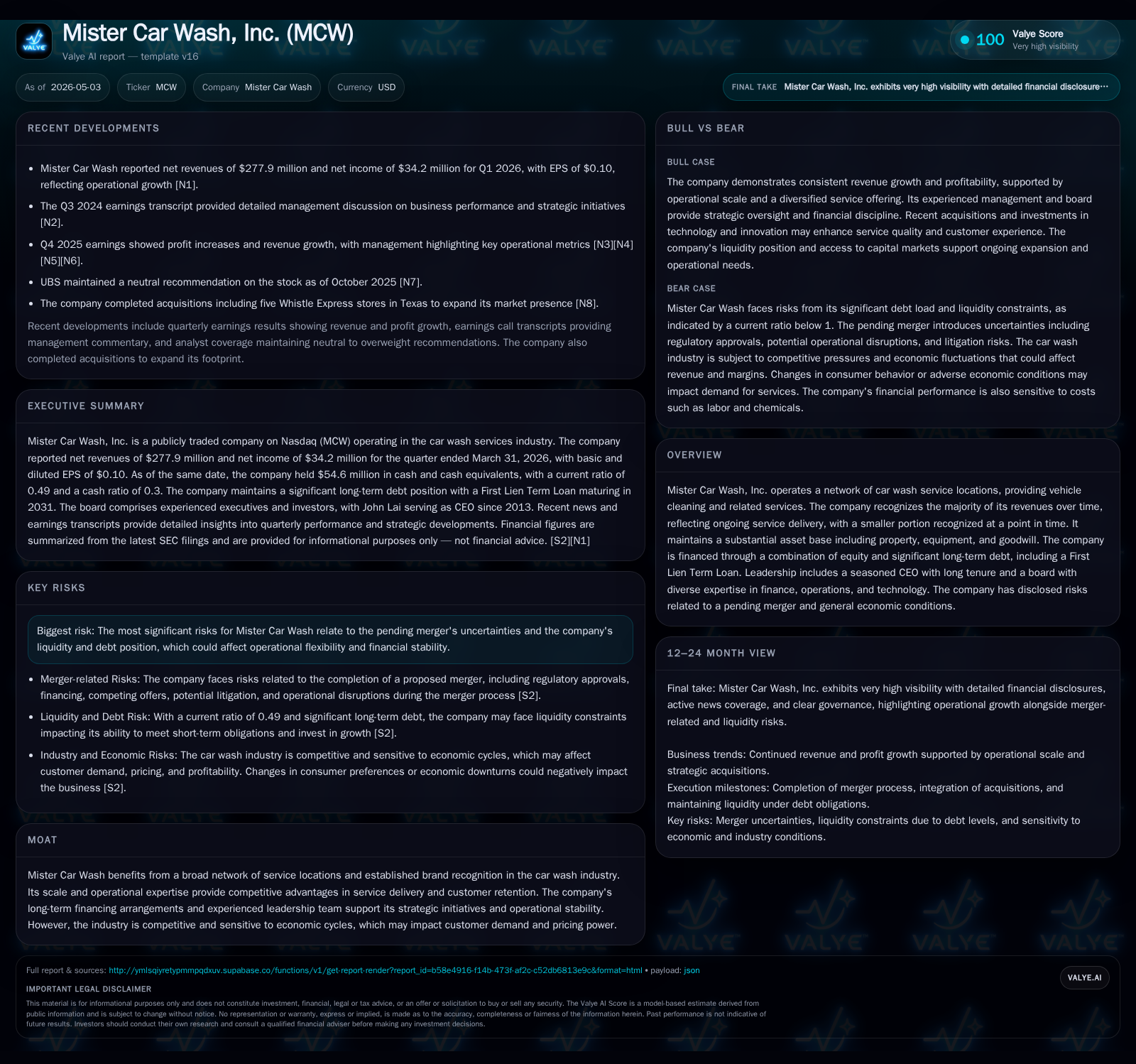

Mister Car Wash Q1 2026 Update Highlights Operational Resilience and Strategic Merger Risks

Mister Car Wash reports steady first quarter performance while navigating merger uncertainties amid a leveraged capital structure.

Mister Car Wash disclosed solid Q1 2026 operational metrics with no near-term debt maturities, supported by stable cash balances, but flagged challenges from an ongoing merger process. The company’s business model centers on a broad network of service locations offering vehicle cleaning services, generating recurring revenue primarily through ongoing service contracts. While scale and brand recognition underpin competitive advantages, the car wash industry faces cyclical demand sensitivity. Growth is driven by new location openings and customer retention strategies, with risks including merger-related operational disruptions and substantial long-term leverage.

Recent Operating Update: Q1 2026 Financials and Strategic Context

Mister Car Wash reported its latest quarterly filing on May 1, 2026 [S2], revealing several noteworthy aspects relevant to its near-term operational and financial condition. The company stated it faces no required debt payments until the maturity date in March 2031 for its first lien term loans. Total net debt stands around $745 million after deducting cash and equivalents of approximately $54.6 million as of March 31, 2026 [F1]. This capital structure continues to rely heavily on long-term financing arrangements amended in 2024 with Bank of America as administrative agent, including a revolving credit facility with borrowing capacity doubled to $300 million and subject to leverage covenants capped at a net leverage ratio of 6.5x [S4].

Further transparency around fair value accounting was updated with interest rate swap valuations included in assets and liabilities pockets of the balance sheet [S2]. Management also disclosed that the merger process underway introduces significant uncertainties encompassing regulatory approvals, financing procurement by the acquirer, management distraction risks, and potential disruptions to both business operations and customer relationships [S8]. This merger-related caution underscores a key contrast between operational stability in the quarter versus looming strategic transition risks.

Complementing these SEC updates, market observers highlight that MCW beat earnings expectations in Q1 2026 [N1], consistent with management's focus on operational efficiencies despite industry headwinds.

Business Model: Revenue Mechanics and Service Offering

Mister Car Wash generates revenue primarily through its extensive network of vehicle cleaning service locations distributed nationally. Revenue streams hinge largely on ongoing service delivery recognized over time, which reflects membership or subscription models wherein customers pay for regular washes — anchoring recurring revenue predictability. A smaller portion comes from immediate sales at service points such as vacuum stations or detailing services that are recognized at the point in time when rendered [S1].

Customers typically pay via membership programs or per-wash transactions; volume drivers depend on customer visit frequency influenced by weather patterns, economic conditions, vehicle ownership levels, and regional demographics. Pricing dynamics are shaped by competitive pressures but benefit from MCW's brand strength and scale economies that facilitate promotions while maintaining reasonable margins.

Margins are subject to variability based on labor costs, chemical expenses for wash materials, and site-level operational efficiency. The company invests in state-of-the-art equipment to bolster throughput and quality while reducing labor intensity. Customer retention efforts emphasize convenience—such as app-based scheduling—and consistent quality to encourage loyalty amidst numerous local alternatives.

Industry Structure and Competitive Position

The car wash industry is fragmented yet characterized by several established regional players alongside national platforms like Mister Car Wash. Entry barriers remain moderate due to capital requirements for facilities and equipment.

Competition emerges not only from other branded chains but also local independents offering price-driven alternatives. Pricing power is thus modest; inflationary pressures on chemicals and wages can squeeze profitability unless offset by volume gains or operational improvements.

Mister Car Wash’s extensive footprint affords it advantageous supply chain arrangements and brand recognition that support higher customer retention compared to smaller peers. Its long-standing operating history combined with data-driven customer engagement strengthens switching costs for consumers favoring convenience and reliability.

Growth Drivers

Organic Expansion: The company systematically adds new wash locations in targeted markets where it sees underpenetration or strong demographic growth vectors. These openings require upfront capital investments but tap into existing platform synergies.

Acquisitions: Selective acquisitions complement geographic expansion plans or add complementary services to broaden customer appeal. Integration focus remains integral to preserving margins post-acquisition.

Subscription Programs: Growth in monthly membership enrollments provides predictable revenue streams with higher lifetime value per customer through increased visit frequency incentivization.

Technology Investments: Enhancements such as mobile app integration for scheduling and payments improve user convenience promoting higher retention rates.

While these drivers present opportunities for scale gains and margin improvements, broader economic conditions that impact discretionary spending can cause softness in volumes — an inherent cyclical vulnerability within this segment.

Risks / Growth Constraints

Merger-Related Uncertainty: Pending merger execution risks could distract management focus, stall strategic initiatives, or unsettle employees and customers during transitional phases [S8]. Regulatory hurdles or financing challenges may delay or derail completion.

Leverage Profile: Substantial net debt nearing three-quarters billion dollars raises financial flexibility concerns. Despite no near-term maturities until 2031, stringent covenant adherence amidst volatile earnings demands prudent liquidity management [F1][S4].

Industry Cyclicality: Vehicle wash demand fluctuates seasonally and economically; recessionary periods or spikes in fuel prices may reduce discretionary automotive maintenance expenditures impacting volumes.

Competition & Pricing Pressure: Mature markets intensify pricing competition limiting ability to pass through cost inflation fully without risking customer loss.

Operational Cost Inflation: Rising labor costs or chemicals could compress margins if not offset by efficiency gains or price increases.

What to Watch Next

Investors should monitor the following key developments:

- Progress toward completing the announced merger including regulatory clearances, financing arrangements by the acquirer, shareholder approvals, and timing updates [S3][S8].

- Quarterly earnings releases for indications of stable or improving customer usage patterns and pricing power amid macroeconomic shifts.

- Leverage covenant compliance reports particularly Rent Adjusted Total Net Leverage Ratio metrics tested quarterly per amended credit agreements [S4].

- Execution success of new location openings or acquisitions contributing incremental revenues without diluting margins.

- Operational cost trends especially labor wage inflation impacts versus productivity improvements.

Financial Profile Snapshot (Q1 2026)

Latest financial snapshot

| Metric | Value | Period |

|---|---|---|

| Cash & equivalents | $55mm | |

| 2026-03-31 | ||

| Total debt | $800mm | |

| 2025-12-31 | ||

| Net debt | $745mm | |

| 2025-12-31 | ||

| Current assets | $89mm | |

| 2026-03-31 | ||

| Current liabilities | $183mm | |

| 2026-03-31 | ||

| Current ratio | 0.49x | |

| 2026-03-31 |

Source: SEC companyfacts cache [F1].

Mister Car Wash reported an operating income of approximately $200 million at FY-end December 31, 2025 along with net income of $103 million providing a profitable base though leverage metrics remain elevated [F1]. The company has refinanced its first lien credit agreement recently improving borrowing capacity yet retains amortization schedules starting late-2024 requiring disciplined cash flow generation going forward [S4].

This analysis is based strictly on available disclosures from Mister Car Wash's SEC filings through May 2026 without investment recommendations or forecasts. All values reflect reported data without conjecture beyond documented evidence.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments