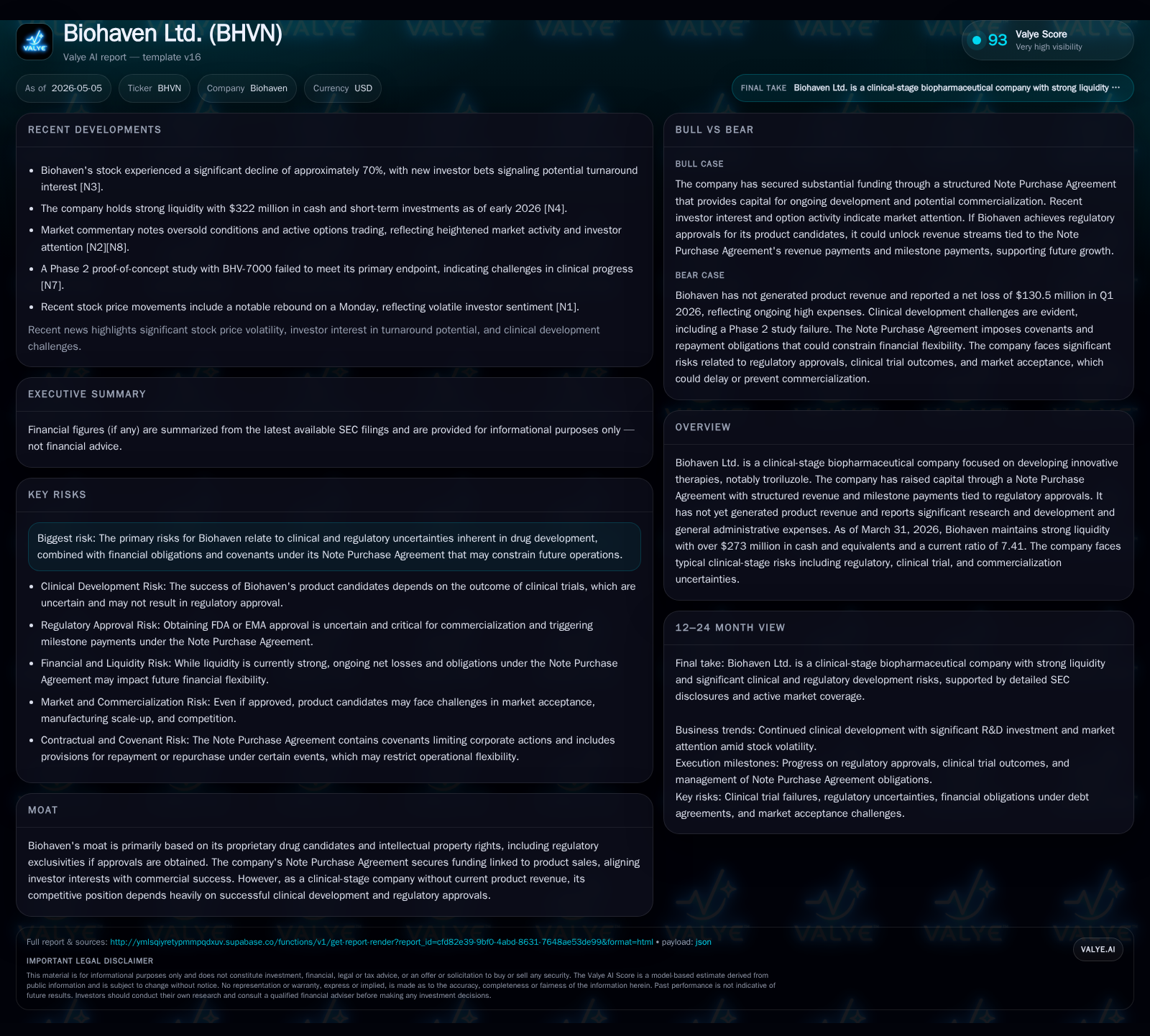

Biohaven Ltd. Advances Clinical Pipeline with $273M Cash Cushion Amid Regulatory Milestones

Biohaven's latest quarter highlights clinical progress, funding structure, and strategic risks ahead of potential FDA approval for troriluzole.

Biohaven Ltd., a clinical-stage biopharmaceutical company, reported significant progress in its pipeline during Q1 2026, maintaining a strong liquidity position with $273 million in cash and equivalents. The company's revenue model hinges on the future commercialization of its lead candidate, troriluzole, with milestone-driven funding from a senior secured Note Purchase Agreement that aligns investor returns with product sales. Despite encouraging developments, Biohaven remains exposed to typical clinical-stage risks including regulatory approvals, clinical trial outcomes, and financial covenants tied to its note agreements. Growth drivers center on late-stage clinical advancement and potential regulatory milestones, while watchpoints include capitalization of the contingent second tranche funding and successful commercialization preparations.

Recent Operating Update

Biohaven Ltd.’s Q1 2026 SEC filing [S2] reveals a secure liquidity position with $273 million in cash and equivalents as of March 31, 2026, coupled with a current ratio of 7.41 [F1]. This liquidity supports continued investment in their clinical pipeline during absence of product revenues. The company publicly disclosed ongoing expenses tied primarily to advancing their key drug candidate troriluzole through late-stage studies alongside other pipeline programs.

Simultaneously filed event disclosures [S3] reiterate these points alongside management commentary highlighting expectations for continued R&D investments aligned with approaching regulatory milestones. Importantly, the Note Purchase Agreement established in April 2025 underpins Biohaven’s financing strategy by coupling investor returns directly to future commercial success through royalty-like revenue payments linked to net sales of troriluzole if approved.

Business Model and Revenue Mechanics

Biohaven operates as a clinical-stage biotech research company focused on novel therapies such as troriluzole. Its current business model centers on advancing proprietary drug candidates through costly preclinical and clinical development phases toward regulatory approval.

The company has not yet generated product sales revenue; instead, it funds operations primarily through equity issuances and debt placements—most notably the Note Purchase Agreement which raised an initial $250 million senior secured note offering in April 2025 [S1]. This financing structure includes contingent tranches totaling up to an additional $350 million conditioned on FDA approval milestones for troriluzole.

Revenue generation mechanics are explicit: upon FDA marketing approval and commercial launch of troriluzole, Biohaven will owe note holders Revenue Payments starting at 6.25% of global net sales [S1]. This percentage can increase or decrease depending on cumulative payments against total funded amounts by a set test date (December 31, 2030).

Margins remain speculative given no current sales; however, if approved, scaling production and distribution costs will influence future profitability alongside royalty escalations embedded in financing agreements. Operational expenses continue heavily weighted toward R&D and general & administrative functions necessary to sustain pipeline progression.

Industry Structure and Competitive Position

Biohaven resides within the specialty pharmaceutical sector characterized by high R&D intensity and significant regulatory hurdles. The company’s competitive advantage lies principally in its proprietary intellectual property portfolio surrounding unique molecules like troriluzole—a glutamate modulator with neuroprotective potential.

Commercial differentiation depends on advancing these candidates beyond proof-of-concept into commercially viable products with demonstrated efficacy and safety profiles that meet regulatory criteria globally.

Unlike diversified pharma conglomerates with multiple revenue streams, Biohaven’s risk profile is concentrated: clinical trial outcomes dictate near-term survival prospects. There is no entrenched commercial infrastructure yet; success will demand substantial build-out or partnership/licensing deals post-approval.

In this landscape, speed to market combined with patent protection windows will be critical moats alongside scientific differentiation targeting high-unmet medical needs such as neurodegenerative conditions.

Growth Drivers

- Regulatory Milestones: Primary growth catalyst is FDA approval of troriluzole triggering additional funding tranches ($150M Second Notes) thereby extending operational runway [S1]. Positive trial data releases would also bolster risk assessment favorably.

- Pipeline Advancement: Expansion beyond troriluzole into other clinical-stage candidates (e.g., BHV-8000, BHV-1510) diversifies potential future revenue sources.

- Commercialization Readiness: Building manufacturing scale-up capacity and commercial infrastructure post-approval will enable market entry timing advantages.

- Strategic Partnerships or Acquisitions: Potential licensing deals or acquisitions funded by optional $200M Third Notes would strengthen portfolio breadth.

- Intellectual Property: Maintaining exclusive rights via patents and license agreements preserves market exclusivity which is vital given competitive biological pathways targeted.

These drivers link closely to tangible KPIs: successful trials completions, receipt of marketing authorizations, newly initiated pivotal studies or expansion cohorts, licensing milestones reached, manufacturing readiness indicators, and capital funding releases.

Risks / Watchpoints / Growth Constraints

- Clinical & Regulatory Risk: Failure to demonstrate required efficacy or safety standards could impose irreversible setbacks or termination of programs [S7]. Delays in enrollment trials or FDA review processes can also impact timelines significantly.

- Milestone Payment Burden: Obligations include development milestone payments under license agreements adding short-term cash outflows [S22].

- Competition & Market Entry: Even if approved, Biohaven may face competing therapies from larger players with established sales forces unless strategic collaborations materialize rapidly.

- Patent & IP Challenges: Patent expirations or contention could erode exclusive positioning [S12].

Close attention must be paid to upcoming FDA communications regarding troriluzole’s approval status along with trial update releases that predicate funding drawdowns.

What to Watch Next

- FDA Approval Decision: Critical inflection point triggering Second Notes issuance worth up to $150 million before June 30, 2026 [S1].

- Clinical Trial Updates: Data readouts from ongoing Phase 3 studies or registrational trials affecting market entry timing.

- Milestone Achievement Announcements: Progression along licensing deal terms especially for partnered assets outside primary pipeline.

- Capital Raising Activity: Additional equity offerings or strategic partnerships signaling capacity building for commercialization efforts.

These events collectively set the trajectory for transitioning from clinical-stage investment mode toward commercial execution phase.

Brief Financial Profile Context

Latest financial snapshot

| Metric | Value | Period |

|---|---|---|

| Cash & equivalents | $273mm | |

| 2026-03-31 | ||

| Current assets | $386mm | |

| 2026-03-31 | ||

| Current liabilities | $52mm | |

| 2026-03-31 | ||

| Current ratio | 7.41x | |

| 2026-03-31 |

Source: SEC companyfacts cache [F1].

As of Q1 2026 end, Biohaven boasts:

| Metric | Value | Period Ended |

|---|---|---|

| Cash & Equivalents | $273 million | |

| 2026-03-31 | ||

| Current Assets | $386 million | |

| 2026-03-31 | ||

| Current Liabilities | $52 million | |

| 2026-03-31 | ||

| Current Ratio | 7.41 | |

| 2026-03-31 |

The company continues reporting operating losses consistent with heavy R&D investments (-$745 million operating income FY-end 2025) but retains sufficient liquidity for near-term development expenditures [F1]. No product revenues have been recorded; thus financial sustainability hinges on milestone-triggered note proceeds plus prudent cash management [S2][S3].

Disclaimer

This analysis is intended solely as an informational overview based on publicly filed SEC materials as of May 2026. It does not constitute investment advice or recommendations regarding Biohaven Ltd.’s securities.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments