Envista Holdings Corp Deep Dive: Earnings Momentum, Innovation-driven Moat, and Strategic Growth Challenges

An analytical exploration of Envista's recent financial performance, segment dynamics, innovation focus, and strategic risks amid evolving industry pressures.

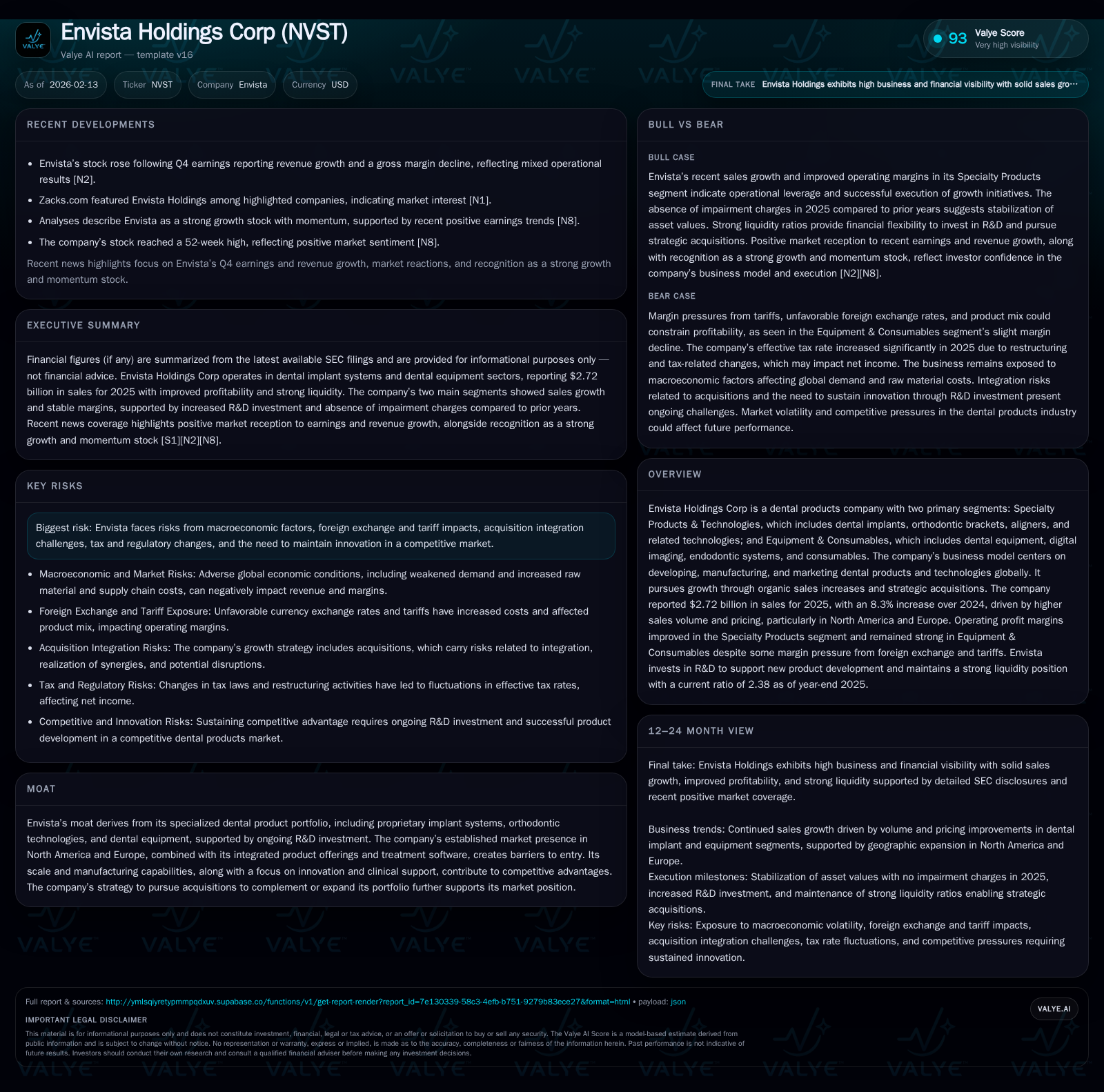

Envista Holdings Corp delivered a notable Q4 2025 earnings beat fueled by strength across its Specialty Products & Technologies and Equipment & Consumables segments, prompting a positive market reaction despite margin pressures from FX and tariffs. Its durable moat, anchored in proprietary dental technology and sustained R&D investment, underpins competitive positioning but must be weighed against integration challenges from acquisitions and macroeconomic headwinds. The company's liquidity remains robust with improved operating profit margins in key segments, though regulatory and global economic risks loom. Future growth hinges on balancing innovation leadership with operational agility amidst sector-wide disruptions.

Riding the Wave: Analysis of Envista’s Recent Earnings Surprise and Market Response

Envista Holdings Corp’s Q4 2025 earnings release ignited an upbeat reaction in equity markets, with shares advancing post-announcement [N1]. The company reported $2.72 billion in sales for the full year—a robust 8.3% increase over 2024—driven by volume increases alongside price adjustments particularly evident across North American and European markets [F1]. This revenue beat outpaced consensus expectations despite downward pressure on gross margins linked primarily to adverse foreign exchange moves and tariff-related cost increments. Notably, operating profit margins improved in the Specialty Products segment while Equipment & Consumables faced margin headwinds. This duality highlights a nuanced earnings landscape where top-line momentum tempers underlying cost structure challenges amid global volatility.

Unpacking Segment Performance: Specialty Products & Technologies vs. Equipment & Consumables

Envista’s business bifurcates into two core segments with distinct growth drivers. The Specialty Products & Technologies segment — encompassing innovative dental implants, orthodontic brackets, aligners, and associated tech — contributed materially to margin expansion during 2025 [S1]. This segment leveraged pricing power supported by proprietary product offerings and sustained clinical demand. By contrast, the Equipment & Consumables segment, which includes digital imaging systems and endodontic equipment, maintained steady revenue gains but experienced margin pressure partly due to fluctuating currency rates and tariff implementation costs affecting component sourcing [S1]. The balanced interplay between segments underscores Envista’s diversified exposure; Specialty Products acts as the margin driver while Equipment & Consumables provides stable cash flow albeit within a more cost-volatile environment.

Innovation at the Core: How Envista’s R&D Fuels Its Competitive Edge

Central to Envista’s moat is its investment in research & development aimed at maintaining technological leadership within the dental industry [valye_report_excerpt]. Development efforts span proprietary implant systems that cater to evolving clinical needs, orthodontic technologies enhanced by integrated treatment software packages, and ongoing lifecycle management focused on product enhancements that sustain customer loyalty. This commitment supports a differentiated product portfolio engendering high barriers to entry through intellectual property protection combined with clinical endorsements. Additionally, Envista couples its hardware innovations with software offerings that streamline providers’ workflows — a strategic complement that bolsters customer retention by embedding Envista solutions deeper into clinical practice operations.

Growth Engines and Acquisition Strategy: Opportunities and Integration Hurdles

Envista actively pursues bolt-on acquisitions as a pillar of its growth model [S1]. The firm continuously evaluates targets that either augment existing capabilities or broaden avenues into attractive new dental technology niches. However, management acknowledges the complexity inherent in effectively integrating acquired businesses to realize projected synergies or cost saving opportunities — a factor that could temper near-term operating leverage [S1]. Past restructuring initiatives illustrate proactive efforts to absorb acquisitions efficiently while recalibrating capacity to reflect shifting demand landscapes. Although acquisitions can accelerate scale advantages and expand addressable markets, failure to execute integration smoothly remains a salient risk potentially disrupting operational consistency.

Navigating External Challenges: Currency, Tariffs, and Regulatory Risks

Envista confronts pronounced macroeconomic headwinds including persistent foreign exchange volatility which has tangible implications for reported revenues and margins given its multinational footprint [valye_report_excerpt][S1]. Trade tariffs have also raised input costs in certain jurisdictions necessitating pricing concessions or absorbing margin erosion temporarily. Complementing these are regulatory compliance demands entailing product registrations across diverse geographies that elevate operational complexity and expenses. Legal proceedings related to intellectual property or product liability claims further contribute as episodic risks with potential financial consequences [S1]. These external factors introduce layers of uncertainty requiring vigilant risk management practices to safeguard profitability.

Financial Health Snapshot: Liquidity, Margins, and Balance Sheet Strength

From a balance sheet perspective, Envista stands on solid footing with $1.21 billion in cash & equivalents offsetting $853 million in current liabilities — yielding a healthy current ratio of approximately 2.38 as of year-end 2025 [F1]. Operating margins exhibit segment-dependent variability but the company’s cost structure benefits from ongoing restructuring aimed at enhancing efficiency [S1]. While gross margin faced pressure from FX movements and tariffs in pockets of the business, overall operating profits grew supported by scale advantages particularly within Specialty Products & Technologies [F1][S1]. Maintaining this liquidity buffer equips Envista with financial flexibility to pursue strategic investments or weather macroeconomic disruptions.

Macro Risks and Emerging Threats: From AI to Supply Chain Vulnerabilities

Beyond traditional risks lie emerging issues such as artificial intelligence adoption which Envista leverages for process automation but also flags as introducing inherent operational uncertainties [S1]. Dependence on third-party information technology providers adds layers of cybersecurity vulnerabilities amid evolving threats targeting sensitive data assets intrinsic to medical device companies. Moreover, supply chain fragilities—exacerbated globally post-pandemic—pose intermittent risks for manufacturing continuity given the exacting specifications required for dental products [S1]. Data privacy laws evolving worldwide impose compliance costs alongside potential reputational damage if breached. Collectively these factors represent strategic uncertainties where proactive mitigation will influence future competitive positioning.

Outlook and Valuation Perspectives: What Surging Earnings Estimates Signal

Recent broker upgrades reflecting surging earnings estimates signal market confidence buoyed by Envista's demonstrated momentum over recent quarters [N7][N10][N11]. Analysts highlight robust core sales growth backed by innovation cycles while cautiously noting margin sensitivity to macro factors. The elevated valuation multiples implied incorporate both optimism over secular trends such as increasing orthodontic adoption rates globally as well as anticipated acquisition-fueled expansion. However, prudent valuation perspectives emphasize balancing near-term growth enthusiasm against persistent integration execution risks alongside geopolitical trade policy ripple effects that could weigh on cost structures or demand patterns.

Investor Takeaways: Momentum Stock Status and Strategic Considerations

In summary, Envista presents as a momentum-infused equity reflecting strong recent execution anchored by compelling dental technology assets coupled with disciplined capital allocation towards acquisition-led growth [N12][N13][S1]. Investors keen on thematic plays tied to healthcare innovation will note the company's well-established moat fortified through R&D investments delivering differentiated products embedded deeply within clinical workflows. That said, potential investors should weigh these strengths against integration complexities inherent in expanding via acquisitions alongside macroeconomic headwinds including currency turbulence and tariff escalations detailed extensively in SEC filings. Given the dynamic dental products industry landscape characterized by rising competition and evolving regulatory expectations, successful navigation will demand sustained innovation paired with operational agility.

This analysis is intended solely for informational purposes without any direct investment recommendations or advice. All data herein is sourced from publicly available materials as of February 2026; readers are encouraged to consult primary filings or professional advisors for decision-making.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments