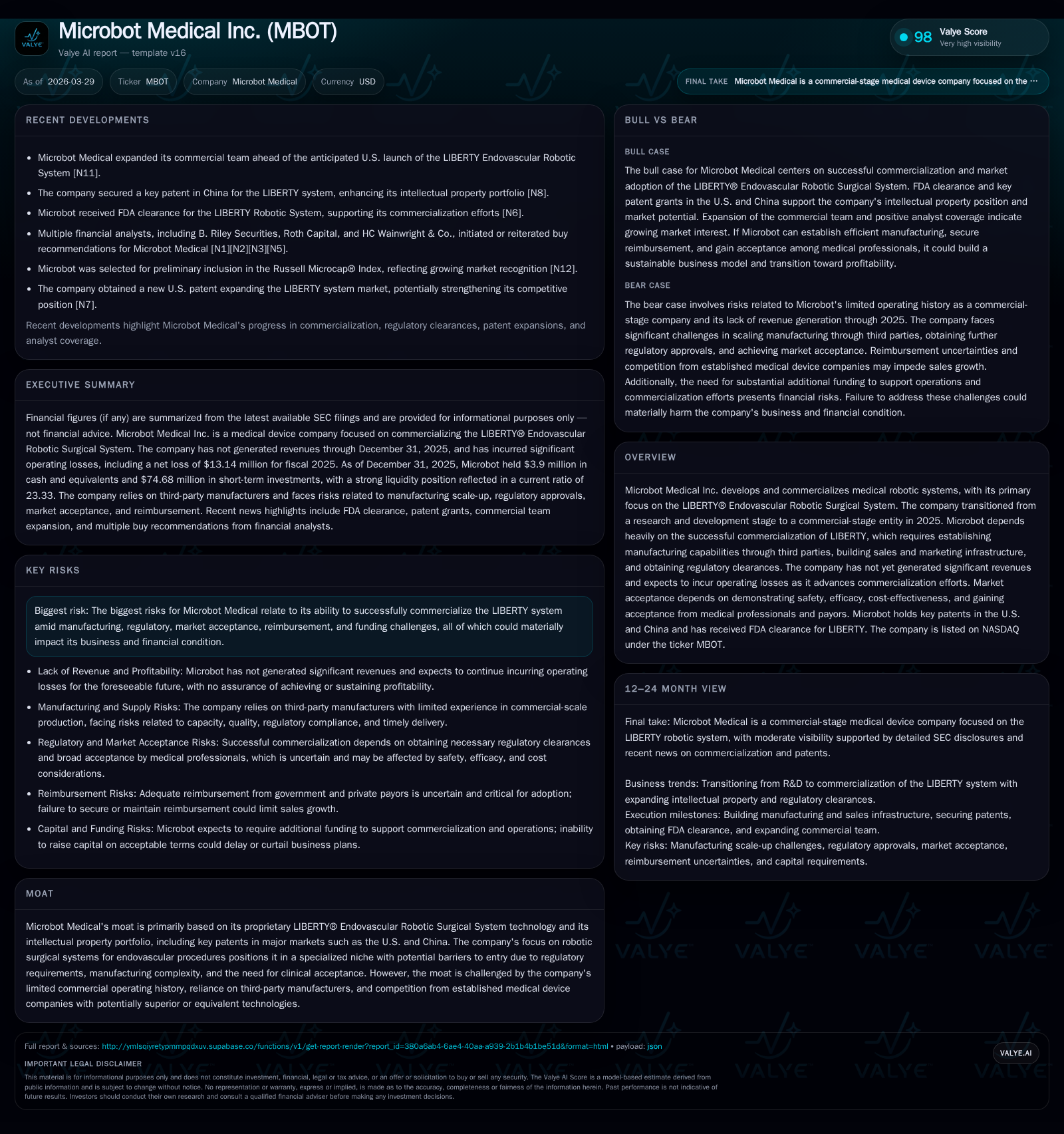

Microbot Medical's Transition to Commercial-Stage Hinges on LIBERTY® System Rollout Challenges

Microbot Medical moved from R&D to commercialization in 2025 but faces significant hurdles ahead.

Microbot Medical Inc. has shifted focus from research and development to commercial-stage operations with its flagship LIBERTY® Endovascular Robotic Surgical System receiving FDA clearance. Despite this progress, the company has yet to generate meaningful revenue and continues to incur substantial operating losses, reflecting the early nature of its commercialization efforts and reliance on third-party manufacturing. Key growth drivers include successful product adoption, expanded regulatory approvals such as CE marking in Europe, and building sales infrastructure, while risks include manufacturing scalability, reimbursement challenges, and intellectual property protection. Monitoring milestones around production ramp-up, revenue generation, and market acceptance will be critical in assessing Microbot’s transition trajectory.

Historical Performance

Microbot Medical’s financial history reflects its evolution as a developmental-stage medical robotics company focused on advancing the LIBERTY® Endovascular Robotic Surgical System. Through 2025, it had not recognized significant sales revenue, with only $29,000 booked in fiscal year 2015 and no meaningful revenue thereafter as the company concentrated on research and regulatory approvals rather than commercial activities [F1][S1].

Losses have been consistent and increasing as Microbot expanded efforts preparing for commercialization. Operating income declined from an operating loss of approximately $9.9 million in FY 2023 to a loss of $14.7 million in FY 2025 (a deterioration of about 26.8% YoY), evidencing intensifying investment in manufacturing setup, clinical trials support, quality assurance processes, and building sales and marketing infrastructure [F1]. Net losses also deepened from $10.7 million in FY 2023 to $13.1 million in FY 2025 (down roughly 14.8% YoY) during this period.

Operating cash flow mirrored these trends with an outflow of about $13 million in FY 2025 versus $8.8 million in FY 2024—a decline signaling mounting cash burn associated with product rollout activities [F1]. Capital expenditures remained modest relative to operating expenses but increased by about 140% from $25 thousand (FY24) to $60 thousand (FY25), likely reflecting investments in product tooling or manufacturing process enhancements.

Historical performance (annual)

| FY | Net ($mm) | CFO ($mm) | OpInc ($mm) | Capex ($) | Net YoY |

|---|---|---|---|---|---|

| 2025 | -13 | -13 | -15 | 60000 | -14.8% |

| 2024 | -11 | -9 | -12 | 25000 | -6.5% |

| 2023 | -11 | -9 | -10 | 33000 | +18.4% |

| 2022 | -13 | -12 | -13 | 84000 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | FCF ($mm) | ROE% |

|---|---|---|

| 2025 | -13 | -16.9 |

| 2024 | -9 | -324.2 |

| 2023 | -9 | -238.6 |

| 2022 | -12 | -180.7 |

Source: SEC companyfacts cache [F1].

Microbot Medical has not yet generated consistent revenue; losses reflect investment toward commercialization [F1].

Future Growth Prospects

The linchpin for Microbot Medical’s future lies predominantly with the successful commercialization of its LIBERTY® Endovascular Robotic Surgical System—the device designed for minimally invasive peripheral endovascular surgeries that leverage robotic precision to improve outcomes [S3]. The company gained FDA clearance for LIBERTY®, marking a crucial regulatory milestone necessary before marketing in the U.S., but is still pursuing approvals for other jurisdictions such as the European CE Mark [S21].

Growth drivers include:

- Establishing scalable manufacturing: Microbot relies on third-party contract manufacturers without prior experience producing at commercial volume; efficiency gains here are critical to controlling costs and ensuring supply chain reliability [S13][S26].

- Building sales/marketing infrastructure: As a first-time commercial operator post-2025, Microbot must develop sales teams capable of educating vascular surgeons and hospital buyers about LIBERTY’s clinical benefits and integration into procedural workflows.

- Clinical adoption: Physician acceptance depends heavily on long-term data supporting safety and efficacy plus ease-of-use claims—factors still under evaluation given the novelty of robotic-assisted endovascular approaches [S10][S16].

- Reimbursement & payor coverage: Obtaining insurance reimbursement codes for device-related procedures remains a major hurdle impacting physician willingness to adopt new technologies given their impact on hospital revenue cycles [S13][S25].

- Expanding product pipeline: Continued R&D may enable broader applications beyond current indications; however, progression timelines are uncertain due to FDA requirements and potential costly clinical trials [S16][S22].

Conversely, several factors could cap growth potential:

- Competitive landscape: Large established medical device firms possess deeper pockets, broader installed bases, and may release competing or more cost-effective robotic solutions [S28].

- Regulatory setbacks: Delays or denials around foreign market clearances (like CE Mark) could defer revenue streams outside the U.S., limiting total addressable market penetration.

- Manufacturing risk: Failure by third parties to meet cost or quality standards could cause recalls or lost customers potentially undermining brand reputation [S8][S10][S13].

- Funding constraints: Ongoing cash burn necessitates future capital raises which might dilute shareholders or limit operational flexibility if financing terms sour [S27].

Forecasts / Milestones / Expectations

Microbot has not provided explicit numeric guidance regarding revenue growth or profitability milestones since transitioning to commercialization late in its timeline [N#]/[S#] unavailable for such data.

Key events investors should monitor include:

- Initial commercial shipments timing: Revenue generation depends heavily on moving first units out of production into clinical use.

- Adoption rates by early adopters like Emory Healthcare completing robotic peripheral procedures using LIBERTY®, signaling clinical feasibility progressing beyond pilot phases [S3].

- Regulatory clearance status updates outside the U.S., especially CE Mark acquisition essential for European sales expansion.

- Reports on scaling manufacturing processes indicating ability to meet volume demands at competitive costs without compromising quality.

- Progress with payors confirming positive reimbursement policies facilitating physician uptake.

- Updates on additional product candidates stemming from existing micro-robotics platforms that could broaden addressable markets.

Without these developments materializing timely or successfully, forecasts remain speculative given the high risk profile conveyed by regulatory filings and absence of historical commercial operations.

Returns / Capital Allocation

As a pre-revenue entity undergoing commercialization transition through FY25:

- Return measures such as ROE are negative; calculated ROE stood approximately at -16.9% given net losses relative to equity base of about $77.6 million at year-end 2025 [F1].

- Operating cash flow continues negative at $13 million annually reflecting heavy investment ahead of any meaningful product sales.

- Capital expenditures remained minimal relative to operating costs indicating reliance primarily on existing assets or third-party manufacturing rather than internal capital-intensive facilities buildout [F1].

- No dividends or share repurchase programs have been initiated; all cash resources directed towards sustaining R&D efforts, regulatory submissions, personnel expansion and commercialization launch expenses.

Liquidity appears adequate currently with strong current ratio above 23 driven by high current assets relative to liabilities which are modest circa $3.4 million—providing runway but future capital raises likely needed absent rapid commercial traction [F1].[S27]

Competitive Moat & Risks Summary

Microbot Medical’s moat is established mainly through its proprietary LIBERTY® robotic platform protected by key U.S. and Chinese patents forming initial IP barriers to entry within specialized robotic-assisted endovascular surgery space—a niche that demands stringent regulatory clearance which itself acts as a barrier against simplistic entrants [S11]. However:

- The moat is constrained by Microbot’s lack of demonstrated commercial-scale manufacturing experience and dependency on third parties whose capability uncertainty introduces execution risk.

- Market penetration depends critically upon winning physician trust despite limited long-term safety/clinical outcome data given technological novelty impacting adoption rates.

- Competing against entrenched industry leaders who may leverage scale economies and deeper distribution networks represents ongoing headwind.

- Regulatory complexity extends beyond initial clearances; maintaining compliance and obtaining approvals internationally adds layers of cost and uncertainty.

- The company faces typical biotechnology-related risks including litigation (e.g., recent employment-related claims), cybersecurity threats affecting sensitive IP/data security further discussed in filings illustrating operational vulnerabilities that require management attention.

In summary: substantial upside exists if Microbot can successfully execute commercialization amidst considerable challenges intrinsic to emerging medical-device innovators transitioning out of R&D phase into competitive product markets.

Industry Context (Analysis)

Robotic surgical systems represent one of the fastest evolving segments within medtech driven by demand for precision minimally-invasive interventions reducing patient trauma while improving procedural accuracy—a trend accelerated by advancements in microelectronics, AI integration for navigation assistance, and enhanced user interfaces facilitating surgeon operation capabilities. Markets for endovascular interventions—treatment of peripheral artery disease among others—are expanding due to aging populations combined with rising prevalence of diabetes triggering vascular complications. However,the barriers are formidable: FDA class II device clearances often require rigorous substantiation via bench/animal studies supported by clinical trials under IDE protocols; reimbursement pathways evolve slowly influenced by payer evaluations balancing innovation benefits vs budgetary impacts;and widespread adoption requires overcoming entrenched surgical habits often conservatively favoring known technologies. This context underscores why many companies flounder converting promising tech into sustained profits despite disruptive potential which depends heavily on navigating regulatory nuances coupled with forging strong clinical collaborations enabling real-world evidence generation supporting broad use-case validation.

Conclusion

Microbot Medical Inc.’s shift toward commercialization marks an important inflection point after years focused largely on R&D culminating in FDA clearance of its core LIBERTY® Endovascular Robotic Surgical System in late-stage development pipeline now poised for market launch activities starting in 2025 [S1][F1]). However: cash flow negativity persists alongside unproven manufacturing scale-up capacity, the client uptake curve remains untested, and significant competitive/regulatory/reimbursement risks loom large. potential exists within rapidly growing robotic-assisted interventional surgery sector but execution challenges must be carefully monitored via key operational milestones including manufacture readiness, sales ramp, demonstrated clinical efficacy acceptance, and new regional approvals particularly CE Mark status pending.[S21] the coming quarters will test whether Microbot can translate technological promise into sustained commercial traction within complex medtech ecosystem characterized by innovation-driven opportunities tempered heavily by regulatory rigor, cost-sensitivity, and entrenched competition dynamics.

This report is intended solely for informational purposes summarizing company data available as of March 29, 2026. It does not constitute investment advice or recommendations. Investors should conduct their own due diligence considering their specific circumstances.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments