Concurrent development of Lyft Ads introduces a supplementary revenue stream by leveraging proprietary data insights for targeted marketing while keeping rider app engagement intact [S1]. As this advertising ecosystem is nascent but growing, it presents upside potential if scaled effectively without diluting user trust or experience.

Technology thus forms both an enabler for operational excellence and a pillar for strategic diversification amid compressing ride-fare margins.

Geographic Expansion and Acquisition Strategy: European Forays and Beyond

Recent acquisitions have propelled Lyft into European markets — a meaningful extension geographically that diversifies revenue base beyond traditionally U.S.-centric operations [S1]. Such moves open new growth pathways but also expose Lyft to regional regulatory complexities including local labor laws, taxation regimes, safety mandates, and cross-border reporting requirements.

Integration risks accompany every acquisition phase: harmonizing culture, systems interoperability challenges with existing tech stacks plus aligning marketing approaches locally all require resources that potentially weigh on near-term profitability.

Nonetheless internationalization offers strategic insurance against saturation in core markets if managed prudently.

Cash Flow and Balance Sheet Health: Interpreting the Current Liquidity Concerns

Financial statements reveal current assets totaling roughly $2.92 billion contrasted with current liabilities exceeding $4.53 billion at year-end 2025 — yielding a concerning current ratio near 0.65 [F1]. This signals potential liquidity strain where short-term obligations outpace readily available assets.

Cash & equivalents hover around $1.13 billion [F1], indicating limited buffer for sudden funding needs or capital expenditures without external financing initiatives. Consequently managing working capital tightly is imperative especially amid macroeconomic uncertainties or unexpected operational shocks.

Financial flexibility may be constrained by debt covenants or market conditions affecting capital raising costs potentially impacting strategic execution timelines.

Risks on the Horizon: Operational, Legal, and Market Dynamics to Monitor

Beyond regulatory complexities detailed earlier lie broader operational risks including cybersecurity threats targeting rider/driver data or payment systems which could impair trust or trigger costly remedial actions [S1]. Supply chain disruptions affecting micromobility fleet upkeep could degrade service availability, and corresponding reputation risk follows accordingly.

Market volatility in consumer demand linked to macroeconomic cycles can affect utilization rates sharply given discretionary nature of ridesharing trips [S1]. Maintaining organizational culture during rapid scaling phases also poses internal risks tied to employee turnover or talent retention challenges particularly in tech roles vital for innovation momentum.

Hence investors should remain vigilant on these multifaceted risk vectors despite optimistic headline profitability metrics.

The Outlook: Sustainability of Profits and Strategic Growth Trajectories

Lyft stands at an inflection point balancing commendable recent profitability against lingering top-line pressures and liquidity tightness. While technology-driven efficiency gains combined with international expansion constitute plausible levers for sustainable growth—the landscape remains fiercely contested by Uber’s scale advantage plus accelerating autonomous vehicle threats altering cost structures fundamentally.

Strategic discipline over fleet management costs coupled with regulatory navigation prowess will dictate margin resilience going forward. Furthermore successfully scaling ancillary revenues like advertising will be crucial to diversify beyond core ride fares vulnerable to commoditization effects.

Emerging geopolitical or economic shocks may amplify headwinds; however continued innovation investment signals management confidence aiming for durable competitive positioning nonetheless [N14][S1][F1]. Monitoring quarterly performance fluctuations closely alongside regulatory developments will be key to assessing how foundational these trends prove over time.

This analysis is intended solely for informational purposes reflecting company disclosures as of early 2026 along with industry context; it does not constitute investment advice.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments